All Activity

- Today

-

Google's FAQ removal and new Ahrefs research challenge schema's value for SERP visibility and AI citations. The post SERP FAQ Removal & New Data Challenge Schema’s AI Search Value appeared first on Search Engine Journal. View the full article

-

Death of Izz al-Din al-Haddad in an air strike piles greater pressure on fragile ceasefire View the full article

-

US president is using threats and inducements to force communist island to open up its economy as it runs out of fuelView the full article

-

When Olympic skier Eileen Gu walked the steps of the Metropolitan Museum of Art at the Met Gala on May 4, she wore a short, shimmering gown that appeared to be made of thousands of iridescent soap bubbles caught mid-float, clustered across her body and trailing into the air behind her. Eileen Gu It was created by Iris van Herpen in collaboration with the Tokyo-London design studio A.A.Murakami. Assembled from 15,000 hand-formed glass bubbles, it took 2,550 hours to construct, and contained hidden microprocessors that released real bubbles into the air as Gu moved. It was also a glimpse into the show that opens at the Brooklyn Museum on May 16: Iris van Herpen: Sculpting the Senses, the North American debut of a retrospective that has already traveled from Paris to Brisbane, Australia, then Singapore and the Netherlands. The 2016 original of that bubble dress will be in the show. “It represents the air that’s inside of our bodies,” says Matthew Yokobosky, the Brooklyn Museum’s senior curator of fashion and material culture. “Over 90% of our bodies are made up of air.” Over two decades, van Herpen has built a body of work that treats science as a creative collaborator. She has made couture inspired by the air in our lungs, the architecture of a stingray’s skeleton, the magnetic fields of the Large Hadron Collider. She has worked with architects, paleontologists, and biologists, and used everything from iron filings to magnets to bioluminescent algae as raw materials. In doing so, she has quietly redefined what it means for fashion to be art. The Brooklyn Museum has been making that argument for nearly a century. Its 1934 Story of Silk exhibition is often cited as the beginning of fashion’s museum era; it has since staged retrospectives of work by Madame Grès, Schiaparelli, Jean Paul Gaultier, Pierre Cardin, Christian Dior, Virgil Abloh, and Thierry Mugler. Sculpting the Senses extends the lineage. Water in all its forms The bubble dress is a launchpad for the exhibit. “The show starts about different inspirations from the different forms of water, liquid, frozen, gaseous, and how all those different states have been equally informative for her as a design inspiration,” Yokobosky explains. It is paired with a piece by the Japanese art collective Mé, a work that Yokobosky says “looks as if they had taken a slice of the ocean and put it into the gallery.” Van Herpen, who grew up in the Dutch village of Wamel, has returned again and again to water in all its states. That preoccupation goes back to the work that put her on the map. Her 2010 Crystallization collection, built around limestone deposits, ice crystals, and the choreography of a splash, contained the first 3D-printed garment ever shown on a fashion runway. The skeletal, ivory-colored top made in collaboration with British architect Daniel Widrig, is on display in Brooklyn. Depending on the angle, the piece looks like a fossilized vertebra or a Dutch ruff from the 17th century. Materialise, the Belgian 3D-printing firm that helped fabricate it, had until then been making architectural models. Bones, fossils, and a baby dinosaur Since the natural history specimens in the Paris version of van Herpen’s show couldn’t travel, Yokobosky struck up a new partnership with the American Museum of Natural History. The Brooklyn show now includes an 80-million-year-old ichthyosaur skeleton and a baby dinosaur, displayed in dialogue with van Herpen’s bone-inspired couture. A gown built around the architecture of bird skeletons sits near the dinosaur fossils—a nod to the fact that birds are the closest living relatives of dinosaurs. “When you look at Iris’s gown, you don’t necessarily see bones immediately, but as you look more closely, you realize that there are all those articulations of bone,” Yokobosky says. Biomimicry runs deep in van Herpen’s work. Her atelier doesn’t replicate a fish scale; it studies how a fish scale is structured, then translates that structure into a new material. Lucid (2016) borrowed from the orb webs of argiope spiders. Sympoiesis and Sensory Seas took their cues from coral systems. The designer’s work has a sustainability dimension too. Van Herpen has experimented with garments made from recycled plastic ocean waste, 3D-printed cocoa beans, and, last year, created a “living” dress in collaboration with biodesigner Chris Bellamy that was seeded with 125 million bioluminescent algae. In an industry that produces somewhere between 92 million and 100 million tons of textile waste every year, the gesture suggests that garments don’t have to come from petrochemicals. They can come from a lab, or a forest, or—occasionally—a tide pool. The slowest fashion The most quietly radical section of the show may be the one with no garment at all. For the Brooklyn exhibit, van Herpen created a new video installation that takes the small, often invisible gestures of her atelier—the placement of a hand, the catch of a needle, the slow accumulation of a single embroidered surface—and projects them, unedited and in real time, onto 25-foot-high screens inside the museum’s 70-foot rotunda. “She really wanted people to understand the slow process that goes into making couture . . . what emerges from this long, meditative process,” Yokobosky says. Fashion in 2026 is dominated by AI-generated lookbooks, Shein-style ultrafast cycles, and the increasingly seamless integration of agentic commerce into the shopping experience. In contrast, van Herpen does not even do ready-to-wear; she focuses entirely on couture. She still makes everything by hand, in collaboration with a rotating cast of scientists and artists, and she still sells the pieces. She just doesn’t make very many of them. “She is very devoted to the craft of couture and to experimenting and helping us understand what is possible in the future of fashion,” Yokobosky says. The Brooklyn show closes in a space the museum is calling Cosmic Bloom: a darkened room full of mannequins suspended from the ceiling at strange angles, wearing some of van Herpen’s most surreal and saturated gowns. It is also a clear statement of what the entire exhibition is arguing—that the body, in van Herpen’s hands, isn’t a hanger for product. It is a small piece of the universe, and clothing is one of the languages we use to describe it. Sculpting the Senses runs through December 6. View the full article

