All Activity

- Past hour

-

Cloudflare yesterday announced its new Markdown for Agents feature, which serves machine-friendly versions of web content alongside traditional human-facing pages. Cloudflare described the update as a response to the rise of AI crawlers and agentic browsing. When a client requests text/markdown, Cloudflare fetches the HTML from the origin server, converts it at the edge, and returns a Markdown version. The response also includes a token estimate header intended to help developers manage context windows. Early reactions focused on the efficiency gains, as well as the broader implications of serving alternate representations of web content. What’s happening. Cloudflare, which powers roughly 20% of the web, said Markdown for Agents uses standard HTTP content negotiation. If a client sends an Accept: text/markdown header, Cloudflare converts the HTML response on the fly and returns Markdown. The response includes Vary: accept, so caches store separate variants. Cloudflare positioned the opt-in feature as part of a shift in how content is discovered and consumed, with AI crawlers and agents benefiting from structured, lower-overhead text. Markdown can cut token usage by up to 80% compared to HTML, Cloudflare said. Security concern. SEO consultant David McSweeney said Cloudflare’s Markdown for Agents feature could make AI cloaking trivial because the Accept: text/markdown header is forwarded to origin servers, effectively signaling that the request is from an AI agent. A standard request returns normal content, while a Markdown request can trigger a different HTML response that Cloudflare then converts and delivers to the AI, McSweeney showed on LinkedIn. The concern: sites could inject hidden instructions, altered product data, or other machine-only content, creating a “shadow web” for bots unless the header is stripped before reaching the origin. Google and Bing’s markdown smackdown. Recent comments from Google and Microsoft representatives discourage publishers from creating separate markdown pages for large language models. Google’s John Mueller said: “In my POV, LLMs have trained on – read & parsed – normal web pages since the beginning, it seems a given that they have no problems dealing with HTML. Why would they want to see a page that no user sees? And, if they check for equivalence, why not use HTML?” And Microsoft’s Fabrice Canel said: “Really want to double crawl load? We’ll crawl anyway to check similarity. Non-user versions (crawlable AJAX and like) are often neglected, broken. Humans eyes help fixing people and bot-viewed content. We like Schema in pages. AI makes us great at understanding web pages. Less is more in SEO !” Cloudflare’s feature doesn’t create a second URL. However, it generates different representations based on request headers. The case against markdown. Technical SEO consultant Jono Alderson said that once a machine-specific representation exists, platforms must decide whether to trust it, verify it against the human-facing version, or ignore it: “When you flatten a page into markdown, you don’t just remove clutter. You remove judgment, and you remove context.” “The moment you publish a machine-only representation of a page, you’ve created a second candidate version of reality. It doesn’t matter if you promise it’s generated from the same source or swear that it’s ‘the same content’. From the outside, a system now sees two representations and has to decide which one actually reflects the page.” Dig deeper. Why LLM-only pages aren’t the answer to AI search Why we care. Cloudflare’s move could make AI ingestion cheaper and cleaner. But could it be considered cloaking if you’re serving different content to humans and crawlers? To be continued… View the full article

Cloudflare yesterday announced its new Markdown for Agents feature, which serves machine-friendly versions of web content alongside traditional human-facing pages. Cloudflare described the update as a response to the rise of AI crawlers and agentic browsing. When a client requests text/markdown, Cloudflare fetches the HTML from the origin server, converts it at the edge, and returns a Markdown version. The response also includes a token estimate header intended to help developers manage context windows. Early reactions focused on the efficiency gains, as well as the broader implications of serving alternate representations of web content. What’s happening. Cloudflare, which powers roughly 20% of the web, said Markdown for Agents uses standard HTTP content negotiation. If a client sends an Accept: text/markdown header, Cloudflare converts the HTML response on the fly and returns Markdown. The response includes Vary: accept, so caches store separate variants. Cloudflare positioned the opt-in feature as part of a shift in how content is discovered and consumed, with AI crawlers and agents benefiting from structured, lower-overhead text. Markdown can cut token usage by up to 80% compared to HTML, Cloudflare said. Security concern. SEO consultant David McSweeney said Cloudflare’s Markdown for Agents feature could make AI cloaking trivial because the Accept: text/markdown header is forwarded to origin servers, effectively signaling that the request is from an AI agent. A standard request returns normal content, while a Markdown request can trigger a different HTML response that Cloudflare then converts and delivers to the AI, McSweeney showed on LinkedIn. The concern: sites could inject hidden instructions, altered product data, or other machine-only content, creating a “shadow web” for bots unless the header is stripped before reaching the origin. Google and Bing’s markdown smackdown. Recent comments from Google and Microsoft representatives discourage publishers from creating separate markdown pages for large language models. Google’s John Mueller said: “In my POV, LLMs have trained on – read & parsed – normal web pages since the beginning, it seems a given that they have no problems dealing with HTML. Why would they want to see a page that no user sees? And, if they check for equivalence, why not use HTML?” And Microsoft’s Fabrice Canel said: “Really want to double crawl load? We’ll crawl anyway to check similarity. Non-user versions (crawlable AJAX and like) are often neglected, broken. Humans eyes help fixing people and bot-viewed content. We like Schema in pages. AI makes us great at understanding web pages. Less is more in SEO !” Cloudflare’s feature doesn’t create a second URL. However, it generates different representations based on request headers. The case against markdown. Technical SEO consultant Jono Alderson said that once a machine-specific representation exists, platforms must decide whether to trust it, verify it against the human-facing version, or ignore it: “When you flatten a page into markdown, you don’t just remove clutter. You remove judgment, and you remove context.” “The moment you publish a machine-only representation of a page, you’ve created a second candidate version of reality. It doesn’t matter if you promise it’s generated from the same source or swear that it’s ‘the same content’. From the outside, a system now sees two representations and has to decide which one actually reflects the page.” Dig deeper. Why LLM-only pages aren’t the answer to AI search Why we care. Cloudflare’s move could make AI ingestion cheaper and cleaner. But could it be considered cloaking if you’re serving different content to humans and crawlers? To be continued… View the full article -

