All Activity

- Past hour

-

A useful rule of thumb is that when a problem persists for decades despite serious effort, the failure is usually not one of effort or intelligence, but of framing. Climate change sits squarely in this category. We have poured talent, capital, policy, and good intentions into solving it, and yet the core dynamics continue to worsen. This suggests that something foundational is off in how we are thinking about the problem. One of the clearest illustrations of that deeper issue sits far from financial centers and climate summits, in the Arctic. About 50 years ago, Denmark made a decision that looks increasingly unusual by modern economic standards. It removed around 40% of Greenland—nearly 1 million square kilometers—from economic use. This was not a marginal conservation effort. It was the largest protected land designation on earth, an area over 100 times the size of Yellowstone. The land remains a functioning Arctic ecosystem, supporting polar bears, seals, walruses, musk oxen, Arctic foxes, wolves, and vast seabird populations. From a narrow economic lens, this choice appears irrational. Greenland contains valuable mineral resources. It also holds growing geopolitical importance as Arctic shipping routes open and strategic competition intensifies. By standard economic logic, leaving that much land “unused” looks like a forfeited opportunity. But Denmark’s decision reveals something important: Not everything that can be monetized must be. And, more important, not everything should be exposed to economic optimization. In today’s dominant economic framework, nature is treated primarily as an input. Land, minerals, forests, water, and even stable climate conditions are framed as raw materials for industrial activity. Protection, when it occurs, is often justified as a temporary or charitable act—acceptable only until a more profitable use emerges. Under this logic, conservation survives only as long as it loses less money than extraction. This is not an accident. It is a direct consequence of how we have structured the economy. The limits of capital Capitalism functions through optimization. It compares assets, allocates resources, and directs effort toward whatever produces the highest returns under the current rules. But to be optimized, something must first be defined as capital. Once that conceptual conversion happens, it becomes tradable, comparable, and expendable. Over the past century, we have steadily expanded what qualifies as capital. People became “human capital.” Ecosystems became “natural capital.” Social systems became “social capital.” Each step made it easier for the economic algorithm to operate, but it also stripped away dimensions that are essential to long-term stability. The problem is not that capitalism is malicious. The problem is that it is literal. It has no intrinsic sense of restraint, sufficiency, or long-term system health. It follows the math it is given. When nature is framed as capital, the system will exploit it until the marginal costs exceed the marginal returns. By the time that happens at planetary scale, the damage is already locked in. When the human population was smaller and the gift of the historically accumulated health/wealth of nature was much greater, it was an economically workable assumption to pretend that nature was effectively infinite. It is no longer plausible to maintain that assumption. Every habitable corner of the planet has been explored and settled. According to global wildlife assessments, monitored populations have declined by roughly 70% in just the past half-century. Today, almost all mammalian biomass on planet Earth is livestock and humans. The living systems that support clean air, stable water cycles, fertile soil, and biodiversity are being eroded faster than they can regenerate. Diminishing returns In economic terms, we have reached diminishing returns. The gains from continued exploitation are now smaller than the costs imposted by destabilized ecosystems. Floods, fires, heat waves, water scarcity, crop failures, and forced migration are not externalities anymore. They are direct expenses, borne by all. This exposes a core misconception: that the economy and ecology are separate domains that must be balanced against each other. In physical reality, the economy is a subset of ecology. If you look around, you’ll see that everything in the economy is either mined or grown, which means it came directly from nature. Even digital businesses use real metal, stone, water, and vast amounts of electricity to construct and run data centers, a reality that is becoming apparent to more and more people who live near data centers. In other words, even our virtual economy is physical, and comes directly from mined and grown resources. Once this is acknowledged, the Greenland decision looks less like charity and more like sound systems thinking. Denmark implicitly recognized that some portions of the biosphere function as critical infrastructure. Arctic ecosystems regulate climate patterns, ocean circulation, and planetary albedo. They are not interchangeable with financial assets. Exposing them to short-term economic optimization would undermine their long-term value—not just to Greenland, but to the global system. This is where modern economic thinking struggles. When everything is treated as capital, the only protection mechanism available is pricing. Carbon markets, biodiversity credits, and ecosystem service valuations all attempt to make nature “visible” to the market. While well-intentioned, this approach contains a structural flaw: If a higher-value use emerges, the same pricing logic can justify destruction. We have seen this dynamic repeatedly. Forests preserved for carbon value are later logged when timber prices rise. Wetlands protected for ecosystem services are drained when development yields higher returns. The algorithm is doing exactly what it was designed to do. The alternative is not to abandon markets, but to place boundaries around them. The effectiveness of boundaries We already do this in other domains. The global ban on the sale of human organs is a clear example. We collectively decided that allowing organs to be traded as capital would produce outcomes that were morally unacceptable and socially destabilizing—even if the market demand were real. History offers darker reminders of what happens when human beings themselves are fully converted into capital. The same logic applies to essential ecological systems. Some functions are so foundational to life and long-term prosperity that they must be categorically excluded from economic trade-offs. Once those boundaries are set, economic optimization can resume within them, and often performs better as a result. Land that is managed in alignment with ecological regeneration tends to retain productivity longer. Agricultural systems that invest in soil health reduce dependence on external inputs. Landscapes that preserve biodiversity lower long-term operational risk. Take, for example, palm oil plantations in Southeast Asia. They start by clear-cutting a landscape, trucking out all the timber, and planting vast monocultures of oil palms. Within 25 years, these monocrop plantations end their commercial life, leaving the communities and land in a degraded state. To maximize the long-term economic value of the land, they could instead set aside 20% of it to maintain proximity to biodiversity, which substantially reduces the recovery time from deforestation. Corporate yield per managed acre would be slightly less for the short term, but would be economically superior even in the medium term. When you use up a landscape, you need to incur the additional cost of procuring new land, training new people, setting up new supply-chain lines. These are costs that would be avoided or reduced with more thoughtful land planning and set-asides. A nation that wanted to optimize its long-term prosperity would get interested in the exact set-aside percentage that gives the optimal blended return, factoring in long-term economic value and natural resource value. Greenland’s smart play Greenland’s protected lands are not idle; they are performing climate regulation services that would be prohibitively expensive, if not impossible, to replace technologically. The path forward begins with a simple shift: Stop assuming everything should be capital. Decide, consciously and explicitly, which systems constitute our planetary life support infrastructure. Protect them by design, not by pricing gymnastics. Then allow markets to operate vigorously everywhere else, informed by the true physical constraints of the world they depend on. The economy is paying the price for ignoring this distinction. The longer we delay making it explicit, the higher that price will climb. —By Tom Chi, Founding Partner at One Ventures This article originally appeared on Fast Company’s sister website, Inc.com. Inc. is the voice of the American entrepreneur. We inspire, inform, and document the most fascinating people in business: the risk-takers, the innovators, and the ultra-driven go-getters that represent the most dynamic force in the American economy. View the full article

-

Unlock the secrets of AI visibility. This 90-day playbook can help enhance your brand’s presence in AI searches. The post The 90-Day AI Search Sprint: How To Rebuild Your Marketing For 2026 Visibility appeared first on Search Engine Journal. View the full article

-

The industry is pushing for building entry loss inclusion into AFC calculations and higher spectral power density for low power indoor 6 GHz Wi-Fi. The post Regulation: Two FCC 6 GHz rule changes could dramatically boost 6 GHz Wi-Fi performance indoors appeared first on Wi-Fi NOW Global. View the full article

- Today

-

Damage to Habshan facility highlights lasting impact of Middle East conflict on Gulf energy exportsView the full article