-

Kevin Warsh is now likely to secure Senate approval as the next Federal Reserve chair—and become arguably the most powerful central banker in the world. But when Warsh appeared before the Senate Banking Committee for his confirmation hearing in April, one punchy question underscored the dilemma that Warsh, lawmakers and the Fed all face: “Are you going to be the president’s human sock puppet?” asked Republican Senator John Kennedy of Louisiana. On one level, the question reflects President Donald The President’s intense pressure on the central bank to cut rates, with current Chair Jerome Powell often the target of his ire. But it also points to Warsh’s own inconsistency on inflation. Earlier in his career, he was a “hawk,” pushing for interest rate hikes to curb inflation and opposing the novel crisis management authorities that the Fed took on after the 2008 financial meltdown. Now, Warsh supports the interest rate cuts that The President has exhorted as a way to juice growth. Warsh has also come under fire for his deep ties to the financial sector, where he once worked. Lawmakers such as Democratic Senator Elizabeth Warren of Massachusetts have cited the potential conflict of interest posed by his undisclosed assets, even though in theory they’ll be divested as part of Warsh’s arrangements with the government’s ethics watchdogs if he becomes chair. As scholars who study central banks and the politics of finance, we understand why concerns about Warsh’s credibility have persisted. But perhaps counterintuitively, we also believe that once he’s confirmed, his finance background could reinforce his prior hawkish leanings, leading to more independence from The President on inflation and interest rates. Is past prologue? If confirmed as chair, as expected, Warsh and his colleagues on the Fed’s policy-setting committee would wield enormous power. Not only does the central bank set the benchmark rate that determines short-term lending, but the Fed also oversees a US$6.7 trillion balance sheet, mostly in government bonds, that partially affects longer-term borrowing costs. Guided by its mandate to control inflation, the Fed’s decisions impact everything from grocery prices to mortgage rates. Along with Warsh’s prior stints in government and on the Fed’s policymaking board as a governor, he worked for the investment firm Morgan Stanley and the hedge fund Duquesne Capital. In those positions, Warsh advanced his career in an industry that has long preferred hawkish Fed policies, even at the cost of job growth: Wall Street is generally “conservative” in that it favors lower inflation and higher interest rates on grounds that those policies can support bigger bank profits and higher prices for bank shares, while reducing the risks brought by disinflation policies. While serving as a Fed governor in the aftermath of the 2008 financial crisis, Warsh’s comments reflected this outlook. He talked extensively about inflation being a “choice”—that is, the result of poor policy decisions, rather than broader structural forces. He also questioned the Fed’s massive bond purchases, which were meant to stimulate the economy and reduce high unemployment by pushing long-term borrowing rates lower. The Fed revived those bond buys during the pandemic recession, while waiting too long, in the eyes of many economists, to hike rates once inflation began rising in 2021. More recently, Warsh has focused his criticism on the central bank’s “bloated” balance sheet as well as its inflation record. Those legacies, along with the stimulative government spending under President Joe Biden, prompted Warsh to warn in February 2022 that “extraordinary excesses in monetary and fiscal policy caused the inflation dragon to resurface after 40 years of dormancy.” Which Warsh will show up? Given that long record, many Fed watchers looked at his turnaround in the second The President administration with some skepticism. When he was a finalist for the nomination to chair the central bank in summer 2025, he told CNBC that the Fed’s hesitancy to cut rates—which was already drawing The President’s wrath—was “quite a mark against them.” “The specter of the miss they made on inflation, it has stuck with them,” he added. “So one of the reasons why the president . . . is right to be pushing the Fed publicly is we need regime change in the conduct of policy.” Warsh’s rhetorical shift has led many to ask whether he can reconcile his responsibilities with political pressure. But the worsening inflation outlook for both the U.S. and world, driven by spiking oil prices, may force his hand regardless. The spike in oil prices from the Iran war, in particular, has economists raising their inflation forecasts for the U.S. At his last Fed meeting as chair, Powell indicated that the central bank could be a long way off from lowering rates given inflation concerns. The Bank of England and the European Central Banks are also bracing for possible rate hikes if inflation doesn’t ease. The President ramp ups the pressure For his part, The President has used unprecedented means to bend the Fed since returning to office. Those tactics include trying to fire Fed Governor Lisa Cook and threatening to fire Powell—who just announced he will stay on as a governor on the Fed’s board after his chairmanship ends. Those kinds of pressure tactics—which effectively seek to restaff the Fed’s leadership with more members favoring interest rate cuts—are more often seen in countries like Turkey or Argentina. So why do we believe that Warsh won’t be the “human sock puppet” some fear? In our view, it’s his background in finance that leads us to think he’ll be able to resist political pressure once on the job. After all, when Powell was appointed by The President during his first term, he had also worked in that sector—and he has demonstrated independence from both The President and Biden. This is not just a theory. Political scientist Chris Adolph has identified a pattern in which Wall Street is the “shadow principal” of the central bankers who shuffle in and out of the financial sector. Similarly, economist Adam Posen has described finance as the interest group with the most prominent lobbying role over monetary policy. In practical terms, this means that Warsh has long been steeped in ideas about inflation that have traditionally held sway over the financial sector, and he may well be more open about these preferences once confirmed. Moreover, he’s likely to return to finance once his term at the Fed ends. Together, we believe these factors may give Warsh the intrinsic motivation and enough incentives to resist overt political pressure from the president. Of course, being too beholden to Wall Street is also a risk, as pointed out by Warren and others. The Fed is meant to support Wall Street in times of crisis—and even more so since the 2010 Dodd-Frank reform. However, the Dodd-Frank Act also asked the Fed to monitor risks to the entire financial system by supervising and regulating financial institutions. That requirement requires the Fed to prevent crises, not just bail out Wall Street when a crisis hits. As it happens, the Fed today is quietly but surely moving to water down the rules put in place after 2008—a deregulatory shift that Warsh strongly supports. Fed independence from government, as a matter of law and of norms, is deeply important for the health of the U.S. economy. And Warsh’s rhetorical shifts on monetary policy raise serious questions about its fate under his chairmanship. Senators have been right to push him as a nominee on this matter. However, the Fed also faces pressure from the finance industry, often pulling policy in the opposite direction. As such, we believe that Warsh’s professional history in finance may bolster his autonomy from The President on rates once he’s confirmed. Cristina Bodea is a professor of political science at Michigan State University and Andrew Kerner is an assistant professor of political science at Michigan State University. This article is republished from The Conversation under a Creative Commons license. Read the original article. View the full article

-

Extreme Networks is ramping up its Wi-Fi strategy with loads of new APs. Here's our conversation with Dave Coleman. The post TECH WATCH: Extreme Networks expands Wi-Fi strategy and AP portfolio appeared first on Wi-Fi NOW Global. View the full article