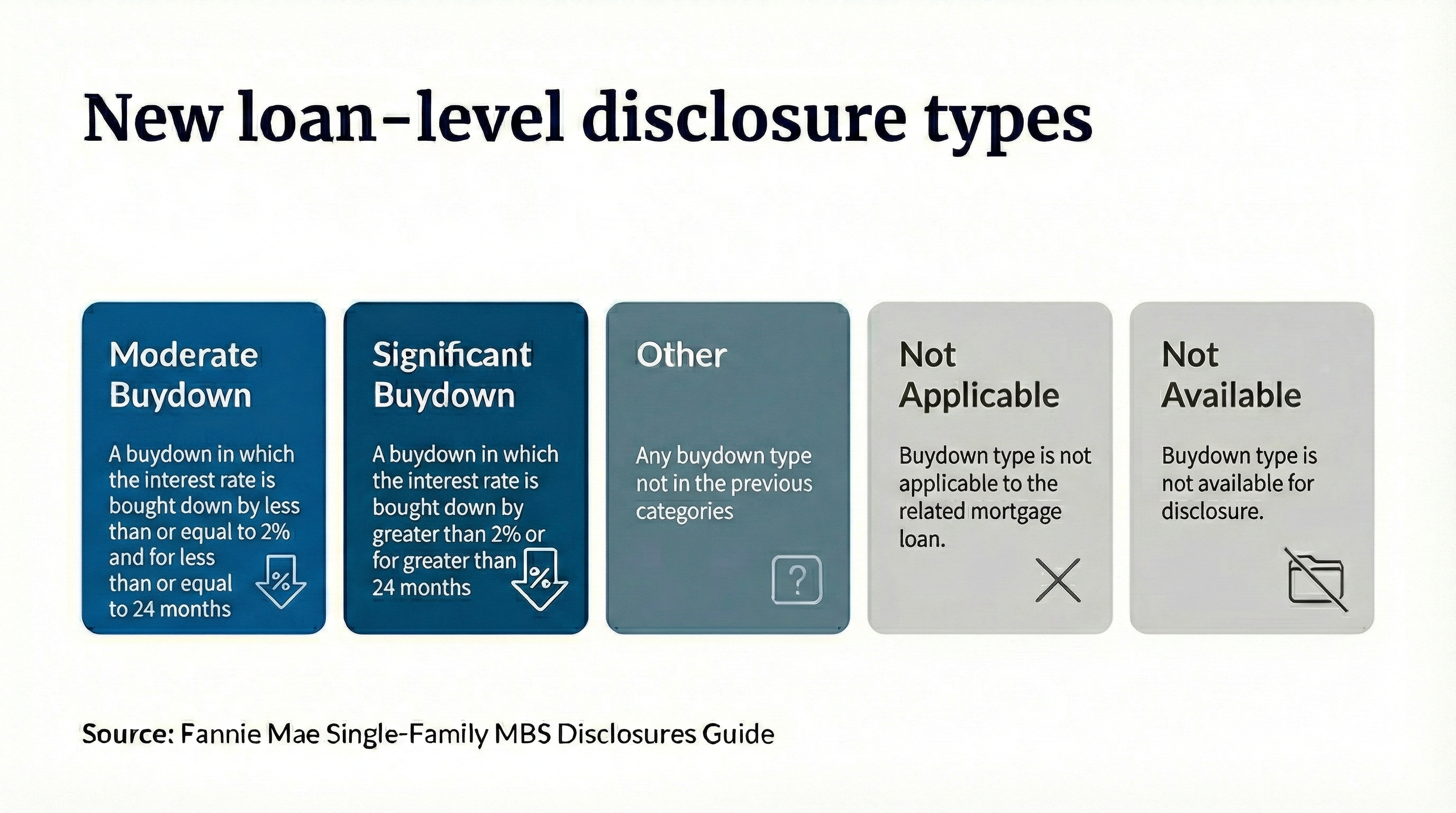

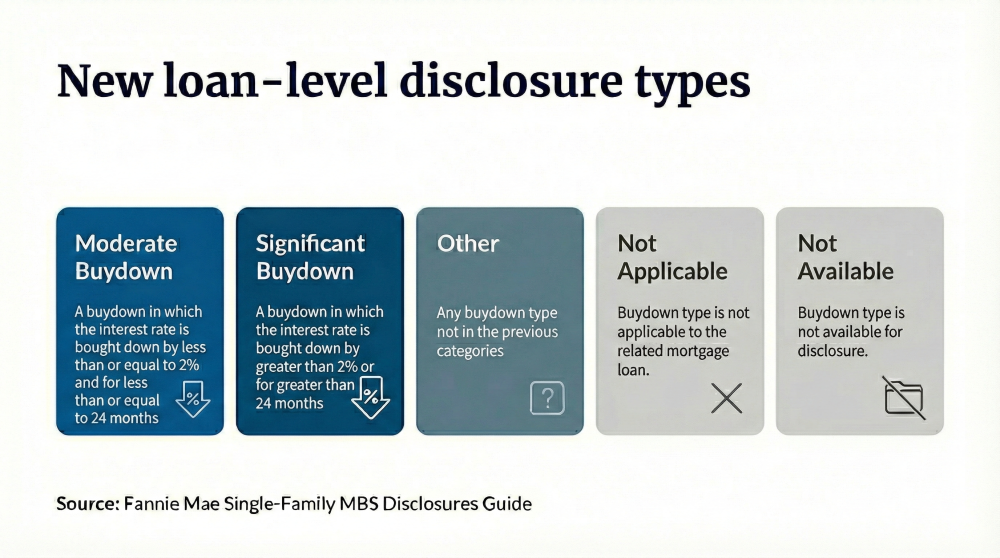

Fannie Mae and Freddie Mac will add loan-level buydown data to MBS this spring, giving investors clearer insight into prepayment risk tied to temporary rate incentives. View the full article

-

Google Ads is rolling out a feature that lets advertisers calculate conversion value for new customers based on a target return on ad spend (ROAS), automatically generating a suggested value instead of relying on manual estimates. The update is designed for campaigns using new customer acquisition goals, where advertisers want to bid more aggressively to attract first-time buyers. How it works. Advertisers enter their desired ROAS target for new customers, and Google Ads proposes a conversion value aligned with that goal. The system removes some of the guesswork involved in estimating how much a new customer should be worth in bidding models. The feature doesn’t yet adjust dynamically at the auction, campaign, or product level. Advertisers still apply the value at a broader setting rather than letting the system vary bids based on context. Why we care. Assigning the right value to a new customer is a weak spot in performance bidding. Many advertisers manually set a flat value that doesn’t always reflect profitability or long-term goals. By tying suggested conversion values to a target ROAS, advertisers can now optimise towards a more strategy-driven bidding, potentially improving how acquisition campaigns balance growth and efficiency. What advertisers are saying. Early reactions suggest the feature is a meaningful improvement over static manual inputs. Founder of Savvy Revenue, Andrew Lolk argues the next step would be auction-level intelligence that adjusts values depending on campaign or product performance. What to watch. If Google expands the feature to support more granular adjustments, it could further reshape how advertisers structure acquisition strategies and value lifetime customer growth. For now, the tool offers a more structured way to calculate new customer value. First seen. This update was first spotted by Founder and Digital Marketer Andrew Lolk who showed the new setting on LinkedIn. View the full article