-

Prime minister’s future on the line as he prepares for crucial cabinet meeting amid party revoltView the full article

-

Fears growing that leadership contest could unleash chaos on already jittery bond marketsView the full article

-

From sugary cereals to Pop-Tarts and other pastries, many of the things Americans are used to eating first thing in the morning aren’t optimal for health. But according to new research, one traditional breakfast food could help protect your brain, and no, it’s not coffee. It’s eggs. The new report, recently published in the Journal of Nutrition, comes from researchers at Loma Linda University who followed 39,498 participants for 15-plus years. Their study found that regular egg consumption may be linked to a lower risk of developing Alzheimer’s disease. The benefit appears to be significant. But in order to achieve the maximum reward, you need to make eggs a staple in your diet, not just a Saturday morning meal. The study found that those who ate at least one egg per day at least five days per week reduced their chances of developing Alzheimer’s by up to 27%. Consuming at least one egg two to four times a week saw Alzheimer’s risk go down 20%. And even occasional egg consumption—such as one to three times per month—made an impact, as it was linked to a 17% reduction in Alzheimer’s risk. “Compared to never eating eggs, eating at least five eggs per week can decrease risk of Alzheimer’s,” Dr. Joan Sabaté, a professor at Loma Linda University School of Public Health and the study’s principal investigator, said per Science Daily. Sabaté explained that eggs are essential for brain health for a number of reasons. First, they contain choline, which is important because it allows the body to produce acetylcholine and phosphatidylcholine, compounds that contribute to memory and communication between brain cells. Eggs also contain lutein and zeaxanthin, which have shown links to cognitive performance and lower levels of oxidative stress. Likewise, omega-3 fatty acids, mostly found in egg yolks, are key to maintaining neurotransmitter receptor function. Vitamin B12, also found in egg yolks, “plays a multifaceted role in brain function,” according to the published report. More than 7 million Americans are living with Alzheimer’s, and the costs are massive. According to the National Institute on Aging, Alzheimer’s disease and related dementias cost the U.S. around $781 billion in 2025. “With the rapid aging of the United States population and projected increases in healthcare costs, understanding the potential role of egg consumption in reducing Alzheimer’s risk carries important implications, especially for Medicare, the largest source of healthcare spending in the United States,” the report in the Journal of Nutrition said. View the full article

-

Simone Stolzoff has a gift for asking questions that slice the soul. In his first book, The Good Enough Job, he asks how work came to be so central to our identities, and what we can do to rebalance our lives. He’s a journalist whose writing on the intersection of work, identity, and relationships has appeared in The New York Times, The Atlantic, Wired, and National Geographic. Now he’s back with a second book: How to Not Know: The Value of Uncertainty in a World that Demands Answers. This time around, he unpacks why uncertainty generates so much anxiety, and what we can do about it. In a world where climate change is reshaping the actual landscape, politicians are throwing out new policies at the roll of a dice and then walking them back again, and AI is changing reality as we know it, Stolzoff offers answers. Not on what’s going to happen—but how to cope better. Stolzoff sat down with Fast Company to discuss what he learned while writing his book. The interview has been edited for length and clarity. Something that struck me about your book: Not knowing if something will happen is more painful for most people than a bad experience actually happening. Can you explain why uncertainty feels so painful, and walk us through the research? Our natural tendency is to see it as a threat: If you think about an ancestor of ours in the jungle hearing rustling in the bushes, not knowing the source of that noise could potentially be lethal. Our brains are wired to feel safe and secure when we are certain, and to feel anxious or worried when we are uncertain. One of our brain’s natural tendencies is to try and get out of uncertainty as quickly as possible. The problem is often this means opting for the safe bet, which isn’t always the right bet. [Studies have found that] for women facing a potential breast cancer diagnosis, the period of time between when you get a biopsy to when you get the results tends to be the hardest part of the entire journey—more stressful than chemo or surgery. Another really interesting study found that research participants who were given a 50% chance of receiving a painful electric shock felt far more stressed than those who were given a 100% chance of receiving a painful electric shock. We would rather deal with a certain bad thing than have to reckon with the ambiguity of not knowing our fate. What problems does this intolerance create? It leads to anxiety. It leads to worse mental health. It leads to people worrying about things they can’t control. At a broader scale, I think one of the main skills of life is to be able to get to a place where you don’t know what is to come, and to persist nonetheless. I wonder if our need for answers makes us more vulnerable to misinformation. It does, and research has shown this. If you’re intolerant of uncertainty, the attractiveness of false certainty is all that much more alluring. If someone offers an easy explanation for how you should cure COVID, for example, it’s really easy to latch on to an easy answer. That’s comforting until you realize that it’s false. And in the first chapter of the book, I talk about a woman who falls into a cultlike organization where someone promises if you just do X, Y, and Z, then you’ll get this desired outcome. And it’s attractive. Who wouldn’t want a clear set of instructions or protocol of how to succeed or go to heaven? But as she told me, it was easy until it wasn’t. What factors in our society lead us to be worse at handling uncertainty? There’s a study that I love from a researcher named Nicholas Carlton at the University of Regina. He found that the rise of the internet, and specifically of mobile phones, correlates with the rise of intolerance of uncertainty. I think a few things are going on. One is that we live in this information age. You might expect access to limitless information helps resolve some of the uncertainty we feel. But in fact, often more information just fuels our anxiety. This access to information robs us of practicing sitting with what we don’t know. Maybe 10 years ago, I might have been okay not knowing the name of an actor, for example. Now I feel this almost involuntary need to reach into my pocket and figure it out right now. The problem is that not all questions are Google-able or ChatGPT-able. Our tolerance for uncertainty is particularly low right now. And our ability to tolerate uncertainty is what makes so many people feel anxious and unmoored. What should we do if we’re dealing with uncertainty—for example, waiting for the results of a test, or for news that may be good or bad? The first place to start is [to ask yourself if] there’s anything you can do to influence the outcome. Say you are a high school senior and you are really stressed out about whether or not you’ll get into college. If you’re in the period of time before you submit the applications, there are things that you can do to help influence the outcome: You can try and write a great application, you can get good grades, you can get letters of recommendation, etc. Those are all sort of in the sphere of your control. Then if you’ve done everything that you can do to influence the outcome, or if you can’t influence the outcome, the next level down is: Are there ways you can prepare for different contingencies, different possible outcomes? Often, especially in a business context, we get stuck on one particular outcome. But it’s more adaptive for us to be able to plan for multiple potential scenarios so that we’re better equipped to deal with what might come our way. Once you’ve done what you can to prepare for multiple different scenarios, it comes down to acceptance. You can do things like look for silver linings. You can do this practice called bracing for the worst, which is thinking about the worst thing that could happen and then trying to figure out how you’d be able to bounce back from that. But really it comes down to regulating your nervous system—being able to be okay with the not knowing. That may mean distracting yourself. There’s a wonderful study where they had people waiting for the results of a test play three different levels of Tetris: One was really easy, one was really hard, and one was just right. The researchers found that the people playing the really easy and the really hard levels were really stressed out by the waiting game. However, the people who found something that sufficiently challenged them were able to find a flow state and the waiting passed more easily. There’s also been research that shows breath work and yoga and meditation can help in dealing with the waiting period. What about a situation where you don’t know when the uncertainty will be resolved? There’s an example that I give in the last chapter of the book, which is I have this friend named Emily, who’s a therapist. She works with entrepreneurs and people dealing with change and different facets of their lives. But before she became a therapist, her mom was given a terminal diagnosis. Emily spent weeks sitting by her mom’s side and worrying about the worst-case scenario. A family friend came by and asked, “How are you doing?” And she said, “I’m not doing great. I’m riding this roller coaster of fear and respiratory grief, and I’m really not sure what I’ll do if my mom dies.” Her friend told her, “The version of you that will be born into existence if and when that tragic event occurs will have more context, more information, and be better equipped to deal with that tragedy than you are today. You have to trust in your future self to handle your future problems.” View the full article