-

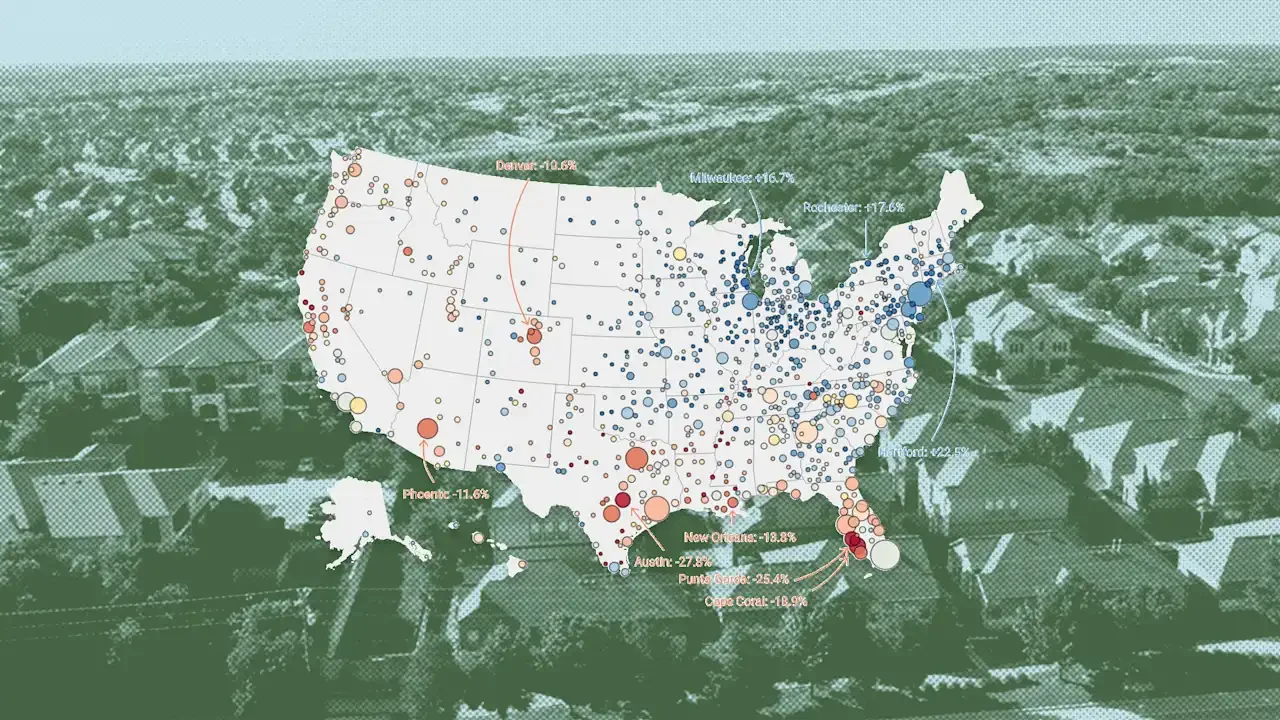

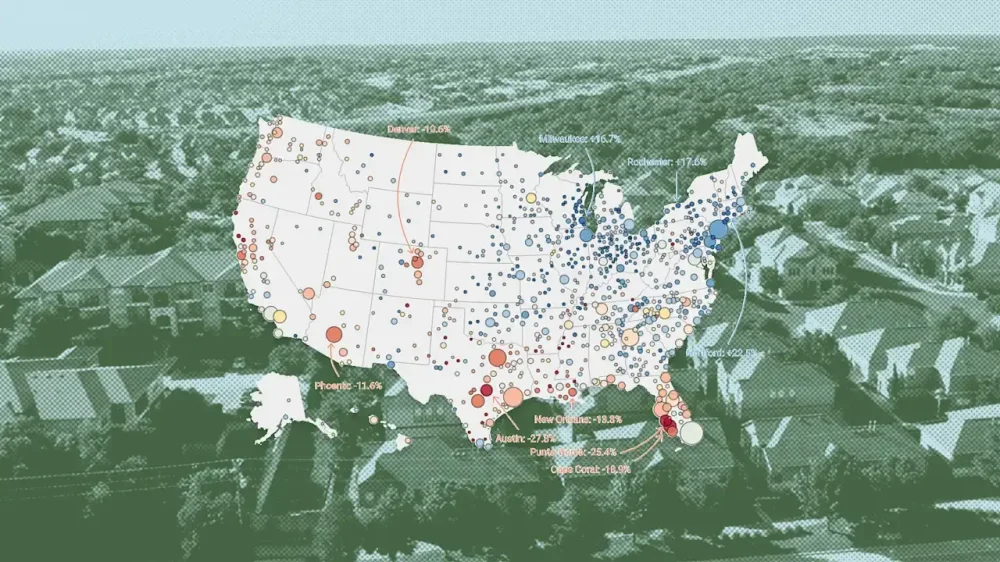

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. During the pandemic housing boom, housing demand surged rapidly amid ultralow interest rates, stimulus, and the remote work boom. Federal Reserve researchers estimate “new construction would have had to increase by roughly 300% to absorb the pandemic-era surge in demand.” Unlike housing demand, housing stock isn’t as elastic and can’t quickly ramp up. As a result, the heightened demand drained the market of active inventory and caused home prices to overheat, with U.S. home prices in June 2022 sitting at a staggering 43.2% above March 2020 levels. The run-up was even greater in some metro markets, including Naples, Florida (+73%); Austin, Texas (+73%); Punta Gorda, Florida (+71%); Cape Coral-Fort Myers, Florida (+70%); and North Port-Bradenton-Sarasota, Florida (+69%). Not long after mortgage rates spiked in 2022, the pandemic housing boom fizzled out. Since June 2022, the nationally aggregated housing market has been going through a period of recalibration—with U.S. home prices in March 2026 up just 2.2% above June 2022 levels, while weekly U.S. worker earnings during that same window jumped 14.7%. However, some markets’ so-called recalibration window has gone further, and they’ve passed through a home price correction. Among the nation’s 300 largest metro-area housing markets, these 15 markets have home prices this spring at least 10% below their local 2022 peak, according to ResiClub’s analysis of the Zillow Home Value Index: Austin-Round Rock-Georgetown, TX → -27.8% Punta Gorda, FL → -25.4% Cape Coral-Fort Myers, FL → -18.9% North Port-Sarasota-Bradenton, FL → -17.5% New Orleans-Metairie, LA → -13.8% Houma-Thibodaux, LA → -13.2% Boulder, CO → -11.8% Phoenix-Mesa-Chandler, AZ → -11.6% Naples-Marco Island, FL → -11.5% Lake Charles, LA → -11.4% San Antonio-New Braunfels, TX → -11.2% San Francisco-Oakland-Berkeley, CA → -11.0% Denver-Aurora-Lakewood, CO → -10.6% Dallas-Fort Worth-Arlington, TX → -10.1% Boise City, ID → -10.1% Note: Just because a market is still down from its 2022 peak doesn’t guarantee that home prices are still falling there. At the latest reading, home prices are up year over year in metro New Orleans (+2.1%), and pockets of San Francisco are seeing notable pricing action this spring. Many of the softest housing markets, where home prices are down the most from their 2022 peak, are located in Southern and Mountain West regions. Many of those areas were home to many of the nation’s top pandemic boomtowns, which experienced significant home price growth during the pandemic housing boom, which stretched housing prices beyond local income levels. Once pandemic-fueled domestic migration slowed and mortgage rates spiked, markets like Punta Gorda, Florida, and Austin, Texas, faced challenges, as they had to rely on local incomes to sustain frothy home prices. The housing market softening in these areas was further accelerated by the abundance of new home supply in the pipeline across the Sunbelt. When and where needed, builders are often willing to reduce prices or make other affordability adjustments to maintain sales. These adjustments in the new construction market also create a cooling effect on the resale market, as some buyers who might have opted for an existing home shift their focus to new homes where deals are available. In contrast, many Northeast and Midwest markets were less reliant on pandemic domestic migration and have less new home construction in progress. With lower exposure to that migration pullback demand shock—and fewer homebuilders offering large incentives—active inventory in these Midwest and Northeast regions has remained relatively tight. As ResiClub has previously covered, there’s a moderate statistical correlation (R² = 0.30) between Moody’s Q2 2022 valuation score and the change in home prices from their 2022 peak through March 2026. If the San Francisco metro area—the largest outlier—is excluded, that correlation strengthens slightly (R² = 0.39). Among the 412 metro areas that Moody’s Analytics tracks, Punta Gorda has seen the biggest drawdown in “overvaluation” since the pandemic housing boom fizzled out in Q2 2022. It’s followed by New Orleans, Cape Coral-Fort Myers, Austin, and North Port-Bradenton-Sarasota. In theory, as froth recedes and “overvaluation” comes down, so does downside risk. And that dynamic may already be quietly reshaping the risk profile in pockets of the Texas and Florida housing markets, where home prices have fallen and “overvaluation” has declined considerably since Q2 2022. View the full article

-

Graduation season is upon us, which means copies of Oh, the Places You’ll Go! are flying off bookstore shelves—since whimsical Seussian life advice has been the go-to gift for new graduates since 1990. But handing over a picture book seems especially unhelpful for the class of 2026. While every generation of young graduates seems to face a unique set of woes in their early adulthood, this year’s new grads are coming up against some particularly turbulent times. AI is gobbling up the entry-level jobs that new graduates need to get their foot in the door. Adding insult to injury, commencement speakers are encouraging grads to embrace their new AI overlords. But wait, there’s more! Inflation is up 3.8% (the highest it’s been in three years), and the unemployment rate for college graduates ages 22 to 27 was 5.6% as of December 2025, outstripping the national average. What’s more disheartening is that of those employed twentysomething college grads, 40% were working in jobs that didn’t require a college degree. Honestly, it’s understandable