-

Software work rarely falls apart because of bad ideas; it unravels when timelines slip, dependencies clash and expectations drift. That’s where delivery planning becomes critical. Instead of reacting to chaos, teams shape a clear delivery plan that aligns scope, sequencing and capacity before code hits production. What Is Delivery Planning? Delivery planning is the structured process of organizing how software work moves from approved requirements to production release. It brings together product managers, delivery managers, developers, QA engineers and sometimes DevOps to decide what will be delivered, in what order and within what time frame. The process typically starts with prioritizing backlog items, reviewing technical dependencies and assessing team capacity. From there, the group maps work into iterations or release increments, stress-tests assumptions and adjusts for risks. Trade-offs are discussed openly, especially when scope, time and resources compete. The central output of this effort is a delivery plan, a practical roadmap that outlines milestones, release targets and the sequence of work needed to ship reliably. ProjectManager is an award-winning project portfolio management software that offers advanced planning, scheduling and tracking tools for software development and IT teams, allowing them to create visual roadmaps for their delivery plans, allocate resources, track costs and manage waterfall and agile workflows. Additionally, ProjectManager integrates with Jira, Azure Devops and features an open API that facilitates integration with other software development tools. Get started for free today. /wp-content/uploads/2024/02/light-mode-CTA-1600x918.jpgLearn more What Is a Delivery Plan? A delivery plan is a structured schedule that outlines how approved work will be executed and released within a defined timeframe. It specifies deliverables, sequencing, milestones, dependencies and target release dates. In IT, software and product development environments, a delivery plan translates strategic objectives and prioritized scope into a coordinated project timeline that guides teams from build through testing and deployment. When to Make a Delivery Plan In IT and product environments, a delivery plan is created once the project scope has been approved and the team is preparing to commit to release dates. It is typically used before major releases, large initiatives or cross-team programs where coordination, sequencing and realistic timelines must be agreed upon before execution begins. Here are the most common scenarios in which a delivery plan helps organizations plan and schedule work. Enterprise IT & Digital Transformation Projects Coordinating multi-system upgrades that require strict sequencing and integration testing. Planning phased ERP, CRM or infrastructure modernization initiatives across departments. Aligning cybersecurity improvements with regulatory deadlines and audit requirements. Managing cloud migration programs involving internal teams and external vendors. Structuring data center consolidation projects with clearly defined transition milestones. Software Development Organizing major application releases that bundle multiple new features together. Planning incremental feature rollouts across several sprint cycles. Coordinating backend, frontend and DevOps deployment activities for production releases. Preparing performance optimization initiatives with staged testing checkpoints. Managing refactoring efforts while maintaining ongoing feature development commitments. Product Management Translating roadmap priorities into quarterly or release-based execution plans. Structuring beta launches before full public product availability. Coordinating go-to-market readiness alongside engineering release timelines. Managing feature bundles tied to contractual or enterprise customer commitments. Planning market expansion releases that introduce region-specific capabilities. What Should Be Included In a Delivery Plan? A delivery plan should clearly outline what will be delivered, in what order, by whom and by when, so execution decisions are anchored in visible, agreed-upon commitments. Objectives and Work Scope Clear objectives keep the team focused on outcomes instead of just activity. Defining the work scope prevents uncontrolled expansion once development begins. When both are written into the delivery plan, everyone understands what problem is being solved and what is intentionally excluded, reducing confusion, rework and misaligned expectations. Project Deliverables and Features In IT and software environments, project deliverables are the concrete outputs that must be completed and released. These can include functional features, APIs, integrations, infrastructure updates, configuration changes or performance improvements. Each deliverable represents something testable and releasable, not just a task or internal activity. /wp-content/uploads/2025/08/Project-deliverables-template-600x296.pngFree project deliverables template for Excel Listing deliverables clearly shapes the delivery plan because timelines are built around them. Sequencing decisions, resource allocation and release groupings all depend on what must be shipped. When deliverables are well defined, teams can estimate effort accurately, identify dependencies early and avoid vague commitments that lead to missed deadlines. Delivery Plan Timeline A delivery plan timeline is built from scheduled deliverables, key milestones, dependency links and target release dates. It shows when major features are expected to be completed, when reviews occur and when releases go live. Milestones mark decision points or readiness checks, while dependencies clarify what must finish before the next activity begins. /wp-content/uploads/2024/10/Gantt-chart-template-for-Excel-600x264.pngFree Gantt chart template for Excel Teams usually represent a delivery plan timeline using Gantt charts, roadmap views or structured release calendars. Gantt charts are common because they visualize sequencing and dependencies clearly. Product roadmaps are often used for higher-level communication. In some environments, shared planning boards or portfolio tools provide timeline views aligned with sprint cycles and release windows. Release Structure A release structure defines how completed deliverables are organized and deployed to users. It determines the pattern the team follows, including how functionality is grouped and how frequently releases occur. Within delivery planning, the release structure clarifies whether work is shipped continuously, in fixed cycles or bundled into coordinated releases aligned with business priorities. Common release structures include continuous delivery, where updates are deployed frequently, and time-based models such as monthly or quarterly releases. Some teams use phased rollouts to reduce exposure, while others package features into major version launches. Enterprise programs may synchronize releases across multiple systems and teams. The chosen release structure shapes sequencing decisions, testing intensity and stakeholder expectations. When the structure is unclear, confusion builds around what ships and when. Clear release logic keeps the delivery plan realistic and aligned with deployment capabilities. Resource Plan A resource plan within a delivery plan defines who will perform the work, what skills are required and how availability aligns with the delivery timeline. It maps people, roles and supporting assets to specific deliverables. In IT and software development, this ensures commitments are grounded in real capacity rather than assumed bandwidth. /wp-content/uploads/2023/03/Resource-Plan-Screenshot-600x213.jpgFree resource plan template for Excel Some of the most important roles to include in a resource plan within a delivery plan for software development or IT projects are: Frontend developers assigned to user interface feature development. Backend engineers responsible for APIs and database logic. QA analysts allocated for manual and automated testing cycles. DevOps engineers supporting CI/CD pipelines and deployments. UX designers contributing wireframes and usability validation. Cloud infrastructure environments required for staging and production. External vendors providing integrations or specialized technical services. Risk Register & Risk Mitigation Plan A risk register in a delivery plan is a structured list of identified threats that could impact timelines, scope or quality. It documents each risk, its likelihood, potential impact and assigned owner. In IT and software projects, this often includes technical uncertainty, integration challenges, resource gaps or external dependencies. /wp-content/uploads/2024/11/Risk-assessment-template-screenshot-600x212.pngFree