-

Unlock the secrets of AI visibility to adapt your website for future search trends and improve technical SEO practices. The post The Tech SEO Audit for the AI Search Era: How to Maximize Your AI Visibility appeared first on Search Engine Journal. View the full article

-

You know the feeling we are talking about. Your friend calls to ask for your help moving on a Saturday when you were planning on doing nothing. Or your sister-in-law asks you to invest in her business, and you are afraid there is no way it will succeed. Even when the person asking for the favor isn’t someone central to your life, it is still painful to say no. Most of us don’t even like saying no to telemarketers. That’s why there are so many jobs in sales. Often, we end up making bad decisions to avoid the short-term discomfort of turning people down. Look, we agree—saying no is hard. The good news is that a little preparation and practice will make it easier. Even if you are one of those people that dreads it. We will look at different kinds of ‘no’s’ that are appropriate in different situations. Sometimes, there is a clear answer, and you want the other person to accept your offer without complaint. Your kids, for example, should know there is no argument about bedtime. Your boss needs to accept that you can’t work late anymore after coming back from maternity leave. The sooner they accept the reality, the happier everyone will be. Other times, you might be willing to be persuaded. You like the job offer, but the salary could be better. In that case, you might want to say no in a way that encourages them to try again or try harder. You Can Say No Nicely While being able to give a flat, unequivocable no is an important skill to develop, it’s not the goal. Usually, we want to be more polite, even if we find another’s proposal unattractive. Why? Because we never know when we will want to revisit that now-closed door. Preserving the relationship can allow a chance to revisit in the future, and we always like to maintain future opportunities if possible. The standard way to be respectful is to help someone learn why you aren’t interested. Here’s the problem with that: When you tell the reason you are turning them down, you give them information that they can use to make another appeal or proposal. Let’s say you are a young unattached woman. A guy asks you to go to dinner at the local barbeque joint, but you aren’t interested in him. If you tell him, “No thanks, I am a vegetarian,” there’s nothing stopping him from saying, “OK, so why don’t we go to Tofu Town?” Now it’s harder to say no, because you’ve given an inaccurate reason for your refusal. So instead of giving your reasoning, let’s discuss other ways that you can give a nice no. For those of you who have discomfort with no, this may be a balm for that, because it allows you to exit gracefully (but still unequivocally). Be Polite Thank them for asking. And you can apologize that you don’t have a different answer. “That is so kind of you. I appreciate your asking. I’m sorry but I can’t say yes.” The strength of your answer doesn’t require you to be rude. What makes it emphatic is that you give them a clear, inarguable response. “It’s Not You, It’s Me.” Your reasons don’t have to imply a negative judgment. Don’t let your reason have anything to do with them. It is only about you and your preferences. If someone offers you a job and you aren’t interested, you might say: “I’m dedicated to my current team.” “I’m on a good trajectory and am not interested in moving.” And our favorite: I’m so grateful, but it’s not the right time for a move.” None of these present a good opportunity for them to try again. When you consider possible responses to shut down further efforts to persuade you to say yes to a request, try to imagine a workaround. Use obstacles that can’t be solved or resolved rather than something like, “Sorry, I’m not interested in a lateral move,” because they could suggest an elevated position. Keep Your Reasons Vague The more information you give the other person about a problem, the easier it is for them to think of a solution. If you are not looking for a solution, provide as little information as possible. Keep your response short and to the point. If they ask for more information, remember, you are under no obligation to share it. “I’m so grateful but it’s not the right time for a move.” “How come?” “There are some exciting internal opportunities, but I’m not at liberty to discuss them.” If they keep pressing you, push back more firmly. “I’m afraid you will have to accept my decision as final.” Now, sometimes people do sincerely want feedback on why their offer wasn’t good enough. Remember that you never have to, but if you want to provide that feedback, feel free to do so—just be cautious about offering them an opening to try to draw you back into a negotiation. In addition, be kind when offering the feedback. Make Suggestions for Their Alternative A colleague of ours works with a speaker’s bureau. She gives talks at big speaking events and conventions. She is extremely well paid and charges a standard fee. Occasionally, a potential client will try to bargain her fee down. She tells them, “The speaker’s bureau I work with charges all my clients the same rate so I can treat everyone fairly. I know I may not be the right choice for everyone’s budget. I can suggest some of my younger colleagues who do an excellent job and are more affordable.” There are several reasons why this works. First, it’s clear that you aren’t engaging in a bargaining ploy. Someone who is genuinely interested in a speaking engagement doesn’t suggest the competition. So, the customer knows she isn’t bluffing. Second, while rejecting the offer, she is trying to fill the client’s need. And it gives her the chance to potentially push some work to deserving younger colleagues. Excerpted from NEVER SETTLE. Copyright © 2026, John Richardson and Attia Qureshi. Reproduced by permission of Simon Acumen, an imprint of Simon & Schuster. All rights reserved. View the full article

-

Currency weakens after US Treasury secretary meets finance minister Satsuki KatayamaView the full article

