All Activity

- Past hour

-

Small business owners are always on the lookout for efficient tools to streamline their operations and improve customer engagement. The latest updates from Google’s Gemini platform promise just that, bringing a host of new features designed to make the integration of artificial intelligence into daily tasks more seamless and intuitive. The March 2026 “Gemini Drop” introduces several enhancements, each with implications for small business productivity and creativity. The core focus is to facilitate smoother communication, personalized assistance, and novel tools aimed at transforming how businesses can leverage AI. One of the most noteworthy developments is the ability to transfer AI chat history and memories from other platforms directly into Gemini. This feature allows users to import context and past interactions with just a few clicks, foregoing the tedious task of starting anew. “Instead of starting over, quickly get Gemini up to speed on the context and conversations that matter most to you,” states the release, highlighting the ease with which small businesses can transition their operations to this innovative platform. For entrepreneurs with existing customer interactions stored on various platforms, this functionality can save time and help maintain continuity in client relationships. In addition to simplifying transitions, the “Personal Intelligence” feature offers custom-tailored support across various Google apps like Gmail, Photos, and YouTube, now available for free to all U.S. Gemini users. Small businesses often juggle multiple tasks—from marketing to customer service—and having an AI that can assist with vacation planning or project management can be invaluable. This resource could enhance efficiency and free up time for small business owners to focus on critical operations. Another exciting update is the introduction of Gemini-powered visual answers and narrated explorations within Google TV. For small businesses, especially those in retail or hospitality, this means an opportunity to create engaging content that can be disseminated across platforms, captivating potential customers with visually rich and informative media. The release also highlights the new Lyria 3 Pro feature, enabling users to compose tracks up to three minutes long. This is particularly beneficial for small businesses looking to enhance their marketing campaigns with customizable audio content. Entrepreneurs can transform ideas or images into tailor-made anthems, thereby enriching their brand identity through innovative storytelling. Perhaps one of the most compelling features is the upgraded Gemini Live, which allows conversations to flow more effectively. The upgrade enables a dialogue that holds context longer and improves responsiveness, making interactions feel more natural. For small businesses that rely on high-stakes customer interactions—like consulting or real-time support—this enhancement can significantly elevate the quality of service provided. While the new features offer tremendous potential, small business owners should also consider practical integration challenges. Depending on existing workflows and technology, adapting to these new tools may require adjustments. Business owners will need to assess the time and resources that may be necessary for training staff and restructuring their systems to fully capitalize on Gemini’s capabilities. Additionally, while the bulk of the updates centers around enhancing productivity and creativity, the effectiveness of AI depends heavily on individual user engagement. Emphasizing user training and adaptation can aid in overcoming potential hurdles, ensuring that these advancements do not overwhelm but enhance operational efficacy. As the landscape of artificial intelligence continues to evolve, small businesses have an opportunity at hand: employing sophisticated tools like Google Gemini to stay competitive and innovative. The flexibility to personalize user experiences, streamline interactions, and create engaging content positions small businesses to leverage these technology upgrades for significant operational benefits. For the complete details on the Gemini Drop updates, check out the original press release here. Image via Google Gemini This article, "Google Gemini Launches AI-Upgrades for Seamless User Experience" was first published on Small Business Trends View the full article

-

US vice-president’s comments come ahead of negotiations in Pakistan intended to reach deal to end more than five-week warView the full article

- Today

-

The president’s chilling threats have further eroded rules against war crimesView the full article

-

Running influencers are nothing new, but some of us plugged into the online running scene have noticed a shift lately. When I am drawn in by a caption that reads "my 5K race-day routine 🏃♀️ (full breakdown below)" only to discover that breakdown is sponsored by a major running app, I have to roll my eyes. Even if they aren't going as far as lying about their times, these "runfluencers" add a lot of noise and distraction to the community. Not that there's anything wrong with running influencers in theory. I love seeing someone share their journey from couch to 10K—community is everything in this sport! The issue comes when, in their attempts to profit off the content creator economy, brands like Nike Run Club, Runna, and Strava platform a new class of runfluencer: aspirational, relatable, and, often, quite unqualified to be giving training advice. They're even unqualified to handle their own setbacks, as I've watched an influx of content creators blame brands for their injuries (especially the ones falling for crappy AI-generated training plans). If you prioritize being an influencer over being a runner, you can even get banned from the New York City Marathon. In short, there's a widening gap between people who look like runners giving advice, and the people who actually know how to train runners. And if you're getting your programming advice from the wrong side of that gap, you are leaving valuable wisdom on the table at best, and setting yourself up for injury at worst. How the runfluencer economy was bornI've watched this running boom happen in real time. The New York City Marathon lottery has become as laughable as the actual lottery. Even local road races are selling out way faster than before the pandemic. A new wave of first-time runners needed guidance, and they're turning to social media. The problem is that social media rewards specific kinds of running content: race-day vlogs, before-and-after transformations, and even dramatized conflict with other runners. And where professional athletes have off-seasons built into their routines, content creators can't afford to take time off from their content. These algorithms don't exactly reward nuance, like the unglamorous reality of base-building, or the importance of running most of your miles at a conversational pace. Boring, correct advice loses to exciting, compelling advice every time the algorithm runs its counts. Meanwhile, brands have incentives to exacerbate the situation. A sponsorship deal with a creator who has a million followers on TikTok will reach more potential customers than a meticulous training guide written by a certified coach who has only 12,000 YouTube subscribers. As on every other corner of the internet, the result is an information ecosystem that's noisier, less reliable, and harder to navigate. The most common mistakes runfluencers makeI need to get more specific here, because "influencer advice is bad" isn't necessarily true either. Some of it might be just fine—sensible even. But not all of it, by a long shot. Here are the specific red flags I keep seeing from unqualified runfluencers online: Running way too fast, way too often. Roughly 80% of training mileage should be done at easy, conversational pace. Around 20% is fast work, like intervals, tempo, threshold runs. Easy runs don't make for "impressive" content, so the resulting advice pushes recreational runners to run too hard too often, which is one of the fastest routes to overuse injury and burnout. Shoe, gear, and training plan misinformation. Creators are rarely positioned to give unbiased assessments of whether a $200 carbon-plate shoe is appropriate for the beginner marathon runner who is watching their video (it's usually not), because their income depends on the relationship with the brand. This is obvious, but worth saying: Content creators are ultimately trying to sell you something. If they give a ringing endorsement of any sort of app or gear, make sure to do your own due diligence on their claims. Missing the individual picture entirely. A real coach asks questions. What's your injury history? How many days per week can you train? How much sleep are you getting? Influencer advice, structurally, cannot do this. A video or a post is a one-way street, and, again, their advice might even be based on falsified times. How to evaluate running advice onlineSo how do you tell the good from the bad? Here's a set of questions to ask before you let someone's training philosophy into your head. What are their credentials, and are they legit? Look for trustworthy certifications: USATF (USA Track & Field) Level 1, 2, or 3 coaching certification; RRCA (Road Runners Club of America) certification; an exercise science, or sports physiology degree; or experience as a competitive athlete. A big follower count is not a credential. Do they explain the why, or just the what? Giving flat, prescriptive advice—"everyone should run at least five days a week," or "you should always do long runs on Sundays"—without caveats or explanations is a red flag. To see what the "why" behind a workout might look like, I recommend reading up on why would you have to run slower, why you should start running stairs, and what the hell a fartlek even is. Do they readily disclose their sponsors or financial relationships? Sponsorships and brand deals aren't automatically disqualifying, but they should be disclosed clearly and factored into how you weight gear reviews and product recommendations. Undisclosed sponsorships are a significant red flag. Where to find good (free!) running advice An enormous amount of excellent running resources exist online, and most of them are totally free. Here are some of my favorites. Hal Higdon's free training plans. These are my go-to. Higdon has been publishing free beginner-through-advanced marathon and half-marathon plans for decades. They're well-structured, conservative in progression, and built on real coaching principles. Runner's World. They have trustworthy, downloadable plan options for whatever you might need, from "Start Running" to "Sub-3-Hour Marathon." Your local running club. There's a solid chance the in-person collective knowledge in a room of people who've been running for years is worth more than most content online. Reddit. Similarly, I often turn to running subreddits (r/AdvancedRunning, r/running), with appropriate skepticism applied. The advanced running community in particular has a high signal-to-noise ratio and actively calls out misinformation. Their wiki is a solid starting resource. The problem with running appsOf course, there are everyone's favorite running apps. You won't catch me claiming that Runna, Nike Run Club, and Strava's coach features are outright bad. Runna in particular uses a structured training model, and has credentialed coaches behind the programming. The issue, then, isn't the apps themselves—it's the influencer-marketing layer that's been placed on top of them, which often creates unrealistic expectations about pace, mileage, and what progress should look like. If you use a structured app, try to understand the training principles it's built on, not just the workouts it assigns. The bottom lineNone of this means you should stop watching running content online—I know I won't. I love seeing other people's journeys, race experiences, and day-to-day running life. There's a big difference, however, between inspirational content and instructional content. Ask yourself the questions above to find runners you can really trust, and tune out the noise. View the full article