risk assessment template for Excel A risk mitigation plan outlines the specific actions the team will take to reduce the probability or impact of identified risks. It may include contingency timelines, fallback technical approaches, additional testing cycles or escalation protocols. Within delivery planning, mitigation planning prevents reactive decision-making when issues arise during execution. Governance Roles Governance within a delivery plan defines how decisions are made, who approves scope changes and how performance is monitored. In IT and software projects, governance ensures delivery stays aligned with business priorities, budget constraints and risk tolerance while maintaining clear accountability for outcomes. Executive Sponsor: Provides strategic direction and approves major scope, budget or timeline changes. Steering Committee: Reviews progress, resolves escalated issues and validates continued business alignment. Product Owner: Approves backlog priorities and confirms feature-level acceptance decisions. Delivery Manager: Monitors execution performance and enforces agreed planning controls. Technical Authority: Validates architectural decisions and ensures compliance with technical standards. Communication Plan A communication plan within a delivery plan defines how progress, risks and changes are shared with stakeholders. It outlines what information is communicated, how often updates occur and through which channels. In IT and software environments, clear communication prevents misaligned expectations between engineering teams, product leadership and business sponsors. Defined reporting cadence such as weekly delivery status updates. Stakeholder audience list with communication responsibilities assigned. Standard status report format including milestones and risks. Escalation channels for urgent blockers or critical issues. Release announcement templates for internal and external audiences. Integration of dashboard metrics from project management tools. Meeting structure for sprint reviews and release readiness checkpoints. Who Participates in the Delivery Planning Process Although many voices contribute, accountability typically sits with the delivery manager or project manager overseeing execution. That person facilitates planning sessions, aligns scope with capacity and ensures commitments are realistic. In product-led environments, a product manager may co-lead, but ownership of the delivery planning process remains clearly defined. Here’s a quick overview of the key roles and responsibilities in the delivery planning process. Product Manager: Defines priorities, clarifies business outcomes and confirms what must be delivered in each release. Protects value, challenges unnecessary scope and ensures planning decisions align with customer and stakeholder expectations. Delivery Manager: Coordinates planning cadence, manages timelines and tracks dependencies across teams. Translates strategic goals into executable increments and holds the group accountable for realistic commitments and achievable release targets. Engineering Lead: Evaluates technical complexity, identifies architectural constraints and flags sequencing risks. Shapes effort estimates and determines whether proposed timelines are feasible given existing systems and technical debt. Developers: Contribute effort estimates, surface hidden dependencies and explain implementation constraints. Provide practical insight that grounds planning discussions in reality, preventing overly optimistic schedules disconnected from actual build effort. QA Lead: Defines testing scope, automation coverage and release readiness criteria. Ensures sufficient time is allocated for validation so quality is not sacrificed under deadline pressure. DevOps Engineer: Reviews deployment pipelines, infrastructure readiness and environment constraints. Ensures releases can be deployed smoothly without last-minute operational bottlenecks. Business Sponsor: Validates timelines against external commitments. Confirms that release targets support market, regulatory or contractual obligations while understanding the trade-offs required to meet those dates. Main Steps in the Delivery Planning Process Delivery planning is not a a mere documentation exercise. It is a series of working sessions where product, engineering and delivery leaders make real commitments, challenge assumptions and decide what can realistically ship. The steps below reflect the conversations and decisions that turn ambition into an executable delivery plan. 1. Clarify Overall Project Objectives & Success Criteria The process usually begins with the product manager explaining the business outcome the initiative must achieve. The executive sponsor confirms why it matters now. The delivery manager pushes for clarity: what problem are we solving, and what result proves success? Engineering leaders question feasibility early, while the group agrees on measurable targets that will later determine whether the release actually delivered value. 2. Define the Work Scope and Identify Deliverables After alignment on outcomes, the team breaks the idea into concrete work. Product walks through prioritized features. Engineering challenges assumptions and flags hidden complexity. QA raises questions about testability. The delivery manager keeps the discussion focused on what will be included and what will not. Together, they separate essential functionality from optional enhancements before effort discussions begin. 3. Identify Task Dependencies and Constraints Before anyone talks dates, the engineering lead maps technical sequencing realities. Backend may need to finish before frontend begins. DevOps confirms environment readiness. If vendors or external systems are involved, timelines are validated directly with them. Compliance or security representatives call out mandatory checkpoints. The delivery manager documents these constraints so the plan reflects real-world blockers, not assumptions. 4. Sequence Work With constraints visible, the group debates order. Product argues for early delivery of high-impact features. Engineering weighs complexity and risk. The delivery manager tests whether value-driven sequencing conflicts with technical flow. The team decides whether to release incrementally or bundle functionality into phases. By the end of this step, the order of execution reflects deliberate trade-offs, not optimism. 5. Estimate Required Effort and Validate Capacity Developers provide effort estimates based on experience, not pressure. The engineering lead reviews whether specialists are overallocated and balances workload. The delivery manager compares proposed work against actual team availability, including vacations and parallel initiatives. If the math does not work, scope or sequencing is adjusted. No timeline is accepted until capacity and workload are visibly aligned. 6. Build and Review the Delivery Timeline Once estimates are accepted, the delivery manager maps work against proposed release windows. Milestones are proposed and challenged. QA confirms testing windows are realistic. DevOps validates deployment timing. Integration points across teams are reviewed out loud. The draft timeline is pressure-tested in the room before being shared more broadly to stakeholders. 7. Agree on Risk Responses and Escalation Paths Before closing the session, the team openly discusses what could derail the plan. Engineering highlights technical uncertainty. Product identifies market timing risks. The delivery manager asks what happens if assumptions fail. Mitigation actions are assigned, buffers are added where justified and clear escalation paths are confirmed so issues can move quickly if they surface. ProjectManager Can Help with IT & Software Development Projects ProjectManager is an award-winning project portfolio management software equipped with powerful features for IT and software development teams, such as Gantt chart roadmaps that can be used to manage individual delivery plans and complete project portfolios, dashboards for monitoring resource utilization, project costs and progress in real time and kanban boards that are ideal for agile sprints and iterative planning. ProjectManager also has robust resource management features such as workload charts to balance teams’ workloads and timesheets for detailed time tracking. On top of that, ProjectManager integrates with Jira and Azure DevOps and has an open API so that organizations can integrate its powerful project portfolio management functionality with their favorite tools. Watch the video below to learn more! The post Delivery Planning In IT & Software Development: Making a Delivery Plan appeared first on ProjectManager. View the full article