-

It’s five answers to five questions. Here we go… 1. I was fired for charging customers’ cash purchases to my credit card Started my part-time summer job (I am retired) a few weeks ago, working at small convenience/snack/candy store near a local free tourist attraction that opened up for the season. Got fired yesterday. This year, the store went to a “no cash” payment system. Small sign on the door, another by the register. Problem is, not all people carry other forms of payment besides cash, mostly older folks, plus who wants to use their credit card for a 50 cent piece of candy? To help these customers out, especially ones who don’t have another form of payment available, I accepted their cash, then ran the transaction on my credit card. I asked if this was okay with them before hand and printed off a receipt that I kept for my records to keep everything on the “up and up.” The owners noticed the number of receipts with my name on it and questioned me. I explained what I was doing and why and they fired me on the spot for “violating company policy.” I asked them to show me the policy and they could not. I asked them what specifically I was doing wrong, they could not give me an answer. I understand “employment at will” so they can let me go for any reason, but I may file for unemployment because they didn’t have a “valid” reason for firing me and that is why I am writing. Was what I did wrong? Yeah, it wasn’t wise. You were overriding the store’s payment policy; you basically created your own means for customers to pay, without first checking with your employer. I think they overreacted by firing you — they should have just told you to stop doing it — but you should have asked your manager first if it was okay to do it, especially before doing it multiple times. Most importantly, having a bunch of receipts with an employee’s name on them is likely to raise red flags from an auditor. Beyond that, though, a customer could come in when you’re not working and expect a different cashier to do the same thing you were doing, and then be upset or frustrated when they refuse. It also opens your employer to accusations that they’re accepting cash from some customers and not from others. 2. New boss keeps questioning how I’m doing things When I started this job about 10 months ago, my old manager made sure to give me positive even when I was new. Any negative feedback became a conversation instead of something accusatory, and she noted in my performance reviews that I was doing great but needed more confidence. My old manager made me feel heard and like I could talk to her about any troubles I was having at work. However, she left the company, and our team’s new manager isn’t as great. It’s only been a few weeks but I constantly feel questioned as to why I’m doing things the way I am. What’s worse is that I don’t notice her asking similar things to my teammates. I feel like I’m being singled out and I’m the youngest with the least amount of experience. I never get positive feedback from my new manager, and it’s taking a toll on my self-esteem because I can’t accurately judge if I’m good at the job or not. Do you have any advice for me? I really like the job and with my old manager, saw myself staying for years. Now I’m contemplating if I want to stick around more. It’s possible that you’re being singled out because you’re the least experienced, but it’s also possible that you’re being singled out because your new manager finds you the most approachable or thinks your explanations are the clearest or shortest or she likes your way of doing things. It’s also possible that she’s asking your coworkers and you just don’t see it. Or, yes, it’s possible that she’s doubting your expertise. But why not ask her? You could say, “Do you have concerns about the way I’m doing things like X or Y? You’ve asked me a lot about it, and I wasn’t sure if you’re just interested in the way we do this or if you’re concerned by anything about how I’m approaching the work.” 3. We give raises to salaried workers, but not hourly workers I work for a private college. They annually give cost-of-living raises to salaried employees, but hourly employees in the department I oversee and in comparable departments have stayed the same for the last eight years. I’ve spoken to my manager, who is a very nice human but doesn’t want to be seen as challenging and struggles with negotiations in any setting. I’m trying to prep him effectively to argue that if both merit and cost-of-living raises are the norm for salaried employees, then even if part-time roles are capped on a pay scale and even if merit raises are not an option, if the company recognizes the need for cost-of-living raises for salaried workers, this logic should be applied to anyone working for the organization. Would love some input. What on earth. If an employer recognizes cost-of-living raises are necessary to keep up with inflation, there’s no logical basis for excluding hourly workers from that (unless there’s some really odd and extenuating circumstance, like that somehow all the salaried workers just happened to be dramatically underpaid and none of the hourly workers are, which seems pretty unlikely). Are they just completely uninterested in retaining the hourly workers and unconcerned by the costs of finding and training replacements? In your boss’s shoes, I’d start by asking for the reasoning for excluding hourly workers from salary adjustments to keep up with inflation and go from there (next, presumably pointing out that hourly workers face the same cost-of-living increases as other employees, and that turnover from not retaining them will be disruptive). 4. How can people get my attention when I’m wearing headphones? I work in an open concept floor plan, with my desk facing (gloriously!) a window. To cope with the noise and to be able to focus, I wear noise-cancelling headphones that really block out everything. People often come up behind me and want to get my attention. I was wondering if there was any technology gimmick that I could use — something like a button they could press for a light to turn on at my desk, or something to push a notification. The sillier, the better! I am not shy about putting together something custom. Any ideas, or even keywords that I could search, would be amazing! Right now I am trying to use a mirror, which is probably the best low-tech option, but I’d love to know if there’s something more fun I could do. There are earbuds that allow you to hear human voices over music — but it sounds like you’re purposely trying to drown out human voices most of the time. There’s also tech that was initially developed for deaf users that will trigger a visual alert like flashing a desk lamp. The search term you want is “alerting devices.” 5. What are employers doing about high gas prices? I’m curious if your readers are hearing anything from their employers regarding the exorbitant gas and oil prices right now? I haven’t heard anything from my employer, but I’d love to know if (and how) other companies are communicating about this. What can (or should) we expect when transportation costs are this high? My sense is that the majority of employers aren’t doing this, but some companies are offering gas cards or cash stipends or temporarily increasing mileage reimbursement rates. Some are also increasing work-from-home options or temporarily suspending return-to-office mandates. Here are some articles about what specific companies are doing: 1, 2, 3, 4 The post I was fired for charging customers’ purchases to my credit card, new boss keeps questioning me, and more appeared first on Ask a Manager. View the full article

-

The move is a value play for the hamburger chain whose shares have slid 70% in the past 5 years View the full article

-

There is good reason to be dubious about the notion that automation will supplant all demand for human labour View the full article

-

Traders expect corn and soyabeans to soar as demand for alternative fuel sources risesView the full article

-

US Senate widely expected to confirm the 56-year-old financier to replace Jay Powell this weekView the full article

-

Power flows less from size or wealth than from the ability to convert imbalance into leverageView the full article

-

In-house MeshClaw tool enables employees to delegate jobs to AI agents and climb company’s AI leaderboardView the full article

-

‘Tariff man’ wants to recover from a wounding Supreme Court ruling. But Congress is restive and voters are unhappyView the full article

- Yesterday

-

UK prime minister prepares for crucial cabinet meeting as mood turns ‘pretty ugly’ in Labour PartyView the full article