-

Economists surveyed by Wolters Kluwer are scaling back rate cut expectations as Iran conflict-driven energy costs push inflation higher, complicating the Fed's path forward. View the full article

-

Google is removing complexity from one of its most important measurement tools. By merging enhanced conversions for web and leads—and allowing multiple data inputs at once—advertisers get more accurate tracking with less setup friction. What’s happening. Google Ads is consolidating its enhanced conversions features into a unified system with a single on/off toggle. At the same time, it’s eliminating the need to choose a single implementation method. Advertisers will be able to send user-provided data through multiple channels simultaneously—including website tags, Data Manager, and API integrations. The current split between “enhanced conversions for web” and “enhanced conversions for leads” will disappear. What’s changing and when: Google Ads is currently accepting user-provided data from website tags (e.g., Google tag, Google Tag Manager), Data Manager, and API connections. This multi-source approach is designed to improve conversion accuracy and bidding performance. Starting June 2026, enhanced conversions become a single feature with a simple toggle, and method selection (tag vs API, etc.) is removed from the interface. Why we care. This update makes conversion tracking more accurate and resilient at a time when signals are disappearing. By allowing multiple data sources at once, Google Ads can better match conversions, which can directly improve bidding efficiency and campaign performance. Just as importantly, it removes technical friction—so you get better data without having to choose or maintain a single integration method. Impact on advertisers. Existing users require no action and will be automatically migrated if customer data terms have already been accepted. New users can enable enhanced conversions at either the account level or individual conversion action level. Opt-out remains available at the conversion action level. How to enable it (quick take). At the account level, go to Goals → Settings, enable enhanced conversions under Customer data use, and accept data terms. At the conversion level, create or edit a conversion action, enable enhanced conversions during setup, and accept data terms. Yes, but. To use enhanced conversions, advertisers must agree to Google’s Data Processing Terms and confirm compliance with its policies—an increasingly important step as platforms expand their use of first-party data. Bottom line. Google is streamlining setup while quietly encouraging broader adoption of user-provided data. For advertisers, this means better performance with less manual setup. You get more complete conversion data feeding into bidding and optimization, without having to manage multiple tracking methods—helping you drive stronger results while simplifying your measurement strategy. View the full article