why parents might reach for Dr. Seuss to help counsel a newly minted graduate in times like these. (And possibly grabbing a fresh copy of Goodnight Moon to ease their own parental insomnia.) No matter how worrisome the economic news may be, however, there are practical gifts you can offer to your new grad that will help launch both their career and their personal financial success. Consider giving these gifts to the graduate in your life. Teach them soft skills When I was 14 years old, a new classmate introduced herself with a handshake, and immediately critiqued the “limp fish” grip I offered in return. My new friend was the daughter of a minister, which meant she shook hands with dozens of parishioners every Sunday and knew a thing or two about greeting people that had never once occurred to me. It’s been more than 30 years, and I still use her advice on handshakes, introductions, and humor on a daily basis. Like my teenage self, the graduate in your life probably doesn’t know all the soft skills that are considered base-level knowledge in the business world. These might include things like: Networking: Learning how to network can be a difficult skill to master, especially if no one tells you that it’s often considered rude to ask a contact for a job directly. Email etiquette: You can save the grad in your life a great deal of heartache by teaching them to wait to type the recipient’s email address in the “To” line until after composing the email to their satisfaction. Interviewing: Practice interviews can help your graduate build up muscle memory for this nerve-wracking experience so they can feel more comfortable when they’re in a real interview situation. Sussing out workplace culture: Every workplace has a different kind of culture. You can help your graduate figure out a workplace’s culture during the interview process. For example, in every academic office I have ever known, the atmosphere among the support staff (especially among the office’s administrative assistants) is the best barometer for understanding the culture of the organization as a whole. Imparting this kind of wisdom to your new graduate can help them stand out among other job candidates and will help them fit in better when they land their first job. An easy budgeting program For many new graduates, walking across the stage marks the transition from childhood to adulthood—at least in the financial realm. Instead of being part of their parents’ budget, a new graduate is likely to be 100% responsible for their own financial decisions. (Well, until they get a flat tire and need to make an emergency withdrawal from the Bank of Mom and Dad). Depending on the young adult, this can be a difficult adjustment. You can help make the shift a little easier by setting your graduate up with a budgeting program of their choice. There are a number of apps and online programs available that are designed to help make money management simpler and more intuitive. If you already use one, consider walking your graduate through the program you prefer. If not, take an afternoon with your grad to look at several options to find one that works for them. While many budgeting apps are free, some charge a monthly or annual fee. If your graduate is interested in one of the paid apps, you might offer to pay for it as long as they continue to use it. It will be an investment that saves both of you money in the long run. Open a Roth IRA account Setting money aside for a retirement 40-plus years in the future is probably the last thing on your graduate’s mind, but that’s partly what makes this is such an impactful gift. The earlier you contribute money to a Roth IRA, the more time you give it to let compounding interest do its incredible magic. A brand-new adult is also in an excellent position for a Roth IRA for another reason: Roth accounts are funded with after-tax dollars. Instead of deducting contributions to these accounts from your income, you contribute money you’ve already paid taxes on into your Roth accounts. The money grows tax-free, and you can withdraw it tax-free in retirement. Here’s why this is so great for young’uns: A new graduate’s tax burden is probably the lowest one they will ever have. Making Roth IRA contributions now, while the new graduate is at a low tax bracket, means paying very little in taxes on the invested money. As of 2026, a young adult can contribute up to $7,500 annually into a Roth IRA, provided they have earned at least that much. (Also, these yearly contribution limits encompass all IRAs you may own. If your graduate has a traditional IRA and a Roth IRA, they can’t send $7,500 to each one.) Helping your child open a Roth IRA account and setting up some contributions, even if they’re not able to maximize them, will give them a gift that keeps on giving decades down the line. Launching your graduate New graduates and their families may be understandably alarmed about their financial and career prospects, considering the nonstop coverage of everything good going up in smoke just as they finish their education. This is the same story financial media has been peddling during graduation season for decades—although that doesn’t erase the potential turbulence facing this year’s crop of graduates. However, offering newly graduated students some practical gifts can help prepare them for a tough launch. These gifts include teaching your graduate the soft skills they need to know to navigate the workplace, setting them up with a budgeting app, and helping them open and fund a Roth IRA. Each of these actions will do so much more to encourage, support, and guide your graduate than any tangible gift, even a picture book by a beloved author. View the full article