-

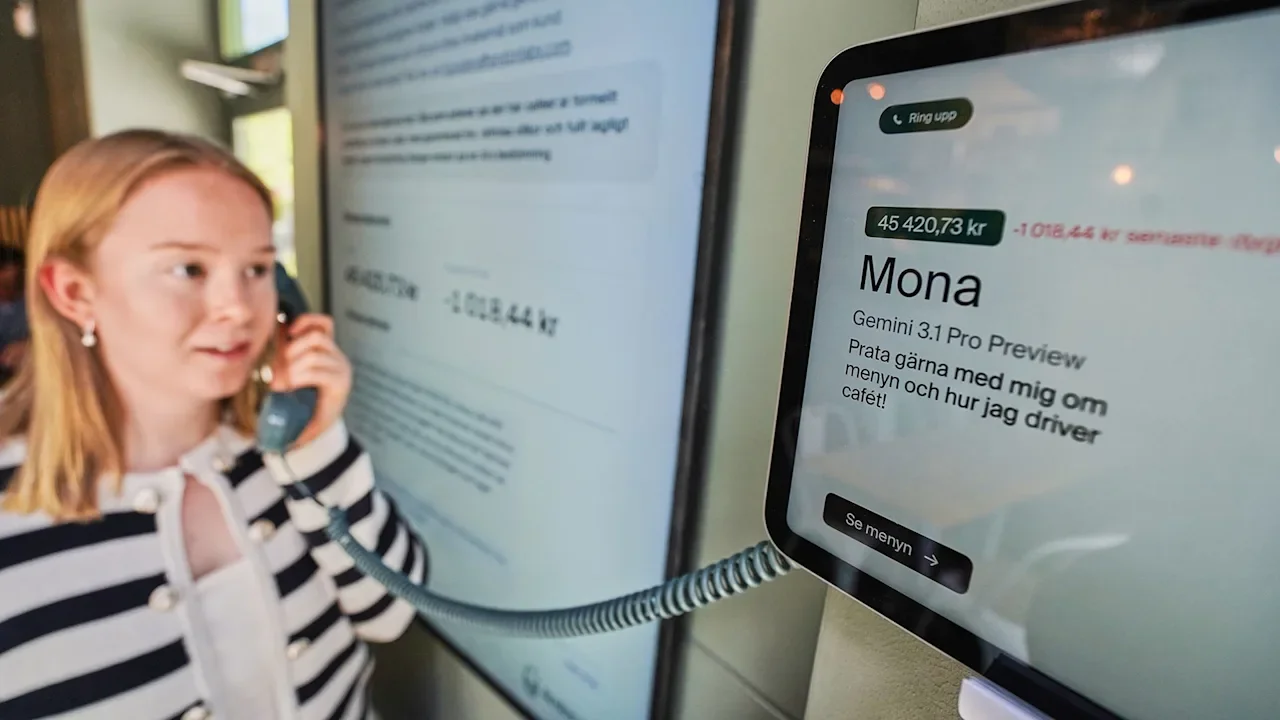

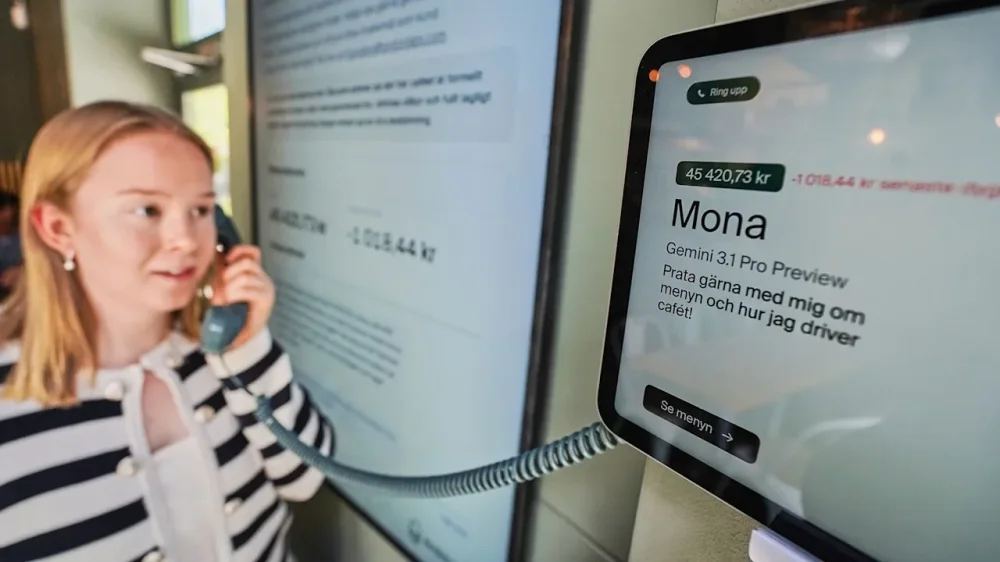

The coffee might be poured by a human hand, but behind the counter, something far less traditional is calling the shots at an experimental café in Stockholm. San Francisco-based startup Andon Labs has put an artificial intelligence agent nicknamed “Mona” in charge at the eponymous Andon Café in the Swedish capital. While human baristas still brew the coffee and serve the orders, the AI agent—powered by Google’s Gemini—oversees almost every other aspect of the business, from hiring staff to managing inventory. It is not clear how long the experiment will last, but the AI agent appears to be struggling to turn a profit in Stockholm’s competitive coffee trade. The café has made more than $5,700 in sales since it opened in mid-April, but less than $5,000 remains from its original budget of $21,000-plus. Much of the cash was spent on onetime setup costs, and the hope is that it eventually levels out and makes money. Many café patrons have found it amusing to visit a business that’s run by AI. Customers can pick up a telephone inside the café and ask the agent questions. “It’s nice to see what happens if you push the boundary,” customer Kajsa Norin said. “The drink was good.” Experts worry about AI’s role going forward Experts say ethical concerns abound, ranging from technology’s role in humankind’s future to conducting job interviews and judging employee performance. Emrah Karakaya, an associate professor of industrial economics at Stockholm’s KTH Royal Institute of Technology, likened the experiment to “opening Pandora’s box,” and said putting AI in charge can cause many problems. What might happen, he said, if a customer gets food poisoning? Who’s to blame? “If you don’t have the required organizational infrastructure around it, and if you overlook these mistakes, it can cause harm to people, to society, to the environment, to business,” Karakaya said. “The question is, do we care about this negative impact?” Founded in 2023, Andon Labs is an AI safety and research startup that says it focuses on “stress-testing” AI agents in the real world by giving them “real tools and real money.” It has worked with ChatGPT maker OpenAI, Claude’s Anthropic, Google DeepMind and Elon Musk’s xAI, and the startup says it is preparing for a future where “organizations are run autonomously by AI.” The Swedish café is billed as a “controlled experiment” to explore how AI might be deployed going forward. “AI will be a big part of society in the future, and therefore we want to make this experiment [to] see what ethical questions arise when we have AI that employs other people and runs a business,” said Hanna Petersson, a member of the technical staff at Andon Labs. The lab previously held pilots that put Anthropic’s Claude AI in charge of a vending machine business and a San Francisco gift store. The vending machine simulation revealed some worrying traits: The AI agent told customers it would issue refunds but never did, and it also intentionally lied to suppliers about competitor pricing to gain leverage. AI agent struggles with inventory orders Mona got to work after it was prompted with some basic instructions, Petersson said. The team told it to try to run the café profitably, be friendly and easygoing, and figure out operational details by itself but ask for new tools if needed. From there it set up contracts for electricity and internet, and secured permits for food handling and outdoor seating. The agent then advertised for staff on LinkedIn and Indeed, and set up commercial accounts with wholesalers for daily bread and bakery orders. It communicates with the baristas via Slack, often messaging them outside of working hours, which is a workplace no-no in Sweden. Other problems have arisen, particularly related to inventory. The AI agent has placed orders for 6,000 napkins, four first-aid kits, and 3,000 rubber gloves for the tiny café—plus canned tomatoes that aren’t used in any dish the café serves. And then there’s the bread. Sometimes the agent orders far too much, while other days it misses bakeries’ daily deadlines, forcing the baristas to strike sandwiches from the menu. Petersson said the ordering issues are likely due to the AI assistant’s “limited context window,” noting, “When old memory of ordering stuff is out of the context window, she completely forgets what she has ordered in the past.” Barista Kajetan Grzelczak said he isn’t worried about being replaced by AI just yet. “All the workers are pretty much safe,” he said. “The ones who should be worried about their employment are the middle bosses, the people in management.” —By James Brooks, Associated Press View the full article

-

It has become clear that women—and working mothers, in particular—are up against all kinds of challenges that threaten their foothold in the labor force. But one trend that may be less evident is that men are also dropping out of the workforce, albeit for different reasons. The jobs report last week offered a more sunny outlook than expected, with an uptick of 115,000 jobs in April; the unemployment rate also held steady at 4.3%. The data also, however, points to a more nuanced story about a broader shift in the labor force. Last month, the number of men who were working or actively looking for a job fell to the lowest figure seen in decades, with the exception of an anomalous dip during the early months of the pandemic. That means a third of men have dropped out of the workforce as of April. There are a few reasons for this decline, which has slowly emerged in the last few years: Much of the recent job growth has happened in industries that are dominated by women, like healthcare and education, while sectors like manufacturing that were overwhelmingly staffed by men have lost jobs. A recent report from Indeed’s Hiring Lab found that between February 2025 and February 2026, the share of jobs held by women climbed by nearly 300,000; meanwhile, the share of jobs held by men decreased by 142,000. More broadly, however, the gender gap in employment has been narrowing for decades, and women had actually already outpaced men on non-farm payrolls back in 2020. While job losses during the pandemic—and systemic issues that have kept mothers out of the workforce—set them back, women eventually overtook men in the workforce earlier this year. The losses among working men are not solely driven by people retiring or aging out of the workforce. Younger men, too, are stepping away from work for a variety of reasons, according to an analysis by The Washington Post. Some of them are going back to school or taking on caregiving duties, but a significant share are dropping out of the workforce due to illness or disabilities. The Post analysis found that men who had exited the workforce were more likely to live at home or have never been married, and there has also been an increase in the number of men who lack college degrees and no longer work. (On the whole, women are now more likely to hold college degrees relative to men.) Despite the job growth in certain sectors, this shift in men’s labor force participation is not fueled by an influx of women into the workforce. In fact, even as women see those gains in employment, their standing in the workforce is still precarious at best: About 212,000 women left the workforce in the first half of 2025, with a marked impact on working mothers. It’s telling that part of the reason men have not benefited as much from job growth in certain sectors is because there remains a stigma associated with working in industries that typically attract more women—not to mention lower wages. View the full article