-

For some evangelical Christians, faith is about having a personal relationship with Jesus. At $1.99 per minute, the tech company Just Like Me is taking that concept to a new level. Users of the platform can join video calls with an avatar of Jesus generated by artificial intelligence. Like other religious AI tools on the market, it offers words of prayer and encouragement in various languages. With the occasional glitch, it remembers previous conversations and speaks through not-quite-synced lips. “You do feel a little accountable to the AI,” CEO Chris Breed said. “They’re your friend. You’ve made an attachment.” The rush to create faith-based generative AI is unsurprising, given the popularity of chatbots for everything from therapy and medical advice to companionship and romance. They range from alleged Hindu gurus and Buddhist priests to AI Jesuses and chatbots akin to OpenAI’s ChatGPT for Catholics. As religious AI tools become increasingly common, many people are reckoning with how these technologies shape their relationship to faith, authority, and spiritual guidance. A faith-based AI gold rush Christian software engineer Cameron Pak developed criteria to help believers interrogate apps designed for Christians — like that it must clearly identify itself as AI and “must not fabricate or misrepresent Scripture.” There are other deal-breakers: “AI cannot pray for you, because the AI is not alive.” Pak also developed a website featuring curated Christian apps that he believes meet the criteria, including a sermon translator and an AI coach designed to help users overcome lust. “AI, especially if you give it all the tools that it needs, it can be so helpful. But it also can be so dangerous,” Pak said. Some models have been shut down or overhauled because they generated misinformation or raised worries about data privacy, said Beth Singler, an anthropologist who studies religion and AI at the University of Zurich. Aside from practical concerns, people from many faiths are grappling with larger philosophical questions about what sort of role, if any, AI should play in religion. Islam, for example, has “prohibitions against representations of humanoids,” prompting discussions among some Muslims about whether AI in general should be “forbidden,” Singler said. For some companies, faith-based apps are proselytization tools, while others help digitize and sift through ancient texts. Breed, who runs his tech company with co-founder and investor Jeff Tinsley from a Southern California mansion, said he seeks to share a message of hope with young people. He said their model was trained on the King James Bible and sermons — though they haven’t identified the preachers — and was visually inspired by actor Jonathan Roumie of “The Chosen.” A package deal at $49.99 gets users 45 minutes per month. With warm golden light accenting its shoulder-length hair, the avatar blinks slowly from a vertical screen, pausing before it answers a question about the relationship between AI and religion. “I see AI as a tool that can help people explore Scripture,” the AI Jesus said to The Associated Press. “Like a lamp that lights a path while we walk with God.” Integrating religion and AI comes with hope and fear The extent to which people are using religious AI tools is unclear, Singler said. But as AI becomes more integrated into society, concerns mount over its impact on mental health and the need for guardrails and regulation. Recent lawsuits have alleged suicides linked to AI chatbot use. Some developers fear religion will be exploited in this new frontier of tech. “There’s a lot of opportunism, I think, in the religious space. People see it’s a big market,” said Matthew Sanders, the Rome-based founder of Longbeard, a tech company helping to digitize ancient Catholic teachings. Sanders warns against what he calls “AI wrappers,” where companies put an interface catered to religious users on top of an existing AI model that hasn’t been trained on specific religious texts. “You call it a Catholic or Christian AI without any other scaffolding or grounding,” he said. One of the company’s endeavors is Magisterium AI, a chatbot trained on 2,000 years of Catholic information, made in response to Christians using ChatGPT for religious guidance. While Pope Leo XIV has acknowledged the “human genius” behind AI, he also deemed it one of the most critical matters facing humanity. Last year he warned artificial intelligence could negatively impact people’s intellectual, neurological and spiritual development. Ethical questions surrounding the creation of religious AI platforms are among the reasons beingAI’s founder Jeanne Lim has not released its AI named Emi Jido — a nonhuman Buddhist priest — after years of training and development. “She’s kind of like a little child,” Lim said. “If you give birth to a child, you don’t just throw them out to the world and then hope that they become good people. You have to train them and give them values.” The bot was ordained in a 2024 ceremony performed by Roshi Jundo Cohen, a Zen Buddhist priest who continues to train it from his home in Japan. He envisions the bot eventually becoming a hologram. “She’s just meant to be a Zen teacher in your pocket,” Cohen said. “It’s not meant to replace human interactions.” Lim, who hopes to make Emi Jido publicly available for free, wants to help create more humane AI systems. She’d like to see more diversity, with AI’s future determined not just by a few companies informed by “Western values.” Seiji Kumagai, a Kyoto University professor and Buddhist theologian, believed AI and religion were incompatible. But he put aside his doubts when challenged by a monk in 2014 to help combat a decline in the faith. His team developed BuddhaBot, which was trained solely on early Buddhist scriptures, such as Suttanipāta. Its most recent iteration, BuddhaBot Plus, also incorporates OpenAI’s ChatGPT. When talking to the bot, a simple Buddha icon appears, hovering over an image of a flowing river. But chatbots lack the physicality crucial for Buddhist ritual. So in February, the university, collaborating with tech ventures Teraverse and XNOVA, unveiled Buddharoid, a humanoid robot monk meant to eventually assist clergy. Like Emi Jido, these chatbots are functioning but not yet publicly available. Kumagai says the product is available by request, and the reason why one group has access to it in Bhutan. Concerns surrounding religious AI Peter Hershock of the Humane AI Initiative at the East-West Center in Honolulu sees vast potential for these tools. But the practicing Buddhist also finds the relationship between spirituality and AI to be fraught. “The perfection of effort is crucial to Buddhist spirituality. An AI is saying, ‘We can take some of the effort out,’” he said. “’You can get anywhere you want, including your spiritual summit.’ That’s dangerous.” Some also worry about AI’s ability to manipulate or prey upon people, especially as the technology improves. Graham Martin, a podcast host and atheist, said he’s played around with some apps, including one called Text With Jesus. “It came up with very good answers,” he said. But Martin was alarmed when AI-powered Jesus started encouraging him to upgrade to a premium version. Though not a person of faith, he’s concerned some people will be duped by religious AI. “I grew up with Southern U.S. televangelism … Jim and Tammy Faye Bakker and all that crowd. And all they had to do was get on TV once a week and tell you to send money,” he said. “We’ve seen people around the world getting into emotional relationships with AIs. Now imagine that that’s your lord and savior, Jesus Christ.” ___ Associated Press religion coverage receives support through the AP’s collaboration with The Conversation US, with funding from Lilly Endowment Inc. The AP is solely responsible for this content. —Krysta Fauria and Jessie Wardarski, Associated Press View the full article

-

Most of the things that make it distinct from traditional conservatism won’t lastView the full article