- Today

-

Mortgage delinquencies increased across loan types, and while 30-day late payments showed overall improvement, later-stage distress worsened. View the full article

-

US Secretary of State cancels attendance at last minute in move that EU official called ‘insane’View the full article

-

Ellie Frazier first started posting content three years ago, sharing day-in-the-life vlogs and content tips for fellow creators. As her following grew, she began noticing other creators posting videos with uncannily similar scripts to her own. The clips felt the same. The editing style, identical. In one example, Frazier stretched in front of a window; another creator stretched in front of a window. Frazier chopped vegetables; the other creator chopped an orange. On its own, that might not seem especially striking. But the voiceover script used by the other creator was also almost verbatim Frazier’s words. “There’s a very stark difference between taking inspiration from everybody and giving credit, versus stealing somebody’s voiceover script word for word multiple times in a row,” says Frazier in a recent post. “Taking credit in the comments for it being their own work.” Plagiarism—presenting another person’s ideas, words, images, or work as your own without credit—while often difficult to litigate, is a cardinal sin in most industries. And yet social media largely operates as a law unto itself. TikTok will remove content that “violates or infringes someone else’s intellectual property rights, including copyright and trademark.” However, many posts on the platform do not clearly meet the legal threshold for copyrightable intellectual property, meaning enforcement is often left to creators themselves. With swaths of content uploaded every day, copycat creators frequently weigh the risk of being discovered against the possibility of profiting from a viral concept with minimal effort. There is even content devoted to explaining exactly how to plagiarize others’ work. Determining who copied whom is also largely a futile exercise. On a platform that thrives on mimicry, true originality is rare. The lifecycle of a trend is familiar: One person creates an original video. If it goes viral, thousands copy it. Some tag the original creator. But as the trend snowballs, that credit is often lost to the algorithm. Once it has been replicated enough times to be labeled a trend, the concept is widely regarded as fair game. Frazier isn’t the first to spotlight the growing issue of digital plagiarism. In a first-of-its-kind lawsuit brought in 2024, one TikTok creator attempted to sue another for copying her “neutral, beige, and cream aesthetic” and posting content with “identical styling, tone, camera angle and/or text.” More than a year later, the so-called “Sad Beige Lawsuit” was dismissed after the claimant chose not to move forward. Imitation may be described as the sincerest form of flattery, but online plagiarism ultimately benefits no one. The original creator loses credit for their idea. The copycat forfeits an opportunity to develop a distinct voice. And audiences are left scrolling through an endless stream of low-quality videos, each one nearly indistinguishable from the last. View the full article

-

Head of Wall Street bank calls attorney a ‘tremendous’ person hours after she quit over links to Jeffrey EpsteinView the full article

-

As outrage spreads over energy-hungry data centers, politicians from President Donald The President to local lawmakers have found rare bipartisan agreement over insisting that tech companies — and not regular people — must foot the bill for the exorbitant amount of electricity required for artificial intelligence. But that might be where the agreement ends. The price of powering data centers has become deeply intertwined with concerns over the cost of living, a dominant issue in the upcoming midterm elections that will determine control of Congress and governors’ offices. Some efforts to address the challenge may be coming too late, with energy costs on the rise. And even though tech giants are pledging to pay their “fair share,” there’s little consensus on what that means. “‘Fair share’ is a pretty squishy term, and so it’s something that the industry likes to say because ‘fair’ can mean different things to different people,” said Ari Peskoe, who directs the Electricity Law Initiative at Harvard University. It’s a shift from last year, when states worked to woo massive data center projects and The President directed his administration to do everything it could to get them electricity. Now there’s a backlash as towns fight data center projects and some utilities’ electricity bills have risen quickly. Anger over the issue has already had electoral consequences, with Democrats ousting two Republicans from Georgia’s utility regulatory commission in November. “Voters are already connecting the experience of these facilities with their electricity costs and they’re going to increasingly want to know how government is going to navigate that,” said Christopher Borick, a pollster and director of the Muhlenberg College Institute of Public Opinion. Energy race stokes concerns Data centers are sprouting across the U.S., as tech giants scramble to meet worldwide demand for chatbots and other generative AI products that require large amounts of computing power to train and operate. The buildings look like giant warehouses, some dwarfing the footprints of factories and stadiums. Some need more power than a small city, more than any utility has ever supplied to a single user, setting off a race to build more power plants. The demand for electricity can have a ripple effect that raises prices for everyone else. For example, if utilities build more power plants or transmission lines to serve them, the cost can be spread across all ratepayers. Concerns have dovetailed with broader questions about the cost of living, as well as fears about the powerful influence of tech companies and the impact of artificial intelligence. The President continues to embrace artificial intelligence as a top economic and national security priority, although he seemed to acknowledge the backlash last month by posting on social media that data centers “must ‘pay their own way.’” At other times, he has brushed concerns aside, declaring that tech giants are building their own power plants, and Energy Secretary Chris Wright contends that data centers don’t inflate electricity bills — disputing what consumer advocates and independent analysts say. States moving to regulate Some states and utilities have started to identify ways to get data centers to pay for their costs. They’ve required tech companies to buy electricity in long-term contracts, pay for the power plants and transmission upgrades they need and make big down payments in case they go belly-up or decide later they don’t need as much electricity. But it might be more complicated than that. Those rules can’t fix the short-term problem of ravenous demand for electricity that is outpacing the speed of power plant construction, analysts say. “What do you do when Big Tech, because of the very profitable nature of these data centers, can simply outbid grandma for power in the short run?” Abe Silverman, a former utility regulatory lawyer and an energy researcher at Johns Hopkins University. “That is, I think, going to be the real challenge.” Some consumer advocates say tech companies’ fair share should also include the rising cost of electricity, grid equipment, or natural gas that’s driven by their demand. In Oregon, which passed a law to protect smaller ratepayers from data centers’ power costs, a consumer advocacy group is jousting with the state’s largest utility, Portland General Electric, over its plan on how to do that. Meanwhile, consumer advocates in various states — including Indiana, Georgia, and Missouri — are warning that utilities could foist the cost of data center-driven buildouts onto regular ratepayers there. Pushback from lawmakers, governors Utilities have pledged to ensure electric rates are fair. But in some places it may be too late. For instance, in the mid-Atlantic grid territory from New Jersey to Illinois, consumer advocates and analysts have pegged billions of dollars in rate increases hitting the bills of regular Americans on data center demand. Legislation, meanwhile, is flooding into Congress and statehouses to regulate data centers. Democrats’ bills in Congress await Republican cosponsors, while lawmakers in a number of states are floating moratoriums on new data centers, drafting rules for regulators to shield regular ratepayers and targeting data center tax breaks and utility profits. Governors — including some who worked to recruit data centers to their states — are increasingly talking tough. Arizona Gov. Katie Hobbs, a Democrat running for reelection this year, wants to impose a penny-a-gallon water fee on data centers and get rid of the sales tax exemption there that most states offer data centers. She called it a $38 million “corporate handout.” “It’s time we make the booming data center industry work for the people of our state, rather than the other way around,” she said in her state-of-the-state address. Blame for rising energy costs Energy costs are projected to keep rising in 2026. Republicans in Washington are pointing the finger at liberal state energy policies that favor renewable energy, suggesting they have driven up transmission costs and frayed supply by blocking fossil fuels. “Americans are not paying higher prices because of data centers. There’s a perception there, and I get the perception, but it’s not actually true,” said Wright, The President’s energy secretary, at a news conference earlier this month. The struggle to assign blame was on display last week at a four-hour U.S. House subcommittee hearing with members of the Federal Energy Regulatory Commission. Republicans encouraged FERC members to speed up natural gas pipeline construction while Democrats defended renewable energy and urged FERC to limit utility profits and protect residential ratepayers from data center costs. FERC’s chair, Laura Swett, told Rep. Greg Landsman, D-Ohio, that she believes data center operators are willing to cover their costs and understand that it’s important to have community support. “That’s not been our experience,” Landsman responded, saying projects in his district are getting tax breaks, sidestepping community opposition and costing people money. “Ultimately, I think we have to get to a place where they pay everything.” —Marc Levy, Associated Press View the full article