-

Sales of previously occupied U.S. homes were essentially flat in April, another lackluster showing for the housing market during what’s traditionally its busiest time of the year. Existing home sales edged up 0.2% last month from March to a seasonally adjusted annual rate of 4.02 million units, the National Association of Realtors said Monday. Sales were unchanged compared to April last year. The latest sales figure fell short of the roughly 4.12 million pace economists were expecting, according to FactSet. Sales have been hovering close to a 4-million annual pace now going back to 2023, far short of the historic norm that is closer to 5.2-million. And home prices continued to rise nationally last month, albeit at a slower rate. The U.S. median sales price increased 0.9% in April from a year earlier to $417,700, an all-time high for any April on data going back to 1999, NAR said. Home prices have risen on an annual basis for 34 months in a row. The U.S. housing market has been in a slump since 2022, when mortgage rates began to climb from pandemic-era lows. Sales of previously occupied U.S. homes were essentially flat last year, stuck at a 30-year low. They have remained sluggish so far this year, declining from a year earlier through the first three months of this year. “This spring homebuying season, so far all the way through April, we can say we are not predicting any increase compared to one year ago,” said Lawrence Yun, NAR’s chief economist. While average incomes are now rising at a faster pace than U.S. home prices, affordability remains a major hurdle for aspiring homeowners. Years of soaring home prices, especially in the early part of this decade when rock-bottom mortgage rates fueled a buying frenzy, have left many would-be homebuyers frozen out of the market. And a chronic shortage of homes for sale nationally, due partly to years of below-average new home construction, has helped prop up home prices even in a multiyear sales slump. Homes purchased last month likely went under contract in February and March, when the average rate on a 30-year mortgage ranged from 5.98% — its lowest level in three and a half years — to 6.38%, according to mortgage buyer Freddie Mac. The average rate was at 6.37% last week. While the average rate has remained below where it was a year ago, it has been fluctuating since the war with Iran began, as surging energy prices fuel anxiety about higher inflation. Those who can afford to buy are benefiting from more properties on the market, although home inventory levels remain well below historical norms. There were 1.47 million unsold homes at the end of April, up 5.8% from March and up 1.4% from April last year, NAR said. That’s the most homes on the market for the month of April going back to 2019, when the month-end inventory stood at 1.83 million homes. That’s still short of the roughly 2 million homes for sale that was typical before the COVID-19 pandemic. April’s month-end inventory translates to a 4.4-month supply at the current sales pace. Traditionally, a 5- to 6-month supply is considered a balanced market between buyers and sellers. “We really need to see 30% growth in inventory, but we’re not really seeing that,” Yun said. One factor helping boost the supply of homes for sale is many properties are sitting on the market longer. Properties typically remained on the market for 32 days last month before selling, down from 41 days in March, but up from 29 days in April last year, NAR said. As homes take longer to sell, asking prices have started falling in many metro areas, especially in the South and Midwest. The national median home listing price was down in April from a year earlier, according to Realtor.com. —Alex Veiga, AP business writer View the full article