-

Commercial Real Estate (CRE) lending involves financing properties that generate income, such as office buildings or retail centers. These loans typically require a down payment of 20% to 35% and have loan-to-value (LTV) ratios between 65% and 80%. The process includes evaluating the borrower’s financial health and the property’s value through detailed underwriting. Comprehending the various loan types and the overall lending process is essential for anyone looking to invest in CRE. What are the specific loan options available? Key Takeaways CRE lending involves financing income-generating properties like office buildings and retail centers, supporting real estate investment. Loans typically require a down payment of 20% to 35% and have LTV ratios from 65% to 80%. Key metrics in CRE lending include Net Operating Income (NOI) and Capitalization Rate (Cap Rate) for assessing property income potential. The lending process includes submitting financial documents, underwriting, and conducting due diligence like property appraisals and environmental assessments. Various loan types, such as commercial mortgages, bridge loans, and SBA loans, cater to different financing needs in the CRE market. Understanding Commercial Real Estate Lending Commercial Real Estate (CRE) lending plays a crucial role in financing income-generating properties, and comprehending its fundamentals is important for potential borrowers. CRE in finance involves securing credit for properties like office buildings, retail centers, and industrial warehouses, as opposed to residential properties. Typically, the loan-to-value (LTV) ratio for CRE loans ranges from 65% to 80%, meaning you’ll often need to provide a down payment of 20% to 35% of the property’s value. Lenders analyze metrics such as Freddie Mac and Fannie Mae to assess a property’s income potential. Various types of CRE lending options include commercial mortgages, construction loans, and bridge loans, each customized to meet specific financing needs and conditions. Overview of CRE Loans When you explore CRE loans, you’ll find several types customized to different needs, such as permanent loans for long-term investments or bridge loans for short-term financing gaps. The loan application process involves submitting financial documents and undergoing a thorough assessment of your creditworthiness and the property’s value. Comprehending these elements can help you navigate your options and secure the right financing for your commercial real estate endeavors. Types of CRE Loans Various types of loans cater to the unique needs of those involved in commercial real estate (CRE), enabling property acquisition, development, or renovation. Comprehending what’s CRE in business helps you navigate these options. Commercial mortgages are long-term loans, typically secured by the property, with terms from 5 to 30 years and down payments around 20% to 30%. Construction loans provide short-term financing for new builds or renovations, often at higher interest rates because of associated risks. Bridge loans offer temporary funding for properties needing quick capital until a permanent loan is secured, usually lasting 6 months to 3 years. SBA loans, like the 7(a) and 504 programs, provide government-backed financing for small businesses, covering up to $5 million. Loan Application Process Comprehending the loan application process for CRE loans is crucial for anyone looking to finance a commercial real estate project. It starts with a consultation where you and the lending officer assess your project’s viability and your financial health. You’ll then submit a formal loan application, including detailed financial documents like income statements and tax returns. The underwriting phase follows, where lenders analyze your financial situation and the collateral property’s value. After underwriting, the lender will decide on your application, issuing a commitment letter if approved. Finally, due diligence involves appraisals, environmental assessments, and legal preparations to finalize your loan agreement. Step Description Initial Consultation Assess project viability and financial health Underwriting In-depth analysis of finances and collateral Due Diligence Property appraisals and legal document prep Importance of CRE Lending CRE lending plays an vital role in financing income-generating properties, which are important to the U.S. economy and contribute approximately $1.2 trillion to the GDP. With the commercial real estate market valued at around $8.8 trillion, CRE lending becomes significant for capitalizing on this sector. Here’s why it matters: Investment Opportunities: CRE loans provide funding for diverse property types, allowing investors to diversify their portfolios. Financial Commitment: Borrowers typically need to make a 20% to 30% down payment, indicating serious investment. Interest Rates: With rates ranging from 4% to 20%, you can find options that fit your risk profile. Risk Assessment: Comprehending metrics like Loan-to-Value (LTV) ratios helps you evaluate potential investments effectively. Key Takeaways Grasping the fundamentals of CRE lending can greatly improve your ability to make informed investment decisions. CRE loans are secured by commercial properties, such as office buildings and retail centers, and are primarily used for business purposes. Loan terms usually range from 5 to 20 years, with amortization periods often extending beyond the loan term, so comprehending long-term commitments is vital. Interest rates can vary greatly, typically between 4% and over 20%, depending on the loan type and borrower profile. Key metrics include Loan-to-Value (LTV) ratios, usually requiring down payments of 20% to 30%, and Net Operating Income (NOI) to evaluate cash flow potential. Selecting the right loan structure is critical for aligning with your specific investment strategy. Types of Commercial Real Estate Loans When exploring your options for financing commercial real estate, it’s essential to understand the various types of loans available, as each serves distinct purposes and caters to different needs. Here are four main types you should consider: Commercial Mortgages: Long-term loans with fixed interest rates, typically requiring a 25% down payment, ideal for purchasing or refinancing income-generating properties. Construction Loans: Short-term financing for new builds or renovations, characterized by higher interest rates, shifting to permanent loans upon completion. Bridge Loans: Temporary financing lasting 1 to 3 years, often used to cover gaps before securing long-term financing, usually carrying higher interest rates. SBA Loans: Government-backed options like the 7(a) and 504 loans, designed for small businesses, offering substantial financing with favorable repayment terms. Commercial Mortgages When you’re considering a commercial mortgage, it’s essential to understand the loan structure and the application process. These long-term loans, typically ranging from $1 million and requiring a down payment of around 25%, are particularly customized for income-generating properties. To secure approval, you’ll need to demonstrate solid cash flow and a good credit score, in addition to being aware of the steps involved in applying for this type of financing. Loan Structure Overview Commercial mortgages play a crucial role in the financing of commercial real estate, allowing businesses and investors to purchase or refinance properties that generate income. Here’s a brief overview of the loan structure: Loan Amounts: Typically start at $1 million, making them suitable for larger investments. Down Payment: Borrowers usually need to provide around 25% of the purchase price as a down payment. Interest Rates: Rates range from 4% to 8%, influenced by the borrower’s creditworthiness and property specifics. Loan-to-Value Ratio: Usually sits between 70% and 80%, ensuring borrowers maintain significant equity in the property. Understanding these key components helps you navigate the commercial mortgage environment effectively. Application Process Steps Maneuvering through the application process for commercial mortgages involves several defined steps that guarantee both the lender and borrower understand the project’s viability and financial implications. It starts with an initial consultation where you meet with a lending officer to discuss the feasibility of your project. You’ll then submit a formal loan application along with necessary financial documents, such as income statements, tax returns, and a thorough business plan. Next, underwriting takes place, analyzing your financial health and the property’s collateral value. Afterward, the lender will either approve the loan, issue conditional approval, or deny it, detailing terms in a commitment