-

The companies are among a number the Pentagon believes could pose a threat to American national securityView the full article

-

A new report by Intuit’s Mailchimp highlights the critical importance of the opt-in moment for brands aiming to foster strong relationships with consumers. Titled The Art of the Opt-In: Why List Building is Only the Beginning, the study reveals that building quality email and SMS lists goes far beyond simply assembling contacts; it’s about creating trust, personalizing experiences, and ultimately driving engagement. Matt Cimino, product manager at Intuit Mailchimp, emphasizes, “As tracking and re-targeting become more complex, the opt-in stands out as one of the few moments when a brand can earn a direct relationship – with permission.” The insights from this report offer small business owners a roadmap to navigate the opt-in landscape effectively. One of the report’s major findings indicates a disconnection between what marketers believe consumers are willing to share and the reality of consumer privacy concerns. For instance, while 65% of brands ask for a phone number during sign-up, only 28% of consumers are comfortable providing that information. This gap underscores the need for brands to rethink their approach to data collection, focusing on high-intent actions like browsing and checkout moments to optimize their opt-in strategies. The report showcases that many marketers—nearly all of whom maintain email and SMS lists—struggle with quality. Less than a third consider their lists “very high quality,” and only 8% report opt-in conversion rates exceeding 20%. These disappointing statistics may stem from a lack of sophisticated tools and insights; only 20% of marketers fully automate their email and text campaigns, and just a third are confident in tracking sign-up sources. Trust also appears to be generational. The study found that while 39% of Gen Z consumers believe brands will adhere to privacy laws, this figure drops to 19% among Baby Boomers. For younger consumers, a clean and simple design is critical for comfort when engaging with a brand for the first time. Diana Williams, VP of Product at Intuit Mailchimp, notes, “This research reinforces what marketers are feeling every day: relevance comes from clarity, not volume.” With consumers seeking valuable content, businesses must shift from generic pop-ups to targeted opt-in strategies that resonate with specific audience segments. Automation plays a pivotal role in enhancing the quality of engagement. Brands that regard their contact lists as best-in-class are three times more likely to utilize full automation in their communications. They often employ welcome series and upsell flows more effectively than their less organized counterparts. Moreover, coordinated omnichannel strategies that synchronize messaging across various platforms yield better engagement and conversion rates. Brands that execute these strategies are likely to see higher returns across channels like organic and paid social media. However, many small businesses may find it challenging to harness the data necessary for effective segmentation and personalization. As the report points out, marketers often have access to data but struggle to transform it into actionable insights. Overcoming this friction requires the use of platforms that can aggregate fragmented data and facilitate smarter decision-making. Ultimately, the findings provide actionable insights for small business owners looking to improve their marketing efforts. By understanding consumer preferences, refining opt-in strategies, and leveraging automation, small businesses can build stronger relationships with their customers. The opt-in moment not only sets the tone for future interactions but also serves as a key performance indicator for brand engagement. For more in-depth insights, small business owners can access the full report here. As brands continue to navigate an increasingly complex marketing landscape, the importance of a well-crafted opt-in strategy cannot be overstated. Understanding the nuances of consumer trust, leveraging automation, and focusing on high-intent moments can make all the difference in fostering lasting relationships. Image via Google Gemini This article, "New Study Reveals How Trust Shapes Consumer Engagement at Sign-Up" was first published on Small Business Trends View the full article