-

RETN started with a bold ambition to build a nine-figure business. After doubling our revenue to nearly $80 million in the last five years, that goal is now within close reach. But it’s taken more than a daring founding team to get us to this point. This is all due to our engineers, sales, and support staff, who share a desire to grow and achieve exceptional results. As a team, we believe a business is only as strong as its weakest link. Poor components can cause bottlenecks and compromise performance. To maintain our strong network, we’re meticulous about hiring, no matter the role. And these three questions help us identify exceptional talent to maintain our growth. Why did you leave your first real job? People leave jobs for many reasons. Some become frustrated with a lack of learning, and others prefer fast growth over steady progress. Some want more compensation. Others find it difficult to retain interest in a project. None of those reasons is inherently bad. What matters, and what you need to find out, is whether a candidate’s needs and approach align with your company and the role. After all, turnover is expensive. The average cost of replacing an employee has jumped to over $45,000 in the past year, up from $37,000, according to the most recent express employment professionals-Harris Poll survey. And that doesn’t account for the lost momentum and slowed progress during search, training, and onboarding. To avoid unnecessary costs to your finances and productivity, you need to glean what energizes and frustrates a person, as well as the kind of environment they need to thrive, before you hire them. A mixed role might suit somebody who struggles with monotony and enjoys wearing multiple hats, while a highly structured role would work better for a candidate who thrives on routine. The best candidate on paper isn’t necessarily the best fit, and the wrong or right answer will always depend on the role. What do you know about our company? Many applicants use a ‘spray and pray’ approach—they send off hundreds of low-effort applications, recycling the same resume and cover letter. These candidates aren’t interested in working for you. They want a job, an improved salary, or a better title. They’re not interested in learning and growing within the company. They’re also likely to bolt as soon as they spot an opportunity for quick progress, even if it harms their long-term growth. I don’t choose employees who apply for every role and take whatever comes their way. It can be difficult to spot them from an application alone, but the level of research (or lack of) they’ve done before the interview can be incredibly telling. Asking the right questions is another clear indication of a committed candidate. While most ask about our flexible working policies or whether I enjoy working at the company, exceptional candidates are curious about operations, challenges, and opportunities to grow. Here are examples of some questions that some high-performing candidates have asked me during the interview process: “How can I succeed beyond just hitting revenue targets?” “Will I be mentored in my role, and can I expect feedback?” “Are junior staff given a chance to offer input and ideas?” “Do you hire from within, and what roles have previous team members moved into?” “Is the position stable, and are you likely to cut numbers in the near future?” We’re looking for candidates who have done their research, want a clear picture of the environment they’re joining, and are planning how they will grow within the company before they’ve even received an offer. What do you think about using technology at work? We don’t expect every hire to be a tech wizard, but they need to have a positive attitude towards innovation and change. In the modern workplace – where collaboration, communication, and problem-solving rely heavily on technology – it’s nearly impossible to thrive without it. It’s helping everyone to work smarter, and the best candidates recognize that. Truly exceptional candidates don’t answer this question by talking about the tools they were required to use in their previous role. They share stories of experimenting with new solutions to save time. And they tell you about the exciting developments in your space that they could use to improve results. Not because the company demands it, but because they see the value it could offer. In my experience, these employees are highly adaptable, brush off hardship, and get on with the job. These are useful qualities to have on your team during times of rapid change. Companies that encourage experimentation and grant autonomy to their teams to try new things are 60% more likely to be innovation leaders. And as history shows, innovative companies have better odds of survival. Much more so than a team that insists on sticking to ‘the way they know’. The best interview questions reveal who you’re really hiring For me, interviews shouldn’t focus on a candidate’s qualifications. That’s what their resume and references are for. Instead, it’s about finding out how they think, what motivates them, and whether they suit your team. Skills are something you can teach, However curiosity, drive, and resilience are all attributes is much more difficult to train. View the full article

-

If you’re considering transforming your business into an S Corporation, it’s essential to understand the steps involved. First, you’ll need to confirm your eligibility and decide on the right business structure. This process includes filing the necessary forms and ensuring compliance with state and federal regulations. By following these steps, you can take advantage of the benefits associated with an S Corporation. Let’s explore the specific actions you need to take to make this change successful. Key Takeaways Confirm eligibility by ensuring your business is a domestic corporation or LLC with 100 or fewer U.S. citizen shareholders. Choose the appropriate business structure, considering the management flexibility of an LLC versus the structured appeal of a corporation. File IRS Form 2553 to elect S Corporation status, ensuring all shareholders consent to the election. Maintain proper documentation, including meeting minutes and operating agreements, reflecting the intention to elect S Corporation status. File annual IRS Form 1120S and provide Schedule K-1 forms to shareholders, ensuring compliance with tax obligations. Confirm Your Eligibility for S Corporation Status Before you can elect S Corporation status for your business, it’s essential to confirm your eligibility based on specific IRS requirements. First, verify your business is a domestic corporation or an LLC. You’re limited to a maximum of 100 shareholders, all of whom must be U.S. citizens or residents; partnerships and corporations can’t be shareholders. Furthermore, your business can only issue one class of stock, meaning all shares must have identical rights regarding distribution and liquidation proceeds. Certain entities, like financial institutions and insurance companies, are ineligible for S Corporation status. All shareholders must consent to the election, which requires you to file Form 2553 with the IRS within the designated time frame. Comprehending how to become an S Corporation is essential, especially if you intend to deal with S Corporation 1099 forms for tax reporting. Confirming your eligibility guarantees a smoother shift to this beneficial status. Choose Your Business Structure When choosing your business structure, you’ll need to weigh the pros and cons of forming an LLC versus a Corporation. Each option has its own shareholder limitations and tax implications, which can greatly affect your business’s financial health. Comprehending these differences is essential as you prepare to elect IRS Corporation status and guarantee compliance with IRS regulations. LLC vs. Corporation Comparison Choosing the right business structure is crucial for your venture, and comprehending the differences between an LLC and a corporation can help you make an informed decision. Here are three key points to reflect upon: Flexibility vs. Structure: An Flexibility offers more management flexibility and fewer formalities, whereas corporations have structured management, which can attract investors. Taxation Benefits: S corporations provide pass-through taxation, similar to LLCs, allowing profits to appear on shareholders’ personal tax returns. This prompts the inquiry: do S corporations get a 1099? Yes, they do, but the S corp 1099 reporting differs from traditional corporations. Ownership Complexity: Corporations can issue multiple classes of stock, offering complex ownership structures that may appeal to investors more than an LLC. Understanding these differences can guide you in selecting the best structure for your business. Shareholder Limitations Explained Grasping the shareholder limitations of an S Corporation is vital if you’re considering this business structure for your venture. An S Corporation can have a maximum of 100 shareholders, which keeps ownership manageable. Significantly, all shareholders must be individuals, certain trusts, estates, or exempt organizations—corporations and partnerships can’t hold shares. Moreover, shareholders must be U.S. citizens or residents, ensuring that ownership remains domestic. The corporation can only issue one class of stock, which simplifies the capital structure but limits fundraising flexibility. Finally, obtaining consent from all shareholders for the S Corporation election is important, highlighting the significance of agreement among owners. Limitation Details Max Shareholders 100 Eligible Shareholders Individuals, certain trusts, estates Stock Classes Only one class allowed Tax Implications Overview Comprehending the tax implications of choosing an S Corporation as your business structure is crucial for effective financial planning. Here are three key points to evaluate: Pass-Through Taxation: S Corporations allow profits and losses to pass directly to your personal tax return, avoiding double taxation faced by C Corporations. Tax-Free Dividends: Shareholders may receive dividends that can be tax-free if specific IRS criteria are met, enhancing your financial flexibility. Reasonable Salary Requirement: You must pay yourself a “reasonable salary,” which is subject to payroll taxes but can lower your overall self-employment tax liability. Be mindful that failing to comply with IRS requirements can jeopardize your S Corporation status, reverting you to C Corporation taxation. Obtain an Employer Identification Number (EIN) Obtaining an Employer Identification Number (EIN) is a fundamental step in establishing your S Corporation. This unique nine-digit number, assigned by the IRS, identifies your business entity for tax purposes. You can apply for an EIN online through the IRS website, by fax, by mail, or even by phone if you’re an international applicant. The online process is particularly efficient, providing your EIN immediately upon completion for U.S.-based entities. There’s no fee to apply, making this an accessible step for any entrepreneur. You’ll need your EIN to open a business bank account, hire employees, and file tax returns, so it’s imperative to keep it secure. Furthermore, you’ll use your EIN when filing your S-Corporation election using Form 2553. Make sure to safeguard this number, as it plays a crucial role in your company’s legal and tax-related activities. Update Your Operating Agreement Updating your operating agreement is a vital step in solidifying your S Corporation status. This document must reflect your intention to elect S Corp status and adhere to IRS regulations. To guarantee compliance, consider making these important changes: Revise Tax Provisions: Modify any sections initially drafted for partnership taxation, as these may conflict with S Corp requirements. Define Shareholder Roles: Clearly outline the roles, rights, and responsibilities of each shareholder, confirming all consent to the S Corp election. Streamline Stock Classes: Remove any references to multiple classes of stock; S Corps can only issue one class. It’s advisable to consult with a legal professional to review and adjust your operating agreement. This step helps you avoid potential issues with the IRS and guarantees your business remains compliant during the shift to S Corporation status. File IRS Form 2553 Filing IRS Form 2553 is a significant step in officially electing S Corporation status for your business. To do this, you’ll need the consent of all shareholders, which is critical for the election. Make certain to submit the form by the 15th day of the 3rd month of the tax year for which you want the election to take effect, typically March 15 for calendar-year entities. Form 2553 requires basic information about your corporation, including its name, address, and Employer Identification Number (EIN). It’s essential to guarantee that your corporation meets the eligibility criteria for S Corporation status, such as having no more than 100 shareholders and only one class of stock. After submitting the form, you should receive a confirmation from the IRS, indicating your S Corporation election’s acceptance, which is important for compliance and future tax benefits. Comply With State Requirements Complying with state requirements is crucial for your S Corporation to operate without legal issues. Before you elect S Corporation status, confirm your business is registered as either a corporation or an LLC in accordance with state laws. Here are three critical steps to follow: Verify State-Specific Requirements: Check if your business meets the specific requirements for S Corporations in your state, which may include filing necessary documents or obtaining licenses. Consult State Officials: Reach out to your state’s Secretary of State’s office for accurate information regarding regulations, as these can vary considerably from state to state. Understand Tax Obligations: Confirm compliance with any state tax obligations, as some states may impose separate requirements for S Corporations beyond federal regulations. Additionally, maintain proper documentation, such as meeting minutes and operating agreements, to demonstrate your adherence to both state and IRS requirements for S Corporation status. Maintain Ongoing Compliance and Reporting Maintaining ongoing compliance and reporting is vital for the successful operation of your S Corporation. Each year, you must file IRS Form 1120S by the business tax deadline, typically March 15. This form reports your corporation’s income, gains, losses, deductions, and credits. Furthermore, you need to provide Schedule K-1 forms to shareholders, detailing their share of the corporation’s income for their individual tax returns. If you have shareholder-employees, guarantee you pay them reasonable salaries, which are reported on W-2 forms and are subject to payroll taxes. You may likewise need to make quarterly estimated tax payments if your S Corp expects to owe $500 or more when filing its return. Finally, remember to comply with state-specific regulations, as state tax return requirements and deadlines can differ greatly from federal ones, so staying informed is necessary. Frequently Asked Questions How to Start an S Corp Step by Step? To start an S Corporation, you’ll first choose a business structure, like an LLC or corporation, and register your business name with the state. Next, obtain an Employer Identification Number (EIN) from the IRS. Then, file Form 2553 to elect S Corp status, ensuring all shareholders consent. Finally, create an operating agreement outlining profit distribution and stay compliant by filing annual tax forms, including Form 1120S, and managing salary distributions properly. What Is Required to Become an S Corp? To become an S Corporation, you need to start by registering as a corporation or LLC. Then, file IRS Form 2553 to elect S Corp status within the first 75 days of your tax year. Confirm you have no more than 100 shareholders, all of whom must be U.S. citizens or residents. You can only have one class of stock, and your operating agreement must reflect your intent for S Corp taxation. What Is the 2% Rule for S Corp? The 2% rule for S Corporations limits the deductibility of employee benefits for shareholders owning more than 2% of the company’s stock. When you provide benefits like health insurance, you must include these in your gross income, affecting your personal tax liability. The IRS requires you to report these benefits on your W-2 form, ensuring compliance. Comprehending this rule is crucial for managing your tax obligations effectively as an S Corp owner. Can I Set up S Corp Myself? Yes, you can set up an S Corporation yourself. Start by forming a business entity, like an LLC or corporation, by filing the necessary paperwork with your state. After that, obtain an Employer Identification Number (EIN) from the IRS. To elect S Corporation status, file IRS Form 2553 within 75 days of forming your entity. Although you can do this independently, it’s wise to consult legal and tax professionals to guarantee compliance with regulations. Conclusion Becoming an S Corporation involves several key steps, from confirming your eligibility to filing IRS Form 2553. By ensuring you meet the requirements, choosing the right business structure, and maintaining compliance with both federal and state regulations, you can enjoy the advantages of pass-through taxation and limited liability. Staying organized and informed about your ongoing responsibilities will help you maintain your S Corporation status and contribute to your business’s long-term success. Image via Google Gemini This article, "7 Steps to Become an S Corporation" was first published on Small Business Trends View the full article