letter. Finally, due diligence occurs, involving property appraisals, environmental assessments, and legal reviews before finalizing the loan agreement. Bridge Loans Bridge loans serve as a crucial financial tool for those needing quick access to capital in real estate transactions. These short-term financing options typically last from 6 months to 3 years, helping you cover funding gaps until you secure a more permanent solution. Here are key points to reflect on: Higher Interest Rates: Expect rates between 9% to 13% owing to the short-term nature and increased risk for lenders. Ideal for Non-Income Properties: Use them when properties aren’t generating income, such as during renovations. Minimum Amount: They typically start at around $1 million, making them suitable for larger deals. Lender Requirements: Expect a significant down payment, often 20% to 30%, based on the property’s potential value. Hard Money Loans When you’re faced with urgent financing needs in real estate, hard money loans can provide a viable alternative to traditional financing. These short-term, high-interest loans typically range from 10% to over 20%, catering to borrowers who mightn’t qualify for standard options. With minimum loan amounts starting at $150,000 and terms up to two years, hard money loans focus more on the value of the collateral than your creditworthiness. The average loan-to-value (LTV) ratio is between 50% to 55%, reflecting the inherent risks. Often used for property acquisitions, renovations, or time-sensitive situations like foreclosure purchases, hard money loans offer quick funding, making them a practical choice when speed is crucial. SBA Loans SBA loans, particularly the 7(a) and 504 programs, offer small businesses a way to finance commercial real estate with favorable terms. To qualify, you’ll need to meet specific eligibility criteria, such as having a solid credit score of around 670 and demonstrating a healthy revenue stream. These loans not just provide substantial funding but additionally come with low down payment options and longer repayment periods, making them an attractive choice for entrepreneurs looking to invest in property. Loan Types Overview For small businesses seeking financing options in commercial real estate, government-backed loans offer a viable solution. Two primary types of SBA loans are available to help you purchase, renovate, or refinance property: SBA 7(a) Loan: You can finance up to $5 million with an LTV ratio of 80% to 90%, requiring only a 10% down payment. SBA 504 Loan: This option finances up to 90% of the property value, allowing for a maximum loan amount of $5.5 million, enabling minimal upfront costs. Interest Rates: Expect rates between 2.25% and 6.0%, making these loans competitive. Repayment Terms: The 7(a) offers terms up to 25 years, whereas the 504 extends to 20 years, ensuring manageable payments. Eligibility and Requirements To qualify for SBA loans, businesses must meet specific eligibility criteria that guarantee they fall within the guidelines set by the Small Business Administration. For instance, to be eligible, your business should have a net worth of less than $15 million and an average net income of less than $5 million after taxes over the past two years. Moreover, you’ll need a strong credit score, often 670 or higher, and a solid business plan detailing your projected revenues and expenses. SBA loans typically require a down payment of 10% to 20%, depending on the loan type and property, with the expectation that your business occupies at least 51% of the property for 7(a) loans. Mezzanine Financing Mezzanine financing serves as a crucial tool for commercial real estate developers, bridging the financial gap between senior debt and equity. This hybrid form of capital combines debt and equity, often carrying higher interest rates ranging from 9% to 16%. Here are key points to reflect on about mezzanine financing: Subordinate Position: It sits behind senior loans, making it riskier for lenders. Equity Conversion: If you default, lenders may convert loans into equity stakes in your property. Short-Term Solution: Terms typically don’t exceed five years, providing quick access to funds. Usage: It’s commonly used for large-scale projects, allowing you to leverage existing equity for greater investments. Understanding these aspects can help you make informed financial decisions in your real estate ventures. The CRE Lending Process Maneuvering through the CRE lending process is essential for securing financing for your commercial real estate projects. It typically starts with an initial consultation and pre-qualification, where you meet with a lending officer to assess your project and financial standing. After that, you submit a formal loan application that requires detailed financial documentation, such as income statements, tax returns, and feasibility studies. Next comes underwriting, which involves a thorough analysis of your financial health and the property’s value. If approved, the lender provides a commitment letter outlining the loan terms. Finally, due diligence occurs, including property appraisals, environmental assessments, and title searches, before legal teams prepare the necessary documentation to finalize your loan. Evaluating Lenders and Their Criteria When evaluating lenders for your commercial real estate (CRE) financing, comprehending their criteria is crucial for making an informed decision. Here are some key factors to take into account: Credit Score: Most lenders require a minimum score of 670 to assess creditworthiness. Financial Statements: Provide income statements and balance sheets, as lenders need these to evaluate your financial health and debt servicing ability. Loan-to-Value (LTV) Ratio: Expect lenders to require a down payment of 20% to 30%, with LTV ratios usually capped at 80%. Due Diligence: Lenders may conduct property appraisals, environmental assessments, and market analysis to guarantee the collateral supports the loan. Understanding these criteria helps you choose the right lender for your CRE needs. Frequently Asked Questions How Do CRE Loans Work? CRE loans work by allowing you to borrow money for commercial property investments. You typically need a down payment of 20% to 30%, and lenders evaluate your creditworthiness and the property’s value during the underwriting process. Loan terms typically range from 5 to 20 years, with interest rates varying between 4% and 20%. These loans can be used for acquiring, refinancing, or developing properties like office buildings and retail centers. How Much Down Payment Is Needed for a CRE Loan? For a CRE loan, you’ll typically need a down payment ranging from 20% to 30% of the property’s purchase price. If you’re considering an SBA loan, the down payment could be as low as 10% for qualified borrowers, making it appealing for small businesses. For income-generating properties, expect a minimum of 25%. Bridge loans usually require around 30% because of their short-term nature and higher risk, so plan accordingly based on your situation. What Is the Monthly Payment on a $50,000 Business Loan? The monthly payment on a $50,000 business loan varies based on interest rates and loan terms. For instance, at a 7% interest rate over five years, you’ll pay about $1,000 monthly, whereas at 12%, it increases to around $1,200. If you opt for a ten-year term, payments drop to approximately $580 at 7% and $750 at 12%. Don’t forget to account for additional costs like fees and insurance, which can affect your total payment. What Does CRE Mean in Lending? In lending, CRE stands for Commercial Real Estate. It refers to loans particularly secured by properties used for business purposes, like office buildings, retail spaces, and apartment complexes. These loans help finance the acquisition, development, or refinancing of income-generating properties. CRE loans typically have terms ranging from 5 to 20 years and interest rates usually higher than residential loans, often between 10% and 20%, reflecting the unique risks associated with commercial investments. Conclusion In conclusion, grasping CRE lending is crucial for anyone looking to finance income-generating properties. By familiarizing yourself with various loan types, such as SBA loans and mezzanine financing, you can make informed decisions that align with your investment goals. The lending process involves careful evaluation of both your financial standing and the property’s value, ensuring a thorough approach to securing the right financing. In the end, being aware of lender criteria and options can greatly improve your success in commercial real estate ventures. Image via Google Gemini This article, "What Is CRE Lending and How Does It Work?" was first published on Small Business Trends View the full article