-

As a sole proprietor, you need to understand your tax obligations. When your net earnings exceed $400, you’ll file Schedule C with your Form 1040 to report your business income and expenses. You may likewise have to complete Schedule SE for self-employment tax. Additional forms might be necessary based on your situation. Knowing which forms to file is essential for accurate reporting and compliance. But what specific deductions can you claim to maximize your benefits? Key Takeaways Sole proprietors report business income and expenses on Schedule C (Form 1040). If net earnings exceed $400, Schedule SE is required for self-employment tax. Form 1099-NEC is used to report nonemployee compensation over $600. Additional forms like Schedules 1 and 2 may be necessary based on the financial situation. Estimated tax payments are filed quarterly using Form 1040-ES if taxes owed exceed $1,000. Understanding Sole Proprietorships When you think about starting a business, a sole proprietorship might be the simplest option available. This structure allows you to own and operate your business without a legal distinction between yourself and the entity. As a sole proprietor, you report your business income and expenses on the Schedule C form, which you file alongside your personal income tax return on Form 1040. Your sole proprietorship tax form helps you track your schedule C income directly, making the process straightforward. The profits and losses are considered your personal income, meaning they’re taxed at your individual tax rate. If your net earnings exceed $400, you’ll likewise need to pay self-employment taxes, calculated using Schedule SE. Since sole proprietors are “disregarded entities,” it’s crucial to understand how these forms work so as to guarantee compliance and accurately report your business activities. Required Tax Forms for Sole Proprietors As a sole proprietor, you’ll need to complete several key tax forms to accurately report your business income and expenses. Schedule C (Form 1040) is crucial for detailing your profits or losses, whereas Schedule SE calculates your self-employment tax if your net earnings exceed $400. Furthermore, depending on your financial situation, you may need to include other forms like Schedules 1 and 2, along with Form 1099-NEC for any nonemployee compensation over $600. Essential Forms Overview Comprehending the fundamental forms required for sole proprietors is essential for managing your business finances effectively. You’ll primarily file Schedule C (Form 1040) to report your business income or loss, which integrates into your personal tax return. If your net earnings exceed $400, you’ll furthermore need Schedule SE to calculate self-employment tax. In addition, Form 1040 is necessary for reporting total income, and you may need Schedules 1 and 2 for specific deductions. If you receive $600 or more in nonemployee compensation, use Form 1099-NEC, whereas payments from cards should be reported on Form 1099-K. For quarterly estimated tax payments, rely on Form 1040-ES. Form Name Purpose Schedule C Report business income or loss Schedule SE Calculate self-employment tax Form 1099-NEC Report nonemployee compensation Form 1040-ES Calculate estimated tax payments Self-Employment Tax Requirements For sole proprietors, comprehension of self-employment tax requirements is crucial since this tax applies to your net earnings from self-employment. You’ll need to file Schedule C (Form 1040) to report your business income or loss, which is included in your personal tax return. If your net earnings are $400 or more, you must calculate your self-employment tax using Schedule SE, covering Social Security and Medicare contributions. Don’t forget about Form 1099-NEC; if you receive $600 or more in nonemployee compensation, it must be reported as income. Furthermore, if you expect to owe $1,000 or more in taxes for the year, you’ll need to make quarterly estimated tax payments using Form 1040-ES. You can likewise deduct half of your self-employment tax. Filing Schedule C and Other Relevant Forms When you’re a sole proprietor, filing Schedule C (Form 1040) is vital for reporting your business income and determining your tax responsibilities. You’ll additionally need to take into account other forms like Schedule SE if your income exceeds $400, along with any additional schedules that may apply based on your unique financial situation. Comprehending these requirements and deadlines is fundamental to guarantee that you accurately report your earnings and comply with tax regulations. Schedule C Overview Filing Schedule C (Form 1040) is vital for sole proprietors who need to report their business income or loss, as it provides a detailed account of profits and expenses for the tax year. You must complete Schedule C if your business income exceeds $400 after expenses. You’ll submit it alongside your federal income tax return. If your net earnings from self-employment reach $400 or more, you’ll likewise need to file Schedule SE to calculate your self-employment tax. Furthermore, you might require Schedule 1 for other income or adjustments, and Form 1040-ES for estimated tax payments. Accurate completion of Schedule C is fundamental for determining your tax liabilities and maximizing deductions for business-related expenses, reducing your taxable income overall. Additional Required Forms Completing Schedule C is just one part of your tax responsibilities as a sole proprietor; you’ll also need to be aware of several other forms that may apply to your situation. Here’s a quick overview of these forms: Form Purpose Schedule SE Calculate self-employment tax if net earnings exceed $400. Form 1099-NEC Report nonemployee compensation of $600 or more. Form 1040-ES Calculate and remit estimated tax payments quarterly. Schedule 1 Report additional income or adjustments to income. Filing Deadlines and Procedures Grasping the deadlines and procedures for filing your tax forms is crucial as a sole proprietor. You’ll need to file Schedule C (Form 1040) by April 15 to report your business income or loss, coinciding with your personal income tax return. If you expect to owe $1,000 or more in taxes, make quarterly estimated tax payments using Form 1040-ES by April 15, June 15, September 15, and January 15 of the following year. Furthermore, if you earn $400 or more from self-employment, you’ll have to file Schedule SE to calculate your self-employment tax. Remember to issue Form 1099-NEC for independent contractors paid $600 or more, and file your federal tax return by the deadline to avoid penalties. Tax Deductions for Sole Proprietorships Comprehending the various tax deductions available can greatly benefit your sole proprietorship, as these deductions help reduce your taxable income and improve your overall financial health. You can deduct ordinary and necessary business expenses, such as office supplies, advertising, and utilities, that are directly related to your operations. If you use a vehicle for business purposes, you can choose between the standard mileage rate or the actual expense method for deductions. Health insurance premiums for yourself and your family are likewise deductible as an adjustment to income on Form 1040. When starting a new business, you can deduct up to $5,000 in start-up costs in the first year, with any remaining costs amortized over 15 years. Furthermore, depreciation on business property allows you to recover asset costs over their useful life, further reducing your taxable income in the years you claim depreciation. Estimated Tax Payments for Sole Proprietors As a sole proprietor, comprehension of your obligation to make estimated tax payments can help you manage your finances effectively. If you expect to owe $1,000 or more in taxes for the year, you’re required to make these payments quarterly using Form 1040-ES. The due dates are April 15, June 15, September 15, and January 15 of the following year. To calculate your estimated tax payments, consider your expected income, deductions, and credits. Here’s a simple overview: Due Date Quarter Covered April 15 Income earned Jan – Mar June 15 Income earned Apr – May September 15 Income earned Jun – Aug January 15 Income earned Sep – Dec If your total tax owed is less than $1,000 after deductions, you won’t need to make estimated payments. Keeping track of your earnings helps you avoid underpayment penalties. Seeking Professional Tax Assistance Many sole proprietors find that seeking professional tax assistance can alleviate the intricacies of managing their tax obligations. Consulting a CPA or tax professional can be invaluable in maneuvering through complex tax forms and ensuring compliance with both federal and state tax laws. These experts help you maximize deductions by identifying all eligible business expenses and credits applicable to your situation. Moreover, engaging a tax advisor can assist you in accurately estimating quarterly tax payments, which helps avoid penalties for underpayment. They provide guidance on completing vital forms like Schedule C and Schedule SE, which are fundamental for reporting business income and calculating self-employment taxes. For new sole proprietors, professional assistance is particularly beneficial in comprehending tax obligations and avoiding common pitfalls associated with self-employment taxation. Frequently Asked Questions Do You File 1099 for Sole Proprietorship? Yes, you do file a 1099 for your sole proprietorship if you’ve paid contractors or freelancers $600 or more for their services during the year. The payer must issue Form 1099-NEC to report this income to the IRS. Furthermore, if you receive payments exceeding $600 through credit/debit cards or third-party networks, you’ll need to report that on Form 1099-K. Always keep accurate records to guarantee compliance with IRS requirements. How Do I File My Taxes as a Sole Proprietor? To file your taxes as a sole proprietor, start by gathering your income and expense records. You’ll need to complete Form 1040 and attach Schedule C, which details your business income and expenses. If your net earnings exceed $400, fill out Schedule SE for self-employment tax. Don’t forget to make quarterly estimated tax payments using Form 1040-ES if you expect to owe $1,000 or more by year-end. Check your state’s requirements too. Do Self-Employed Files Schedule C? Yes, self-employed individuals typically file Schedule C. This form allows you to report income and expenses from your business activities directly on your personal tax return. If your business income exceeds $400 after deducting expenses, you’ll need to complete this form. It helps determine your net profit or loss for the year, which is crucial for calculating your overall tax liability along with potential self-employment taxes. Does a Sole Proprietor Need to File Form 720? You typically don’t need to file Form 720 as a sole proprietor except when your business activities involve specific goods or services subject to federal excise taxes. Most sole proprietors, especially those providing services or selling non-taxable goods, are exempt. Nevertheless, it’s vital to assess your activities carefully. If you find any that trigger excise tax liabilities, then filing Form 720 becomes required to comply with federal regulations. Conclusion In summary, as a sole proprietor, you’ll primarily file Schedule C to report your business income and expenses. If your net earnings exceed $400, you’ll likewise need Schedule SE for self-employment tax calculations. Depending on your situation, additional forms like Schedules 1 and 2 may be necessary. Staying organized and comprehending your tax obligations is essential for maintaining compliance and minimizing potential issues. If needed, don’t hesitate to seek professional tax assistance to navigate the intricacies. Image via Google Gemini This article, "What Tax Form Does a Sole Proprietor File?" was first published on Small Business Trends View the full article