-

If you’re considering transforming your business into an S Corporation, it’s essential to understand the steps involved. First, you’ll need to confirm your eligibility and decide on the right business structure. This process includes filing the necessary forms and ensuring compliance with state and federal regulations. By following these steps, you can take advantage of the benefits associated with an S Corporation. Let’s explore the specific actions you need to take to make this change successful. Key Takeaways Confirm eligibility by ensuring your business is a domestic corporation or LLC with 100 or fewer U.S. citizen shareholders. Choose the appropriate business structure, considering the management flexibility of an LLC versus the structured appeal of a corporation. File IRS Form 2553 to elect S Corporation status, ensuring all shareholders consent to the election. Maintain proper documentation, including meeting minutes and operating agreements, reflecting the intention to elect S Corporation status. File annual IRS Form 1120S and provide Schedule K-1 forms to shareholders, ensuring compliance with tax obligations. Confirm Your Eligibility for S Corporation Status Before you can elect S Corporation status for your business, it’s essential to confirm your eligibility based on specific IRS requirements. First, verify your business is a domestic corporation or an LLC. You’re limited to a maximum of 100 shareholders, all of whom must be U.S. citizens or residents; partnerships and corporations can’t be shareholders. Furthermore, your business can only issue one class of stock, meaning all shares must have identical rights regarding distribution and liquidation proceeds. Certain entities, like financial institutions and insurance companies, are ineligible for S Corporation status. All shareholders must consent to the election, which requires you to file Form 2553 with the IRS within the designated time frame. Comprehending how to become an S Corporation is essential, especially if you intend to deal with S Corporation 1099 forms for tax reporting. Confirming your eligibility guarantees a smoother shift to this beneficial status. Choose Your Business Structure When choosing your business structure, you’ll need to weigh the pros and cons of forming an LLC versus a Corporation. Each option has its own shareholder limitations and tax implications, which can greatly affect your business’s financial health. Comprehending these differences is essential as you prepare to elect IRS Corporation status and guarantee compliance with IRS regulations. LLC vs. Corporation Comparison Choosing the right business structure is crucial for your venture, and comprehending the differences between an LLC and a corporation can help you make an informed decision. Here are three key points to reflect upon: Flexibility vs. Structure: An Flexibility offers more management flexibility and fewer formalities, whereas corporations have structured management, which can attract investors. Taxation Benefits: S corporations provide pass-through taxation, similar to LLCs, allowing profits to appear on shareholders’ personal tax returns. This prompts the inquiry: do S corporations get a 1099? Yes, they do, but the S corp 1099 reporting differs from traditional corporations. Ownership Complexity: Corporations can issue multiple classes of stock, offering complex ownership structures that may appeal to investors more than an LLC. Understanding these differences can guide you in selecting the best structure for your business. Shareholder Limitations Explained Grasping the shareholder limitations of an S Corporation is vital if you’re considering this business structure for your venture. An S Corporation can have a maximum of 100 shareholders, which keeps ownership manageable. Significantly, all shareholders must be individuals, certain trusts, estates, or exempt organizations—corporations and partnerships can’t hold shares. Moreover, shareholders must be U.S. citizens or residents, ensuring that ownership remains domestic. The corporation can only issue one class of stock, which simplifies the capital structure but limits fundraising flexibility. Finally, obtaining consent from all shareholders for the S Corporation election is important, highlighting the significance of agreement among owners. Limitation Details Max Shareholders 100 Eligible Shareholders Individuals, certain trusts, estates Stock Classes Only one class allowed Tax Implications Overview Comprehending the tax implications of choosing an S Corporation as your business structure is crucial for effective financial planning. Here are three key points to evaluate: Pass-Through Taxation: S Corporations allow profits and losses to pass directly to your personal tax return, avoiding double taxation faced by C Corporations. Tax-Free Dividends: Shareholders may receive dividends that can be tax-free if specific IRS criteria are met, enhancing your financial flexibility. Reasonable Salary Requirement: You must pay yourself a “reasonable salary,” which is subject to payroll taxes but can lower your overall self-employment tax liability. Be mindful that failing to comply with IRS requirements can jeopardize your S Corporation status, reverting you to C Corporation taxation. Obtain an Employer Identification Number (EIN) Obtaining an Employer Identification Number (EIN) is a fundamental step in establishing your S Corporation. This unique nine-digit number, assigned by the IRS, identifies your business entity for tax purposes. You can apply for an EIN online through the IRS website, by fax, by mail, or even by phone if you’re an international applicant. The online process is particularly efficient, providing your EIN immediately upon completion for U.S.-based entities. There’s no fee to apply, making this an accessible step for any entrepreneur. You’ll need your EIN to open a business bank account, hire employees, and file tax returns, so it’s imperative to keep it secure. Furthermore, you’ll use your EIN when filing your S-Corporation election using Form 2553. Make sure to safeguard this number, as it plays a crucial role in your company’s legal and tax-related activities. Update Your Operating Agreement Updating your operating agreement is a vital step in solidifying your S Corporation status. This document must reflect your intention to elect S Corp status and adhere to IRS regulations. To guarantee compliance, consider making these important changes: Revise Tax Provisions: Modify any sections initially drafted for partnership taxation, as these may conflict with S Corp requirements. Define Shareholder Roles: Clearly outline the roles, rights, and responsibilities of each shareholder, confirming all consent to the S Corp election. Streamline Stock Classes: Remove any references to multiple classes of stock; S Corps can only issue one class. It’s advisable to consult with a legal professional to review and adjust your operating agreement. This step helps you avoid potential issues with the IRS and guarantees your business remains compliant during the shift to S Corporation status. File IRS Form 2553 Filing IRS Form 2553 is a significant step in officially electing S Corporation status for your business. To do this, you’ll need the consent of all shareholders, which is critical for the election. Make certain to submit the form by the 15th day of the 3rd month of the tax year for which you want the election to take effect, typically March 15 for calendar-year entities. Form 2553 requires basic information about your corporation, including its name, address, and Employer Identification Number (EIN). It’s essential to guarantee that your corporation meets the eligibility criteria for S Corporation status, such as having no more than 100 shareholders and only one class of stock. After submitting the form, you should receive a confirmation from the IRS, indicating your S Corporation election’s acceptance, which is important for compliance and future tax benefits. Comply With State Requirements Complying with state requirements is crucial for your S Corporation to operate without legal issues. Before you elect S Corporation status, confirm your business is registered as either a corporation or an LLC in accordance with state laws. Here are three critical steps to follow: Verify State-Specific Requirements: Check if your business meets the specific requirements for S Corporations in your state, which may include filing necessary documents or obtaining licenses. Consult State Officials: Reach out to your state’s Secretary of State’s office for accurate information regarding regulations, as these can vary considerably from state to state. Understand Tax Obligations: Confirm compliance with any state tax obligations, as some states may impose separate requirements for S Corporations beyond federal regulations. Additionally, maintain proper documentation, such as meeting minutes and operating agreements, to demonstrate your adherence to both state and IRS requirements for S Corporation status. Maintain Ongoing Compliance and Reporting Maintaining ongoing compliance and reporting is vital for the successful operation of your S Corporation. Each year, you must file IRS Form 1120S by the business tax deadline, typically March 15. This form reports your corporation’s income, gains, losses, deductions, and credits. Furthermore, you need to provide Schedule K-1 forms to shareholders, detailing their share of the corporation’s income for their individual tax returns. If you have shareholder-employees, guarantee you pay them reasonable salaries, which are reported on W-2 forms and are subject to payroll taxes. You may likewise need to make quarterly estimated tax payments if your S Corp expects to owe $500 or more when filing its return. Finally, remember to comply with state-specific regulations, as state tax return requirements and deadlines can differ greatly from federal ones, so staying informed is necessary. Frequently Asked Questions How to Start an S Corp Step by Step? To start an S Corporation, you’ll first choose a business structure, like an LLC or corporation, and register your business name with the state. Next, obtain an Employer Identification Number (EIN) from the IRS. Then, file Form 2553 to elect S Corp status, ensuring all shareholders consent. Finally, create an operating agreement outlining profit distribution and stay compliant by filing annual tax forms, including Form 1120S, and managing salary distributions properly. What Is Required to Become an S Corp? To become an S Corporation, you need to start by registering as a corporation or LLC. Then, file IRS Form 2553 to elect S Corp status within the first 75 days of your tax year. Confirm you have no more than 100 shareholders, all of whom must be U.S. citizens or residents. You can only have one class of stock, and your operating agreement must reflect your intent for S Corp taxation. What Is the 2% Rule for S Corp? The 2% rule for S Corporations limits the deductibility of employee benefits for shareholders owning more than 2% of the company’s stock. When you provide benefits like health insurance, you must include these in your gross income, affecting your personal tax liability. The IRS requires you to report these benefits on your W-2 form, ensuring compliance. Comprehending this rule is crucial for managing your tax obligations effectively as an S Corp owner. Can I Set up S Corp Myself? Yes, you can set up an S Corporation yourself. Start by forming a business entity, like an LLC or corporation, by filing the necessary paperwork with your state. After that, obtain an Employer Identification Number (EIN) from the IRS. To elect S Corporation status, file IRS Form 2553 within 75 days of forming your entity. Although you can do this independently, it’s wise to consult legal and tax professionals to guarantee compliance with regulations. Conclusion Becoming an S Corporation involves several key steps, from confirming your eligibility to filing IRS Form 2553. By ensuring you meet the requirements, choosing the right business structure, and maintaining compliance with both federal and state regulations, you can enjoy the advantages of pass-through taxation and limited liability. Staying organized and informed about your ongoing responsibilities will help you maintain your S Corporation status and contribute to your business’s long-term success. Image via Google Gemini This article, "7 Steps to Become an S Corporation" was first published on Small Business Trends View the full article

-

In order for a chatbot to become more intelligent, and thus more useful to the end-user, it needs to assimilate data continuously. This process is known as “training.” The problem is that many AI companies never explicitly ask for consent from data owners before scraping their webpages and adding the data to the corpora of the large language models (LLMs) that power AI chatbots. But some of those data owners, also known as content creators or IP holders, are now fighting back. They are doing this by using tools known as “tarpits.” Their aim? To poison the chatbot’s underlying LLM and thus degrade the quality of its outputs, potentially causing end-user flight. Here’s what you need to know. What is AI poisoning? AI poisoning is the process of corrupting an AI chatbot’s underlying large language model so that the chatbot gives incorrect, misleading, or utterly bonkers outputs. This corruption is achieved by tricking the LLM into assimilating incorrect data during its training, which often involves scraping every possible website and image it can find. There are many ways an LLM can be poisoned, depending on the capabilities of the LLM that the poisoner wants to disrupt. For example, if someone wanted to poison an image generator LLM, they could use a technique known as “Nightshading,” which involves using a piece of software called Nightshade to add an invisible layer to an image. This layer contains pixels invisible to the human eye but visible to LLM scrapers. These pixels then make the artwork look to the AI as if it’s in a different style than it actually is (say, abstract rather than realistic), which prevents the LLM from mimicking the artist’s actual style. Of course, the majority of chatbots deal with text, not images, rendering poisoning tools like Nightshade useless against unauthorized AI scraping of articles and blogs. But in the last several years, a new type of AI poisoning tools has been making the rounds that aim to trick LLMs into training on useless data. These tools are known as tarpits. What are AI tarpits? AI tarpits are a specific type of AI poisoning tool designed to trick the crawlers that LLMs use into ingesting useless data. Since the LLM then uses this junk data to generate its text outputs, those outputs will be incorrect, which degrades the quality of the AI’s responses and, ultimately, could discourage users from using the chatbot. There are numerous tarpit traps that content creators and IP holders can add to their websites, including Nepenthes, Iocaine, and Quixotic. When an LLM crawler visits a website with the tarpit embedded in its code, the crawler will be redirected to assimilate automatically generated, useless text that is either riddled with incorrect information (e.g., Steve Jobs founded Microsoft in 1834) or completely nonsensical information (e.g., the color of water is pepperoni). Further, these pages of poisoned text will have links linking out to additional pages of poisoned text, none of which have exit links. Thus, much like a physical tarpit causes an animal in real life to get stuck, an AI tarpit traps the LLM crawler into an endless assimilation of incorrect data, unable to exit the trap. How can the average user protect their data from AI companies? Content creators and IP holders use tarpits to waste AI companies’ valuable resources and prevent LLMs from assimilating a website’s data without consent. But even if you aren’t a content creator or IP holder, you should be aware that AI companies are using your data to train their models, too. Every prompt you type into an AI chatbot or conversation you have with it is assimilated into that LLM’s corpus for further analysis with the goal of making the chatbot’s LLM even more robust. The good news is that you don’t have to resort to specialized tools like tarpits to protect your data from chatbots. Instead, you can explicitly instruct chatbots not to train on your data, use chatbots through proxies to obscure your identity, or use everyday software tools to redact your sensitive data before you upload any documents to a chatbot for analysis. View the full article