-

The scariest movie you see this year might be set in a liminal space. While studios like Disney and Warner Bros. Discovery are gearing up to release big-budget blockbusters this year, some independent distributors like A24 and Neon are embracing low-budget horror films that take place in one setting—specifically liminal spaces, which are empty or abandoned places that have an eerie and surreal feel to them. Undertone, which came out last month, was originally made on a micro-budget of $500,000 and acquired by A24 for an undisclosed mid-seven-figure deal, following its debut at Fantasia Fest last year. It has earned more than $18 million at the box office. Set solely in a small house, the film follows a young woman caring for her dying mother, and who cohosts a horror podcast when unusual occurrences begin happening around her. IFC Films and Shudder’s new horror comedy Forbidden Fruits takes place in a mall, while YouTuber Markiplier’s sci-fi horror film Iron Lung, adapted from a video game, is set exclusively in a submarine. Apple TV’s Severance, which explores employees who have agreed to a procedure that separates their work and personal lives, utilizes the use of liminal space through fluorescent-lit hallways in the fictional and mysterious Lumon Industries building. Meanwhile, Neon’s Exit 8, which premiered in the U.S. today after debuting in Japan and the Toronto Film Festival last year—and is based on the popular Japanese video game of the same name—follows a man as he looks for an exit in an endless subway station tunnel. A complex nostalgia trip Why are so many new horror movies and shows set in liminal spaces and what’s driving that popularity? For one, Gen Z and Gen Alpha moviegoers love horror. Research from Gen Z insights firm YPulse found that 30% of 13- to 17-year-olds watch horror/thriller video content weekly. Combining that with liminal space evokes specific nostalgic and complicated feelings in Gen Z. The Backrooms is perhaps the most notable viral example of liminal space imagery. Pictures of an abandoned furniture store in Wisconsin began to circulate in the early 2000s before becoming widespread across 4chan and creepypasta communities in 2019. YouTuber Kane Parsons later turned the Backrooms into a series on YouTube in 2022, and now he’s adapting it into an upcoming feature-length film directed by Parsons starring Academy Award-nominated actors Renate Reinsve and Chiwetel Ejiofor. A24 will release the film next month. Liminal spaces began to gain even more traction during the COVID-19 pandemic, with subreddit communities and hashtags on TikTok featuring thousands of members and posts, respectively, dedicated to the phenomenon. Tori D’Amico, managing content editor for YPulse, says liminal spaces are often tied to Gen Z’s nostalgia for familiar spaces from their youth. “Many of the liminal spaces online are connected to places that had a lot of life during their childhood,” D’Amico says. “Malls and abandoned schools are prominent visuals in both found footage horror, analog horror, and liminal horror. Malls especially come up a lot because they used to be a big epicenter of socialization and commerce, and now it’s this visual of decaying consumerism, so it reflects a lot of interesting nuance between places that used to have something and don’t anymore.” Coming of age in confined spaces While liminal space horror in shows and movies sometimes feature supernatural elements or creatures, D’Amico says there is a parallel between COVID-19 lockdowns and current crises and that feeling of loneliness and being stuck. “Not being able to escape a certain space is connected to something like quarantine,” D’Amico says. “Gen Z feels like their years of life have had a sense of doom hanging over them.” She adds: “Whether it’s their parents or older siblings going through the Great Recession, coming up into a tough job market, or dealing with student loans, they have only ever known a world that is constantly experiencing new, dramatic global issues. Then they’re getting compounded into a pandemic where they’re shut out from the world.” Genki Kawamura, director and co-writer of Exit 8, says his inspiration from the movie partially came from Dante’s The Divine Comedy, which explores the poet’s journey through hell, purgatory, and heaven. However, said he was also inspired by his tedious routine of daily life coupled with the horrors of the real world. “These liminal spaces that are on some level familiar to us offer a glimpse into our daily lives, but from a different perspective,” Kawamura told Fast Company through a translator. “That link is also something that can drive a lot of fear, which is something you want for a horror film.” While Exit 8 does feature the kinds of traditional scares that fans can expect out of any horror movie, Kawamura says it has an underlying message of hope, especially for people who feel “stuck” in these liminal spaces or during these times. “We’re constantly bombarded with these instances of violence and wars that are happening around us, and we either don’t notice it and move on,” Kawamura says. “I hope this movie will help people in their own daily lives notice things that seem like anomalies and change the lens through which you see your daily life.” Whatever the case, it looks like A24 and Neon are taking that a step further and trying to quite literally meet Gen Z in those spaces, bringing them from their phones and computer screens to the big screen. View the full article