-

As a sole proprietor, you need to understand your tax obligations. When your net earnings exceed $400, you’ll file Schedule C with your Form 1040 to report your business income and expenses. You may likewise have to complete Schedule SE for self-employment tax. Additional forms might be necessary based on your situation. Knowing which forms to file is essential for accurate reporting and compliance. But what specific deductions can you claim to maximize your benefits? Key Takeaways Sole proprietors report business income and expenses on Schedule C (Form 1040). If net earnings exceed $400, Schedule SE is required for self-employment tax. Form 1099-NEC is used to report nonemployee compensation over $600. Additional forms like Schedules 1 and 2 may be necessary based on the financial situation. Estimated tax payments are filed quarterly using Form 1040-ES if taxes owed exceed $1,000. Understanding Sole Proprietorships When you think about starting a business, a sole proprietorship might be the simplest option available. This structure allows you to own and operate your business without a legal distinction between yourself and the entity. As a sole proprietor, you report your business income and expenses on the Schedule C form, which you file alongside your personal income tax return on Form 1040. Your sole proprietorship tax form helps you track your schedule C income directly, making the process straightforward. The profits and losses are considered your personal income, meaning they’re taxed at your individual tax rate. If your net earnings exceed $400, you’ll likewise need to pay self-employment taxes, calculated using Schedule SE. Since sole proprietors are “disregarded entities,” it’s crucial to understand how these forms work so as to guarantee compliance and accurately report your business activities. Required Tax Forms for Sole Proprietors As a sole proprietor, you’ll need to complete several key tax forms to accurately report your business income and expenses. Schedule C (Form 1040) is crucial for detailing your profits or losses, whereas Schedule SE calculates your self-employment tax if your net earnings exceed $400. Furthermore, depending on your financial situation, you may need to include other forms like Schedules 1 and 2, along with Form 1099-NEC for any nonemployee compensation over $600. Essential Forms Overview Comprehending the fundamental forms required for sole proprietors is essential for managing your business finances effectively. You’ll primarily file Schedule C (Form 1040) to report your business income or loss, which integrates into your personal tax return. If your net earnings exceed $400, you’ll furthermore need Schedule SE to calculate self-employment tax. In addition, Form 1040 is necessary for reporting total income, and you may need Schedules 1 and 2 for specific deductions. If you receive $600 or more in nonemployee compensation, use Form 1099-NEC, whereas payments from cards should be reported on Form 1099-K. For quarterly estimated tax payments, rely on Form 1040-ES. Form Name Purpose Schedule C Report business income or loss Schedule SE Calculate self-employment tax Form 1099-NEC Report nonemployee compensation Form 1040-ES Calculate estimated tax payments Self-Employment Tax Requirements For sole proprietors, comprehension of self-employment tax requirements is crucial since this tax applies to your net earnings from self-employment. You’ll need to file Schedule C (Form 1040) to report your business income or loss, which is included in your personal tax return. If your net earnings are $400 or more, you must calculate your self-employment tax using Schedule SE, covering Social Security and Medicare contributions. Don’t forget about Form 1099-NEC; if you receive $600 or more in nonemployee compensation, it must be reported as income. Furthermore, if you expect to owe $1,000 or more in taxes for the year, you’ll need to make quarterly estimated tax payments using Form 1040-ES. You can likewise deduct half of your self-employment tax. Filing Schedule C and Other Relevant Forms When you’re a sole proprietor, filing Schedule C (Form 1040) is vital for reporting your business income and determining your tax responsibilities. You’ll additionally need to take into account other forms like Schedule SE if your income exceeds $400, along with any additional schedules that may apply based on your unique financial situation. Comprehending these requirements and deadlines is fundamental to guarantee that you accurately report your earnings and comply with tax regulations. Schedule C Overview Filing Schedule C (Form 1040) is vital for sole proprietors who need to report their business income or loss, as it provides a detailed account of profits and expenses for the tax year. You must complete Schedule C if your business income exceeds $400 after expenses. You’ll submit it alongside your federal income tax return. If your net earnings from self-employment reach $400 or more, you’ll likewise need to file Schedule SE to calculate your self-employment tax. Furthermore, you might require Schedule 1 for other income or adjustments, and Form 1040-ES for estimated tax payments. Accurate completion of Schedule C is fundamental for determining your tax liabilities and maximizing deductions for business-related expenses, reducing your taxable income overall. Additional Required Forms Completing Schedule C is just one part of your tax responsibilities as a sole proprietor; you’ll also need to be aware of several other forms that may apply to your situation. Here’s a quick overview of these forms: Form Purpose Schedule SE Calculate self-employment tax if net earnings exceed $400. Form 1099-NEC Report nonemployee compensation of $600 or more. Form 1040-ES Calculate and remit estimated tax payments quarterly. Schedule 1 Report additional income or adjustments to income. Filing Deadlines and Procedures Grasping the deadlines and procedures for filing your tax forms is crucial as a sole proprietor. You’ll need to file Schedule C (Form 1040) by April 15 to report your business income or loss, coinciding with your personal income tax return. If you expect to owe $1,000 or more in taxes, make quarterly estimated tax payments using Form 1040-ES by April 15, June 15, September 15, and January 15 of the following year. Furthermore, if you earn $400 or more from self-employment, you’ll have to file Schedule SE to calculate your self-employment tax. Remember to issue Form 1099-NEC for independent contractors paid $600 or more, and file your federal tax return by the deadline to avoid penalties. Tax Deductions for Sole Proprietorships Comprehending the various tax deductions available can greatly benefit your sole proprietorship, as these deductions help reduce your taxable income and improve your overall financial health. You can deduct ordinary and necessary business expenses, such as office supplies, advertising, and utilities, that are directly related to your operations. If you use a vehicle for business purposes, you can choose between the standard mileage rate or the actual expense method for deductions. Health insurance premiums for yourself and your family are likewise deductible as an adjustment to income on Form 1040. When starting a new business, you can deduct up to $5,000 in start-up costs in the first year, with any remaining costs amortized over 15 years. Furthermore, depreciation on business property allows you to recover asset costs over their useful life, further reducing your taxable income in the years you claim depreciation. Estimated Tax Payments for Sole Proprietors As a sole proprietor, comprehension of your obligation to make estimated tax payments can help you manage your finances effectively. If you expect to owe $1,000 or more in taxes for the year, you’re required to make these payments quarterly using Form 1040-ES. The due dates are April 15, June 15, September 15, and January 15 of the following year. To calculate your estimated tax payments, consider your expected income, deductions, and credits. Here’s a simple overview: Due Date Quarter Covered April 15 Income earned Jan – Mar June 15 Income earned Apr – May September 15 Income earned Jun – Aug January 15 Income earned Sep – Dec If your total tax owed is less than $1,000 after deductions, you won’t need to make estimated payments. Keeping track of your earnings helps you avoid underpayment penalties. Seeking Professional Tax Assistance Many sole proprietors find that seeking professional tax assistance can alleviate the intricacies of managing their tax obligations. Consulting a CPA or tax professional can be invaluable in maneuvering through complex tax forms and ensuring compliance with both federal and state tax laws. These experts help you maximize deductions by identifying all eligible business expenses and credits applicable to your situation. Moreover, engaging a tax advisor can assist you in accurately estimating quarterly tax payments, which helps avoid penalties for underpayment. They provide guidance on completing vital forms like Schedule C and Schedule SE, which are fundamental for reporting business income and calculating self-employment taxes. For new sole proprietors, professional assistance is particularly beneficial in comprehending tax obligations and avoiding common pitfalls associated with self-employment taxation. Frequently Asked Questions Do You File 1099 for Sole Proprietorship? Yes, you do file a 1099 for your sole proprietorship if you’ve paid contractors or freelancers $600 or more for their services during the year. The payer must issue Form 1099-NEC to report this income to the IRS. Furthermore, if you receive payments exceeding $600 through credit/debit cards or third-party networks, you’ll need to report that on Form 1099-K. Always keep accurate records to guarantee compliance with IRS requirements. How Do I File My Taxes as a Sole Proprietor? To file your taxes as a sole proprietor, start by gathering your income and expense records. You’ll need to complete Form 1040 and attach Schedule C, which details your business income and expenses. If your net earnings exceed $400, fill out Schedule SE for self-employment tax. Don’t forget to make quarterly estimated tax payments using Form 1040-ES if you expect to owe $1,000 or more by year-end. Check your state’s requirements too. Do Self-Employed Files Schedule C? Yes, self-employed individuals typically file Schedule C. This form allows you to report income and expenses from your business activities directly on your personal tax return. If your business income exceeds $400 after deducting expenses, you’ll need to complete this form. It helps determine your net profit or loss for the year, which is crucial for calculating your overall tax liability along with potential self-employment taxes. Does a Sole Proprietor Need to File Form 720? You typically don’t need to file Form 720 as a sole proprietor except when your business activities involve specific goods or services subject to federal excise taxes. Most sole proprietors, especially those providing services or selling non-taxable goods, are exempt. Nevertheless, it’s vital to assess your activities carefully. If you find any that trigger excise tax liabilities, then filing Form 720 becomes required to comply with federal regulations. Conclusion In summary, as a sole proprietor, you’ll primarily file Schedule C to report your business income and expenses. If your net earnings exceed $400, you’ll likewise need Schedule SE for self-employment tax calculations. Depending on your situation, additional forms like Schedules 1 and 2 may be necessary. Staying organized and comprehending your tax obligations is essential for maintaining compliance and minimizing potential issues. If needed, don’t hesitate to seek professional tax assistance to navigate the intricacies. Image via Google Gemini This article, "What Tax Form Does a Sole Proprietor File?" was first published on Small Business Trends View the full article