-

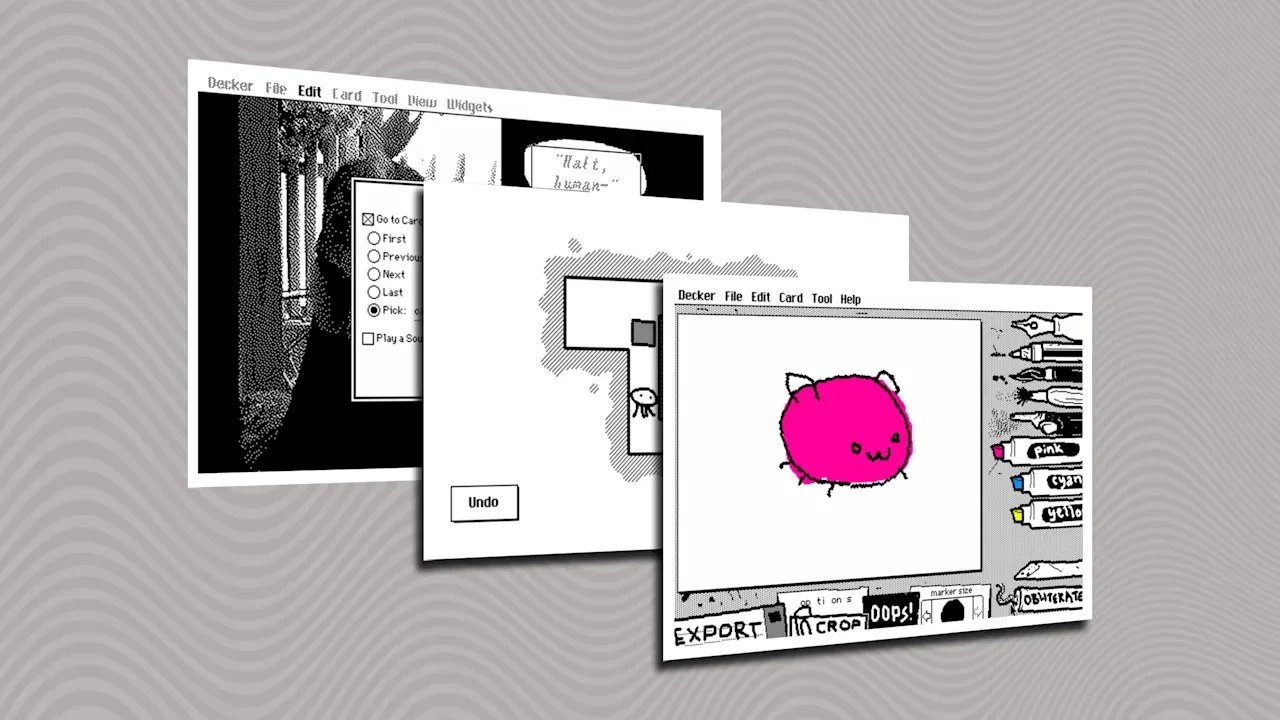

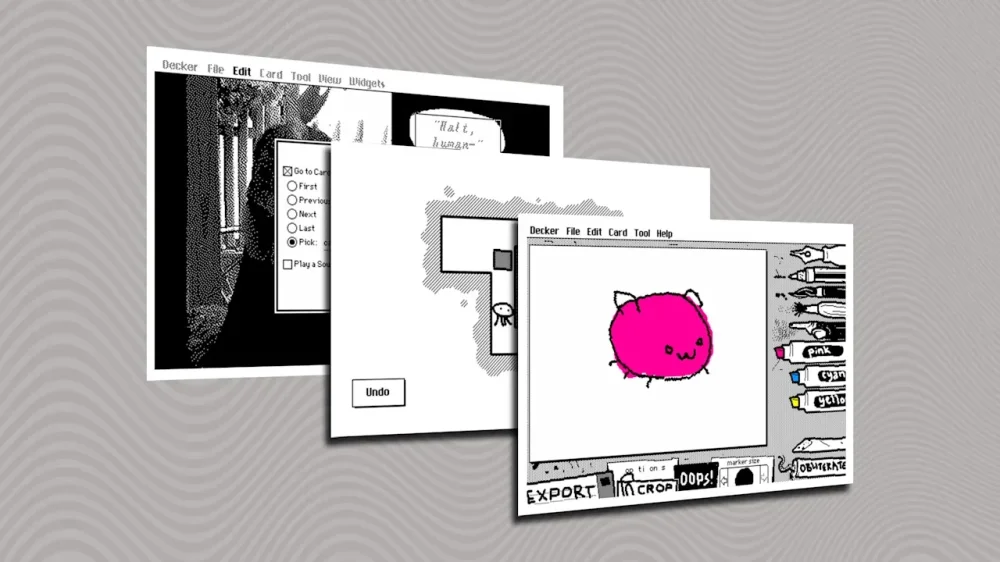

Decades ago, when a classmate and I were supposed to be learning Photoshop in our high school computer lab, we stumbled upon something much cooler—and weirder. The program was called HyperCard, from Apple, and it let you create interactive presentations with multiple choice buttons and branching pathways. We quickly started using it to craft crude choose-your-own adventure games when the teacher wasn’t looking. HyperCard could have become something bigger if Apple hadn’t abandoned it, which is a whole other story. The point of this article, though, is to let you know about a spiritual successor that enables all kinds of modern uses despite its old-school aesthetic—on whatever kind of device you’re using. This tip originally appeared in the free Cool Tools newsletter from The Intelligence. Get the next issue in your inbox and get ready to discover all sorts of awesome tech treasures! Interactive documents, retro-style To bring back the glory of HyperCard on modern devices, check out Decker. ➜ Decker is a desktop app for creating interactive documents, presentations, and games. ⌚ It takes five or 10 minutes to learn the basics well enough to start putting a presentation together. 💸 And it’s available for free or under a pay-what-you-can model. You can also try a web-based version without installing anything. ✅ Let’s start with the download first: Head to the official Decker download page, then scroll down and click the “Download Now” button. You’ll see a few payment options if you want to support the developer, or you can click “No thanks, just take me to the downloads” instead. Then choose either the “mac” or “win” version to download (or, again: If you’re using a phone or another type of device, head over to the web version instead). In Windows, you can extract the ZIP file to any folder you like and run the decker.exe file, as it’s a portable app with no need to install anything. For the Mac version, extract the ZIP file and move the Decker.app file to your Applications folder. ☝️ Decker is safe to use, gets regular updates, and has an active community of users—but because the app isn’t notarized, it runs afoul of the Windows and Mac safety filters. In Windows, hit “Run Anyway” when prompted. For the Mac version, head to System Settings > Privacy & Security, then select “Open Anyway” next to the message about Decker being blocked. You’ll only have to do this once. 🖌️ With all that out of the way, you can start making things. While the app has a “Guided Tour” that demonstrates its main features, I suggest doing the following: Head to File > New Deck and hit “Discard” for a clean slate. Under the “Tool” tab, select “Widgets.” Under the “Widgets” tab, select “New Button.” Double-click the button, and write something in the Text field, like “Next Page.” Click the “Action…” button, select “Next,” then hit “OK.” Head to File > New Card. Under the Widgets tab, create a new button again, set the Text to something like “Previous Page,” then hit the “Action…” button and select “Previous.” Head to Tool > Interact, so the buttons become clickable. Now, you should have two pages, each with a button for flipping back and forth between them. This is the essence of Decker: creating documents with interactive buttons for jumping around to different pages. 💡 From there, you can try some different things to dress up your pages: In the Tool tab, use the various drawing tools such as Line, Pencil, and Box. Make another button, but this time set it to “Invisible” and draw your own custom button art around it. Try adding some other types of objects from the Widgets menu, such as text fields, sliders, and canvases to draw on. Decker also includes its own scripting language called “Lil,” which can add even more layers of interactivity to your documents. For instance, you can have a button that adds to a counter, which then loads another card when the counter exceeds a certain level. It’s even possible to create entire games in Decker this way. If you want to dive deeper into Decker’s capabilities, I suggest loading some of the files in the “Examples” folder or on the Decker website. Like any other Decker document, you can edit these examples to see how they work. Once you’ve finished making a document, head to File > Save As to export it. The default file format is .deck, but you can also change the extension to .html, which lets you load the document in any web browser. Yes, that means you can make any document public by uploading the .html file to your personal website, if you have one. Much like the original HyperCard, it’s surprising how much you can do with this little program. Who knows? You might even end up building the next Myst. Decker is available for Windows and Mac, and you can try it online, too. The app is free to download with an optional donation. Decker is open-source software, does not require an internet connection, and does not collect any user data. Treat yourself to all sorts of brain-boosting goodies like this with the free Cool Tools newsletter—starting with an instant introduction to an incredible audio app that’ll tune up your days in truly delightful ways. View the full article