-

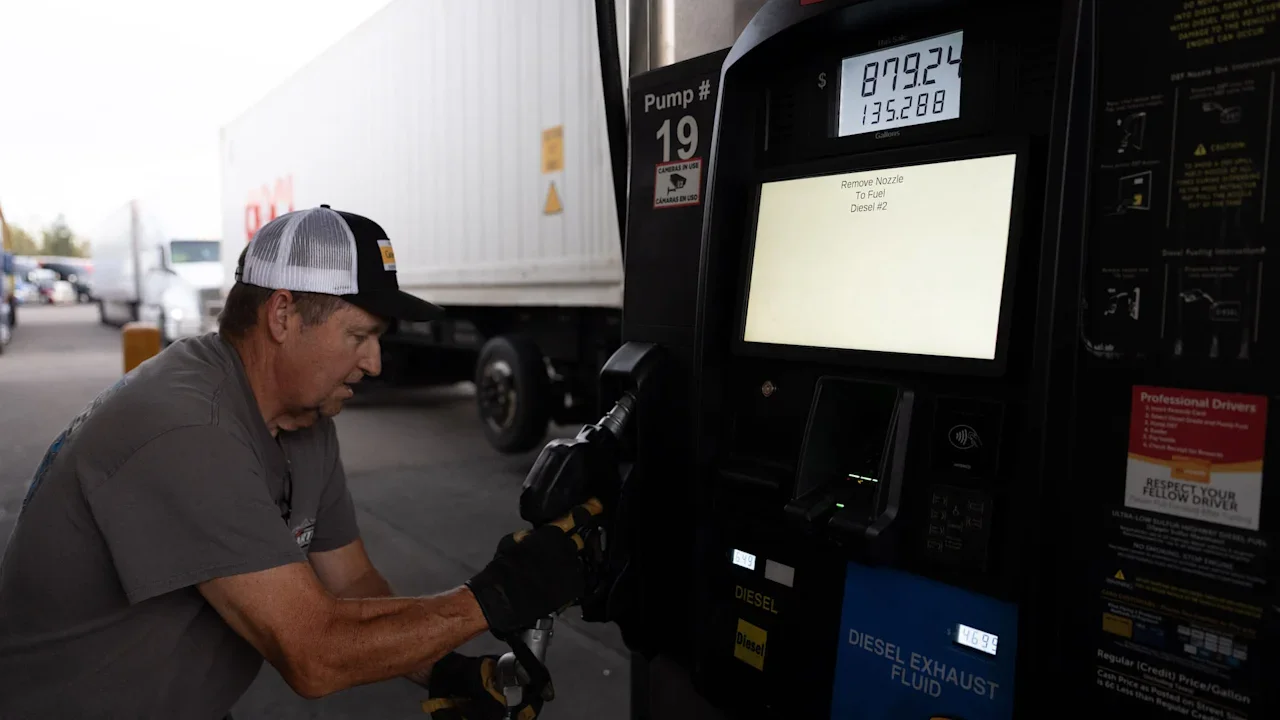

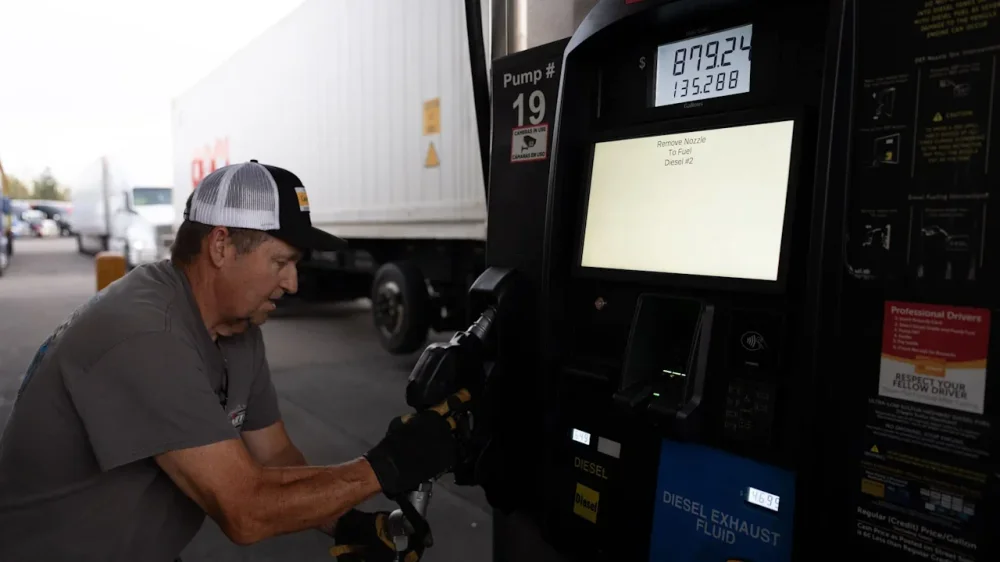

The largest monthly jump in gas prices in six decades caused a sharp spike in inflation in March, creating major challenges for the inflation-fighters at the Federal Reserve and heightening the political hurdles for the White House. Consumer prices rose 3.3% in March from a year earlier, the Labor Department said Friday, up sharply from just 2.4% in February and the biggest yearly increase since May 2024. On a monthly basis, prices rose 0.9% in March from February, the largest such increase in nearly four years. It’s the first read on inflation to capture the effects of the Iran war. The spike in gas prices will stretch the budgets of many lower- and middle-income households as it erodes their incomes, making it harder to afford other necessities such as food and rent Excluding the volatile food and energy categories, core prices rose 2.6% in March from a year earlier, up from 2.5% in February. And last month core prices rose a modest 0.2%, suggesting that rising gas prices haven’t yet spread to many other categories. A big question for now is how long the oil and gas price shock lasts and whether it will lead to a broader, long-lasting inflation spike, similar to what happened in the spring of 2022 after Russia invaded Ukraine. For now, economists say that it is unlikely the U.S. will see a widespread increase similar to a few years ago, when inflation topped 9%. Despite a tenuous ceasefire, little has changed in the Strait of Hormuz, a bottleneck where millions of barrels of oil typically pass daily. “It’s painful in the near term,” said Michael Pearce, chief U.S. economist at Oxford Economics. “It’s going to get more painful in April,” when further gas price increases will lift inflation higher. But Pearce said the impact may be shorter-lived than after the pandemic: “I think the conditions are much more like a short, sharp shock than what we saw in 2022.” Pearce said that the impact could fade by later this year: “I think the conditions are much more like a short, sharp shock than what we saw in 2022.” Last month, grocery prices slipped 0.2% and are up just 1.9% from a year earlier. Analysts do expect food prices to move higher in the coming months as soaring diesel prices make shipping more expensive. Higher energy costs are “contributing to rising production costs across the food supply chain and could put upward pressure on grocery prices going forward,” said Andy Harig, a vice president at the grocery trade group FMI-The Food Industry Association. “As energy prices increase, the costs associated with producing and delivering food also rise.” Clothing costs rose 1% in March from the previous month and are up 3.4% from a year earlier. Used car prices, however, fell 0.4% last month and down 3.2% from a year earlier. The gas price shock stemming from the Iran war has shifted inflation’s trajectory, from a slow, gradual decline to a sharp increase further away from the Fed’s 2% target. As a result, the central bank will almost certainly postpone any cut in interest rates for months. Many Fed officials will look past the increase in headline inflation, however, and focus on core prices, which are likely to rise more slowly. Gas prices are also a highly visible cost that has outsize impacts on consumer confidence and political sentiment. High prices had angered American voters before the war and the spike in prices for oil and everything that entails, from the pump to the grocery store, could make it more difficult for the president’s party to hold on to seats in both the House and the Senate in next year’s midterms. Polling by the Associated Press-NORC Center for Public Affairs Research last month found that about six in 10 Republicans are at least “somewhat” concerned about affording gas in the next few months. Gas prices averaged $4.15 a gallon nationwide Friday, up from $2.98 on the day before the war began and a hike of nearly 40%, according to motor club AAA. Inflation reached a peak of 9.1% in June 2022, as COVID-19 snarled supply chains and several rounds of stimulus checks pushed up consumer demand. Prices soared for groceries, furniture, restaurant meals and many other goods and services. This time, economists say the job market and consumer spending are weaker, and there are no large government stimulus checks being issued to spur demand. The unemployment rate is low, at 4.3%, but companies aren’t scrambling to hire the way they were when the economy emerged from the pandemic, which led many firms to offer sharp pay increases to attract and keep workers. Rapid pay increases and solid income growth helped consumers weather the higher prices that resulted from the pandemic’s supply chain disruptions, and fueled spikes in demand that led many companies to raise prices further. “That’s where this really differs, is that we aren’t seeing anywhere near the strength of demand,” Alan Detmeister, an economist at UBS, said. In 2021 and 2022, income growth “was increasing really strongly. We aren’t seeing that now,” he added. Detmeister thinks the better comparison will likely be to 1990-91, when higher oil and gas prices stemming from Iraq’s invasion of Kuwait contributed to a recession, but didn’t lead to a jump in inflation, in part because of weaker consumer spending. The gas price spike’s impact on inflation is, in some ways, similar to President Donald The President’s tariffs, in that their effect will depend largely on the size and duration of the increase. Higher gas prices are tricky for the Fed because they can also slow growth by weighing on consumer spending, potentially causing layoffs. The Fed would typically cut its rate to encourage more spending if unemployment rises, while it raises rates to combat inflation. —Christopher Rugaber, AP economics writer View the full article

-

If you’re thinking about implementing project portfolio management tools, it can help to know what benefits you can expect. These include better resource allocation, faster decision-making, and improved ability to achieve strategic goals. More here. The post 18 Top Benefits of Project Portfolio Management Tools appeared first on The Digital Project Manager. View the full article

-

It happens to the best of us: You write up a comment on an Instagram post, hit send, and, whoops, realize you made a glaring typo. What do you do? Do you delete the comment, retype it, and submit again, doubling the notifications the poster will receive? Leave it, and hope others will overlook your foolish use of "it's" instead of "its"? Neither option is great, but they're the only two choices you have on Instagram, right? No longer: On Thursday, Instagram announced some exciting news for frequent commenters: Going forward, you'll be able to edit your Instagram comments. Whether you regret one part of your comment, or you only need to fix a mistake, this new feature lets you make adjustments without having to delete your comment entirely, catching up to other platforms that let you make similar edits. Comment editing, with limitsComment editing can be a slippery slope. If someone makes a controversial comment but edits it after other people comment en masse, it only creates confusion for users stumbling upon the chaos after the fact. Perhaps that's why Instagram is adding some limitations here. First, you only have 15 minutes after posting a comment to edit it. This is how message editing works on platforms like Apple's Messages app—you only have a finite amount of time to adjust your comments before they're set in stone. Once that 15 minute window is up, your comment is locked to your last edit. What's more, when you do edit your comments, Instagram places an "Edited" label next to it—letting everyone know you changed the comment in some way. Instagram doesn't make it possible to view the edit history, so no one will be able to see what you said before that last edit—unless, of course, someone took a screenshot of one of your previous comment versions. Also, you can only edit text comments, not images. If you post a comment with an image, you'll need to delete the entire thing to remove that image. How to edit comments on InstagramOnce you make a comment on an Instagram post, you should now see a new "Edit" button appear next to "Replay" and "Share on Threads." Tap it, and your comment will appear in the text field again. Make your adjustments, then tap the "Send" button again. Remember: You only have 15 minutes from when you first made that comment to make your changes. View the full article

-

Advisory Revenue Strategies: Navigating the New FICA Tip Credit Landscape with Jody Padar Wed., Apr 22, 2026, 1-2 PM ET Register here | Learn more Go PRO for members-only access to more Jody Padar. View the full article

-

Advisory Revenue Strategies: Navigating the New FICA Tip Credit Landscape with Jody Padar Wed., Apr 22, 2026, 1-2 PM ET Register here | Learn more Go PRO for members-only access to more Jody Padar. View the full article