-

A new report by Intuit’s Mailchimp highlights the critical importance of the opt-in moment for brands aiming to foster strong relationships with consumers. Titled The Art of the Opt-In: Why List Building is Only the Beginning, the study reveals that building quality email and SMS lists goes far beyond simply assembling contacts; it’s about creating trust, personalizing experiences, and ultimately driving engagement. Matt Cimino, product manager at Intuit Mailchimp, emphasizes, “As tracking and re-targeting become more complex, the opt-in stands out as one of the few moments when a brand can earn a direct relationship – with permission.” The insights from this report offer small business owners a roadmap to navigate the opt-in landscape effectively. One of the report’s major findings indicates a disconnection between what marketers believe consumers are willing to share and the reality of consumer privacy concerns. For instance, while 65% of brands ask for a phone number during sign-up, only 28% of consumers are comfortable providing that information. This gap underscores the need for brands to rethink their approach to data collection, focusing on high-intent actions like browsing and checkout moments to optimize their opt-in strategies. The report showcases that many marketers—nearly all of whom maintain email and SMS lists—struggle with quality. Less than a third consider their lists “very high quality,” and only 8% report opt-in conversion rates exceeding 20%. These disappointing statistics may stem from a lack of sophisticated tools and insights; only 20% of marketers fully automate their email and text campaigns, and just a third are confident in tracking sign-up sources. Trust also appears to be generational. The study found that while 39% of Gen Z consumers believe brands will adhere to privacy laws, this figure drops to 19% among Baby Boomers. For younger consumers, a clean and simple design is critical for comfort when engaging with a brand for the first time. Diana Williams, VP of Product at Intuit Mailchimp, notes, “This research reinforces what marketers are feeling every day: relevance comes from clarity, not volume.” With consumers seeking valuable content, businesses must shift from generic pop-ups to targeted opt-in strategies that resonate with specific audience segments. Automation plays a pivotal role in enhancing the quality of engagement. Brands that regard their contact lists as best-in-class are three times more likely to utilize full automation in their communications. They often employ welcome series and upsell flows more effectively than their less organized counterparts. Moreover, coordinated omnichannel strategies that synchronize messaging across various platforms yield better engagement and conversion rates. Brands that execute these strategies are likely to see higher returns across channels like organic and paid social media. However, many small businesses may find it challenging to harness the data necessary for effective segmentation and personalization. As the report points out, marketers often have access to data but struggle to transform it into actionable insights. Overcoming this friction requires the use of platforms that can aggregate fragmented data and facilitate smarter decision-making. Ultimately, the findings provide actionable insights for small business owners looking to improve their marketing efforts. By understanding consumer preferences, refining opt-in strategies, and leveraging automation, small businesses can build stronger relationships with their customers. The opt-in moment not only sets the tone for future interactions but also serves as a key performance indicator for brand engagement. For more in-depth insights, small business owners can access the full report here. As brands continue to navigate an increasingly complex marketing landscape, the importance of a well-crafted opt-in strategy cannot be overstated. Understanding the nuances of consumer trust, leveraging automation, and focusing on high-intent moments can make all the difference in fostering lasting relationships. Image via Google Gemini This article, "New Study Reveals How Trust Shapes Consumer Engagement at Sign-Up" was first published on Small Business Trends View the full article

-

Help them embrace it to reach their goals. By Aaron Klein and Dan Bolton The Holistic Guide to Wealth Management Go PRO for members-only access to more Rory Henry. View the full article

-

Help them embrace it to reach their goals. By Aaron Klein and Dan Bolton The Holistic Guide to Wealth Management Go PRO for members-only access to more Rory Henry. View the full article

-

Huw Pill pushes back against calls for reductions from more dovish voices on MPCView the full article