-

Below, David Epstein shares five key insights from his new book, Inside the Box: How Constraints Make Us Better. David is the author of The New York Times bestsellers Range and The Sports Gene. He has worked as a senior writer for Sports Illustrated and an investigative reporter for ProPublica. What’s the big idea? Using deliberate constraints and simplification strategies helps you focus better, be more productive, and make more creative decisions. Listen to the audio version of this Book Bite—read by David himself—in the Next Big Idea App, or buy the book. 1. Make all your current commitments visible. At one genomics lab, the staff took the time to write each of their current projects on Post-it notes (one project per Post-it) and put them up on a wall. They immediately noticed that they had way too many things in progress at once. The lab team saw the importance of picking priorities to focus on. Making all your commitments visible is a useful exercise. This can be done for personal matters, professional tasks, or both. When taking account of everything, ask yourself, “If I had to cut one of these things out in the next 90 days, which would it be?” That doesn’t mean you have to kill it forever, but maybe you put it on hold because constraints can help clarify your priorities. That’s what this exercise is about. Most people or teams who do this realize that they’re overcommitted and that a lot of medium-priority tasks are competing with top-priority tasks. Humans are bad at taking things away. So think of this exercise as a subtraction audit. We have a bias called subtractive neglect bias, meaning we overlook solutions that involve taking things away. Do this regularly to actively reduce obligations rather than only accumulating more. 2. Batch your email. Psychologist Gloria Mark has spent two decades observing people at work to understand what they do all day. In one of her more recent studies, she found that people in offices check email about 77 different times a day. That’s the average. And that leads to lower productivity and higher stress. New evidence suggests that this kind of frequent toggling might even affect immune function, but we do know it affects stress, because switching tasks frequently causes the quality and pace of work to drop. Less gets done, and it’s not done as well. Dr. Mark likes to describe the brain as a whiteboard: When doing a task, you’re writing on the whiteboard, and when you switch, you erase, but it leaves a residue that interferes a little bit with the next thing. By toggling back and forth all day, you’re building up that residue and shrinking cognitive bandwidth for each successive task. This isn’t to say you can’t answer your email, but consider dividing it into one, two, or three batches a day. What you don’t want to be doing is switching back and forth all day long. In fact, if you can batch your work in general, that can be helpful for boosting productivity and lowering stress. “Less gets done, and it’s not done as well.” If monotasking sounds difficult, maybe start your day with 30 minutes of non-toggling work during which you focus exclusively on your most important task. You can gradually work up to longer and longer blocks of time before opening that inbox. Ideally, you can eventually block all your work so that the different types of things you do in a day are done within their own monotask blocks of time. This will increase your productivity and make you feel less stressed at the end of the day. 3. Block the familiar solution. This might be the single greatest creativity prompt. When you block the solution that you’re used to choosing, it forces you to think in new ways. Psychologists sometimes call this a preclude constraint, where you’re precluding whatever the familiar path is to force doing something else. As the cognitive scientist Daniel Willingham has said, you may think that your brain is made for thinking, but it’s actually made for preventing you from having to think whenever possible. Thinking is energetically costly, so your brain wants to do the thing that’s easy. When faced with a problem or a task, your brain will reach for what cognitive psychologists call the path of least resistance, which means something that’s convenient or habitual. But if you want to be creative, you want to block that default. Sometimes it’s blocked by necessity, and that’s why we have the adage that necessity is the mother of invention. When the easy option is not a choice, you’re forced to do something inventive. But if you’re just trying to be more creative, think about whatever you’re doing and block it. Let me give you a sense of how I applied this in some of my own work. When working on this book, I would start new chapters by writing down the first thing that popped into my mind. But then I would say, “Cross that out. I can’t use this as my beginning. I have to find something else.” It was annoying and inconvenient, but it forced me to think hard about what is really the best place to start the chapter, not just the first thing that came to mind. “When the easy option is not a choice, you’re forced to do something inventive.” Whatever your creative task is, don’t jump to the familiar solution. Maybe, at work, consider saying, “If we couldn’t recommend the usual thing at our next client meeting, what would we do instead?” Even if you end up choosing the familiar solution after all, it can be worth exploring the results of this generative, creative prompt before deciding. 4. Start with the box. This is a tip that comes from Tony Fadell. He’s publicly known as the “pod father” because he was the lead designer of the iPod, and then he went on to cofound the smart thermostat company, Nest. The main advice that he gives entrepreneurs is to start by writing the press release before embarking on the project. In fact, at Nest, he had the team prototype the literal box before they had the product. He said, “This will force us to prioritize the things that we’re trying to communicate to the end user. It will force us to clarify what those things are and decide what the priorities are.” Similarly, he suggests that entrepreneurs write a single-page press release as if their project were done. Answer: What do I want this to look like? What problem is it solving? What do I hope people say about it when it’s done? That gives a bounding box for the project. Suddenly, you have guide rails to work within. It doesn’t mean you can’t change them, but if you do, you are aware that you are making thoughtful trade-offs. This can keep a project contained and channeled. I tried this for myself, even just for a few personal projects. I found it a useful exercise that forces you to think about why you’re doing what you’re doing, define your theory of what you’re doing, what you hope it looks like, and what the priorities are. Some people think of it as working backward. These kinds of constraints can be annoying because, as Fadell says, setting boundaries early on slows you down, but they are powerful because they force you to think ahead. I took a cue from Fadell because my previous books had really sprawled, so this time around, I made a full structural outline of the book on a single page. I tried to foil my own system by writing as small as possible, but this exercise forced me to ruthlessly prioritize. As a result, this was the first time I hadn’t written 50% over the length I was allotted for a book. Even though writing this outline slowed me down initially, it drew boundaries that allowed me to write very fast once it came time to execute. I turned the book in early, which is unheard of for me. 5. Set “satisficing” rules and stick with them. Satisficing is a term coined by Herbert Simon, who was a Nobel laureate in economics and one of the founders of AI and cognitive psychology. Satisficing is a combination of satisfy and suffice. What Simon found was that humans cannot optimize their decisions in the way that classical economic theory would have us do because we have limited bandwidth to evaluate different options and predict the future. So, we must satisfy ourselves by selecting good-enough options. Simon suggested that we should proactively set good-enough rules for our decisions, and once those are surpassed, we go with the option and don’t look back. Maybe whatever decision you make or purchase you make or whatever it is goes way beyond the good enough limits, but once you pass them, you go with it. If you’re making a purchase, you establish what you need the item to do, and once you find that option, you take it and move on. The opposite of satisficing is what’s called maximizing. That’s where you’re really trying to evaluate every option and make the best decision. This is like when you’ve found something you’d like to watch on Netflix, but because there might be something better, you keep searching. Dating apps are an obvious example: You find someone you like, but choose to swipe some more anyway, because who knows what’s around the next corner? “Maximizers are less satisfied with their decisions.” Psychology research shows that it’s almost always bad to be a maximizer. Maximizers are less satisfied with their decisions. They’re less satisfied with their lives. They’re much more prone to regret. They prefer reversible decisions, even when they end up happier with irreversible decisions. Just the option to always keep their options open is something that draws them into a certain level of unhappiness. We can all do with a little more satisficing in this world, where it has never been easier to compare every decision and aspect of life to an almost infinite number of other people and other options. It’s important for our well-being to think about and set good-enough rules. Simon himself wore the same brand of socks. He always owned one beret at a time and only bought a new one when the one he had got worn out. He told his daughter that a person only needs three pairs of clothing: one on one’s body, one in the closet ready to wear, and one in the wash. He ate the same breakfast every day. He lived in the same house for 46 years. He famously wrote, “The best is the enemy of the good.” You’d almost accuse him of having low standards if he hadn’t won the highest possible awards in psychology, computing, and economics. Simon recognized that by satisficing, you deliberately save cognitive bandwidth for other areas where it really matters. This article originally appeared in Next Big Idea Club magazine and is reprinted with permission. Enjoy our full library of Book Bites—read by the authors!—in the Next Big Idea app. View the full article

-

During a commencement address at Emory University in Atlanta on Monday, Delta Air Lines CEO Ed Bastian admitted that he used artificial intelligence to write his speech. “Out of curiosity, I asked AI to prepare the address. I was amazed at how quick and easy it was generated,” Bastian told the graduating class of more than 5,000 students. “But I also noticed the lack of soul nor warmth it conveyed,” he said. “It was not my personal voice, and it did not express my genuine appreciation for the opportunity to impart my insights to thousands of you. You want to hear from me, not some algorithm of me. “So, don’t worry,” he told the crowd. “I threw it away, and took pencil to paper.” New grads are facing a turbulent job market that has been completely reshaped by AI, so Bastian’s measured words about the technology likely felt like a breath of fresh air. The CEO was met with a round of applause—a change of pace from the booing some commencement speakers have been subjected to in the last few weeks. For example, at the University of Central Florida last Friday, humanities department commencement speaker Gloria Caulfield, vice president of strategic alliances at Tavistock Development Co., was booed after touting AI as the “next industrial revolution.” Bastian joined Delta in 1998 as its vice president of finance and climbed through the ranks until he became the company’s CEO in 2016. Under his tenure, Delta has grown to surpass a market capitalization of $46 billion. Through his career, he told grads that he’s been faced with making some tough decisions (perhaps such as recently cutting snacks and drinks from hundreds of daily flights). “Doing the right thing comes at a cost,” he told the students. “But I always prefer to think of it as an investment, a smart investment.” “I’ve had many important decisions to make over the course of my career, and I must admit, taking a shortcut or pushing the easy button can sometimes be quite tempting,” Bastian added. “But they never yield an enduring result or an effective solution.” Bastian didn’t promote AI tools or make promises of an “AI revolution.” Instead, he told the members of the graduating class that their most important asset is a “good name.” “It’s your brand,” he said. “It’s what you stand for. And there’s only one person that can take that away from you. That person is you.” View the full article

-