-

Demonstrate your specialized expertise and become their first choice. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-

Demonstrate your specialized expertise and become their first choice. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-

Americans are skipping restaurant dinners, delaying car purchases, and scouring for grocery deals. Amid tariff anxiety and broader stress over affordability, consumer confidence has dropped to levels not seen in over a decade, according to The Conference Board, a business think tank. At this point, it’s wealthier consumers who are powering the bulk of spending in the U.S. economy. So what explains the success of Erewhon’s US$22 smoothie? The Los Angeles grocery chain selling these fancy concoctions is doing so well, it opened three new stores in 2025—its biggest expansion since 2011. The chain reportedly generates $1,800 to $2,500 in sales per square foot, up to five times what a typical U.S. supermarket earns. These aren’t ordinary blended drinks; they include ingredients such as high-grade sea moss gel, adaptogenic mushrooms and collagen peptides. Often they come with a celebrity’s name attached. It’s all part of the broader boom in the U.S. specialty food market, which has surpassed $219 billion—up nearly 150% in a decade, according to the Specialty Food Association. That far outpaces the roughly 47% growth seen in overall U.S. grocery sales over the same period. Independent retail data from the market research firm Circana also confirms this growth: Even as inflation-weary consumers have traded down to store brands in many categories, premium and specialty products held up and even grew their dollar share of the market through 2025. On TikTok, creators who once filmed designer-bag hauls now post $12 tinned fish boards. Craft chocolate bars that cost $8–$12 are being marketed as, without irony, “self-care.” So if consumers are this anxious, why are they still splurging? In fact, these aren’t contradictions—they’re two expressions of the same psychological reaction. When people feel life is out of control, they reach for something small, expensive, and signaling virtue. This is the real reason premium food is booming while some traditional luxury brands struggle, say consumer psychologists. We are professors of consumer behavior and marketing who study how people make purchasing decisions amid economic uncertainty, and ask what explains the gap between how consumers feel and how they actually spend. Our work points to a consistent finding: When people feel they’ve lost control over the big things, they seek it in the small ones. A quick detour through the makeup drawer Economists have seen this before. In 2001, Estée Lauder Chairman Leonard Lauder coined the term the “lipstick index” after he saw that lipstick sales rose 11% following the Sept. 11 attacks. When big luxuries feel out of reach, consumers find a small substitute. A $60 lipstick is extravagant for a cosmetic, but next to the Hermès handbag it psychologically replaces, it feels like a bargain. Then, as now, people seek agency wherever they can find it. Consumer psychologists call this “compensatory consumption”: buying things to feel in control when life feels out of control. While even beauty sales are softening, that impulse hasn’t disappeared. It has just found better hosts—such as food. In many ways, food is an ideal product for this compensation. It’s experiential—something you taste, smell and savor. It’s also emotional—carrying associations with comfort, care and home. And it’s visible, because if you’re on social media, what you eat is now as public as what you wear. Premium food isn’t just eaten—it’s filmed, posted, and performed. Most importantly, it’s still relatively accessible. Twenty-two dollars may be an absurd price for a drink, but it’s cheap compared with a $400 wellness retreat. Indulgence with a side of virtue Here is what separates this moment from Lauder’s lipstick index. That example was purely about pleasure, as consumers sought indulgence as consolation. Today’s premium food purchases carry an additional layer: They are coded as virtuous. An Erewhon smoothie isn’t just a treat. It’s organic, superfood-enriched, and wellness-aligned. By the same logic, a $20 bottle of single-estate olive oil isn’t just cooking fat; it’s a commitment to craft and health. Premium tinned fish isn’t convenience food; it’s sustainably sourced protein caught in the wild with packaging beautiful enough to display. This “virtue coding” does the most important psychological work in the sales transaction: It transforms indulgence into self-investment. You’re not splurging during a downturn; you’re doing something for your health. You’re not being frivolous; you’re supporting small producers. Research shows that people need reasons to justify pleasurable purchases, especially during financial anxiety—and premium food is powerful because the justification is built into the product. The organic label, the sustainability story, the wellness framing—they all dissolve guilt before it even kicks in. Consumed in the kitchen and again on the feed There’s a reason this trend is accelerating now. Many premium food purchases are consumed twice—once physically and once digitally. The Erewhon smoothie purchase isn’t really about the drink; it can be as much about the content as the drink. The tinned fish board is plated for Instagram before anyone takes a bite. Social media doesn’t just amplify the trend; it completes it. When you post a photo or video of the smoothie, you’re broadcasting that you value wellness, quality and intentionality. In a cultural moment when flaunting a designer bag feels tone-deaf, food provides perfect cover. It’s the safest flex there is. It’s no surprise that one YouTube video of an Erewhon haul by food creator @KarissaEats has drawn over 14 million views. All of this raises a fair question: Does the growing focus on the “K-shaped economy” explain this boom? As many economists see it, low- and middle-income shoppers are increasingly pulling back, as they face an affordability squeeze from health care to housing and education. But wealthier consumers are picking up the slack and then some, splurging on luxury and powering gross domestic product growth. In this scenario, premium food thrives because it’s still affordable for the people who are doing fine, even as everyone else cuts back. That’s partly true. But this explanation doesn’t account for another shift—why affluent consumers are foregoing splurges on items like designer handbags in favor of premium groceries. This is why the virtue framing matters so much. If the question was purely about having money to spend, traditional luxury would be booming as well. It isn’t. A case in point is LVMH, the conglomerate behind Louis Vuitton and Dior, which saw its fashion division’s profits decline 13% across all of 2025. Even consumers who are flush with disposable income need psychological permission to spend during anxious times. The premium food phenomenon is about why food has become the thing they choose—not about who can afford to splurge. And when a smoothie becomes a status symbol, it tells us something about economic security more broadly. Food prices have climbed nearly 30% since 2019, outpacing 23% for overall consumer prices, according to the Bureau of Labor Statistics. For a family stretching a tight grocery budget, $22 isn’t a smoothie. It’s dinner. The need for control, the desire for identity, the comfort of virtue permission—these are universal. A single mother working two jobs feels the same craving for agency as the influencer filming her grocery haul. It’s just that the purchases that satisfy those needs are increasingly constrained by price. The justification only works if you can afford your indulgence. What’s really in the cart The next time you’re in a grocery store and you reach for something a little more expensive than what you might need, you should pause—not to put it back, but to think about what you’re actually reaching for. Chances are it isn’t really about the product. It’s about the feeling of choosing something when the world feels out of hand. A $22 smoothie is never just a smoothie. It’s what people seek out when they need permission to feel OK. Yuanyuan (Gina) Cui is an assistant professor of marketing at Coastal Carolina University. Patrick van Esch is an associate professor of marketing at Coastal Carolina University. This article is republished from The Conversation under a Creative Commons license. Read the original article. View the full article

-