-

After 25 years of obsessing over Mars, Elon Musk announced that SpaceX has shifted focus from invading the Red Planet to invading the Moon. He claims he will build a self-sustainable lunar metropolis in less than a decade—a sharp contrast to his proposed Mars colony, which he says would now take at least 20 years. Both timelines are as fictional as Star Trek, but at least now his plan makes sense. It is a jarring plot twist from January 2025, when Musk dismissed the Moon as a “distraction.” Now, he says, the satellite is the “overriding priority” to secure civilization. Musk argues a lunar base is necessary because a “natural or man-made catastrophe” on Earth could cut off the supply lines a Mars colony would need to survive. Musk might actually be making sense this time. As Harvard physicist Avi Loeb points out, Musk is right to pivot. The Moon is closer, making it faster to get to, and it aligns with the geopolitical objectives of the United States (the government pays a lot of SpaceX’s bills). It makes sense financially, opening the opportunity for the return of investment that may come from mining the lunar surface and orbiting asteroids, as well as his absurd plan to put one million AI satellites in orbit (made and launched from the Moon, no less). The financial aspect is the key. Really, it’s the whole end game. By choosing a target that’s more accessible—and lucrative—than Mars, Musk is crafting a realistic illusion for investors and bull analysts. He needs to inflate the immediate financial expectations of SpaceX, so his company can get as much money as possible in its programmed 2026 IPO. Hard limits The unavoidable fact that forced him to pivot from Mars is, above everything, basic physical limitations. “[The Moon] is much more practical to bring people back and forth,” Loeb told NewsNation. Musk described his “self-growing city” on X as a settlement that would be capable of expanding rapidly using local resources. It’s not something that that has ever been demonstrated. Still, Loeb argues that “the moon makes much more sense” before we attempt to leap into the deep void of the solar system. The physics of space travel don’t care about Musk’s marketing tweets. The Moon is simply a more forgiving target. Musk says that SpaceX can launch to the Moon every 10 days, allowing for rapid iteration; whereas Mars missions are shackled to planetary alignments that only occur every 26 months. The commute is also drastically different: a two-day hop versus a six-month deep-space haul exposed to radiation and all sorts of space dangers. As Quentin Parker, a professor of astrophysics at the University of Hong Kong, points out: “If you have some issue or emergency, you’re a few days away from Earth. You’re months away if you’re on Mars.” That’s the difference between a rescue mission and a lot of funerals. Whenever it is ready, Starship’s massive capacity to haul over 110 tons of cargo makes it a powerful workhorse to send everything Musk needs to build his fabled city as fast as possible. Base alpha and lava tubes Musk is calling his proposed self-sustaining lunar city “Moon Base Alpha,” a direct homage to the 1970s British-Italian science fiction television series Space: 1999. In the show, Moonbase Alpha is a high-tech scientific research center located in the lunar crater Plato. Musk city’s hardware is radically different from the series’ shiny sets and spaceships. The workhorse for his plan is the Starship Human Landing System, a modified version of the regular Starship stripped of its heat shield and flight flaps since it will never need to re-enter Earth’s atmosphere. Instead of massive engines at the base, this ship uses smaller hull-mounted thrusters for touchdown to avoid blasting a crater into the landing zone and kicking up lethal dust. Once landed, a massive elevator would lower crews and cargo from the high-altitude cabin. The sheer volume of a Starship offers nearly 35,000 cubic feet of pressurized space—dwarfing the Apollo Lunar Module’s cramped 160 cubic feet—which allows for actual living quarters rather than just survival pods. SpaceX also envisions landing and tipping Starships horizontally and burying them under five meters of regolith to shield crews from cosmic radiation. Powering this buried city requires overcoming the lunar night, which lasts for two weeks of freezing darkness. For that, SpaceX will need nuclear reactors like those designed by Kilopower, 10-kilowatt fission units that can run continuously for a decade—rather than relying solely on solar. The city will still need solar arrays, especially in the initial phase. NASA and SpaceX are developing Vertical Solar Array Technology (VSAT)—32-foot-tall masts designed to capture sunlight that grazes the horizon at the lunar South Pole. To move around, astronauts won’t just be walking; they will live inside pressurized rovers, essentially mobile habitats that allow them to explore for weeks without returning to base. But the ultimate goal is to go underground. Musk’s engineers are exploring another old idea for lunar bases: lava tubes. These massive natural tunnels were formed millions of years ago by ancient lunar volcanic flows. They offer ready-made protection with stable temperatures of around 63 degrees.Inside these subterranean cathedrals, SpaceX can build habitats using regolith-based 3D printing tech, like those imagined by 3D-printing construction companies Luyten and Icon. Giant rovers can also weave fibers from moon dust to construct inflatable module supports inside the lava tubes. However, the chasm between rendering and reality remains vast. SpaceX targets a 2026 orbital refueling test for Starship—a critical prerequisite for any lunar mission—a date that has been pushed repeatedly and doesn’t look like it’s going to happen. Aside from part of its elevator, the company hasn’t delivered most of the hardware for Starship HLS. It’s all on the drawing board, which is why NASA reopened the bids for the lunar lander in 2025 after SpaceX failed to progress on their promised milestones. Icon’s lunar construction system is still in R&D, and the Kilopower nuclear reactors, while promising, are still in the ground-testing phase with deployment unlikely before the 2030s. Musk’s “less than a decade” timeline assumes a flawless convergence of technologies that, right now, exist mostly on paper. Follow the money But we know Musk’s pivot isn’t about practicality. It’s about business and valuation. On February 2, SpaceX merged with Musk’s artificial intelligence venture, xAI, creating a corporate titan valued at $1.25 trillion. Sources indicate SpaceX is preparing for a mid-June 2026 IPO that could target a valuation as high as $1.5 trillion, potentially the largest listing in history. Investors love many fast catalysts, not multi-decade pipe dreams. Musk wants to dominate AI, and he knows he needs raw power so he plans to build orbital data centers to feed this AI obsession, allegedly bypassing the power and cooling constraints of terrestrial facilities. Musk’s narrative is selling the idea that the only way to put one million xAI servers in orbit is to exploit the Moon’s resources. Mine it for silicon and oxygen. Build the factories to make the servers. Build a magnetic cannon system to launch the servers into Earth orbit. The Moon becomes the construction site for the “vertically-integrated innovation engine” he promised during the xAI merger announcement. Musk appears to believe he can build this infrastructure before his life ends. It doesn’t matter that multiple experts think that’s impossible. It doesn’t matter that he’s basically proposing building a potential weapon of mass destruction—a cannon satellite launcher—on the Moon. It doesn’t matter that he wants to put a one-million satellite orbital minefield around Earth. And it doesn’t matter that thermodynamics makes his idea of cooling xAI servers in space extremely hard. Space is not “the cheapest place to put AI in 36 months or less,”as Musk has said. In fact, according to Lluc Palerm, research director for satellite at consulting firm Analysys Mason, Musk’s plan to make money out of space servers has the same magnitude of challenge as a Mars mission. Still, building a lunar city aligns perfectly with NASA’s Artemis program—which recently saw the SLS rocket lift off for the first time in 50 years—and offers immediate revenue potential through government contracts that a distant Mars colony simply cannot match. The Bezos threat Which brings us to the second player in this Moon race: Musk is suddenly battling a competent Jeff Bezos. For years, SpaceX’s factory in Texas stood unrivaled. But Blue Origin has finally started delivering. It’s landing its New Glenn rocket and planning a Blue Moon Mark 1.5 lander that doesn’t require complex orbital refueling. That’s competition to Musk in terms of actual Earth dollars. “Multiple sources have told Ars that Bezos has told his team to go “all in” on lunar exploration,” writes Ars Technica’s space editor Eric Berger. This creates a genuine threat that Blue Origin could put humans on the lunar surface before Starship gets there. Bezos isn’t just playing catch-up either. He is building a parallel industrial machine. Blue Origin has successfully tested Blue Alchemist, a technology that melts lunar regolith to autonomously manufacture solar cells and transmission wire without needing any materials from Earth. The company has also launched Project Oasis, a mission to map lunar water ice and helium-3 using low-orbit satellites equipped with neutron spectrometers. To cut costs, Blue Origin is developing Project Jarvis, a reusable stainless-steel upper stage for the New Glenn rocket, mirroring the reusability of Starship. Bezos’s vision is not to build underground cities on the Moon but to build O’Neill colonies, massive orbiting habitats. He sees the Moon not as a colony, but as the mine that will build them (again, a crazy long-term plan). So Musk’s pivot appears to be a calculated move to seize the commercial opportunity of the Moon before his rival does. Red Moon rises While Musk tweets about future cities and Bezos powers up, the most dangerous enemy for the United States’ space hegemony is on a fast collision course. China is the last part of Musk’s wild turn. The Asian giant is executing a concrete, century-long roadmap. On January 29, the China Aerospace Science and Technology Corporation (CASC) officially launched the Tiangong Kaiwu program, a massive national plan named after a 1637 Ming explorer’s encyclopedia to extend Chinese industrial dominance across the solar system. The plan treats space not as a scientific frontier, but as an economic zone. According to academic Wang Wei, who architected the proposal, the goal is to secure strategic minerals from near-Earth objects to fuel Earth’s sustainable development. According to the regime’s official China Space Daily, “among the 1.3 million asteroids in our solar system… about 700 are relatively close to Earth and estimated to be worth over $100 trillion U.S. dollars each. Taking technical feasibility and cost-effectiveness into consideration, 122 of them are economically suitable for mining and use.” This is a four-stage industrial conquest. CASC’s roadmap dictates that by 2035, China will establish a lunar resource development system and begin mining near-Earth asteroids. By 2050, operations will expand to Mars and the main asteroid belt. The timeline extends to 2075 for the exploitation of Jupiter and Saturn, aiming for a fully operational solar-system-wide resource network by 2100. Unlike Musk’s private ventures, this is state policy: verify feasibility by 2030, build the supply chain by 2035, and dominate the market by mid-century. China has already poured concrete for this launchpad. They have successfully deployed the Queqiao satellite constellation—including the recently launched Queqiao-2—creating the world’s first permanent communication relay for the lunar far side. This network is the backbone for future autonomous mining operations. Furthermore, the plan includes a gigawatt-class space-based digital infrastructure that integrates cloud computing and space debris monitoring, essentially creating a space traffic control system that China intends to manage. While Musk is pivoting his company to catch up, Beijing’s machine has been methodically laying the tracks for decades. And it has a plan to catch up and surpass the U.S. While Musk may want us to believe that only he has the key to our future and that his new Moon plan is now what we all need, there are clearly other people on the planet who think otherwise. For now, what we really have is yet another erratic plot twist, a radical course change masquerading as “The New Way to Save Humanity” while he makes lots of money in the process. View the full article

-

Of course we have a recommendation. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-

Of course we have a recommendation. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-