All Activity

- Past hour

-

Google is doubling down on Data Strength as conversion signals become more critical to bidding, performance, and how campaigns are optimized. The post Google’s Push For Data Strength Is Really A Push For Better Bidding appeared first on Search Engine Journal. View the full article

- Today

-

For those of us not born tall and strong, using a shared electric bike can sometimes be cumbersome—they’re often big, heavy, and hard to maneuver. Bike-share giant Lime has taken note, releasing a new generation of bikes tailored for riders who could benefit from more accessible design. One of the first dockless micromobility companies, Lime launched in 2017, eventually filling the streets of major cities across the U.S., Europe, Australia, and the Middle East with its bright-green two-wheelers. Now the company has introduced an alternative model to its standard Gen4, designed to reach riders—particularly women and older adults—who may have found its original model challenging or intimidating. “The new vehicle builds upon the strong foundation of what is already working well,” Jason Parrish, Lime’s senior director of product management, tells Fast Company. Lime piloted its new design in July 2024 in Atlanta, Seattle, and Zurich, with an official release in April last year. The model, called a “LimeBike,” is not meant to replace the Gen4, but rather serve as a complement to the company’s bike-share services, offering an alternative for riders. LimeBikes are currently in circulation domestically in Atlanta, Seattle, and Nashville, and globally in Munich, Paris, Berlin, and other cities. A rider-friendly redesign The LimeBike model came about based on feedback from riders and city officials from around the world who said they wanted bike sharing to feel more approachable and accessible to a wider range of riders, especially those who are shorter in stature or have more restricted range of motion. Compared to the original model, the LimeBike weighs less, has a more compact frame, a lower step-through, and smaller, 20-inch tires. The designers also moved the bike’s battery under the seat to shift its center of gravity, and introduced an ergonomic seat clamp to ease height adjustments. These details make the bike more comfortable to get on and off of, steer, and ride. “We wanted to keep the great ergonomic ride feel that our riders love about the Gen4 bike, but do it in a new way that makes the vehicle feel more approachable and accessible,” Parrish says. “The result is that while the frame changed, the rider geometry of the bike [distance between seat, pedals, and handlebars] was maintained from the Gen4.” The redesign also addresses safety concerns. As the blog London Centric reported, a number of Lime riders in the U.K. have suffered broken legs, which some attribute to the Gen4 e-bike’s heavy design. Some riders are pursuing legal action against the company. The redesign features details that will improve trips for all riders, like a new phone holder, wider front basket, and advanced location-recognition accuracy so they don’t accidentally leave the bike in a no-parking zone. “The updates focus on making the LimeBike more approachable, intuitive. and practical for everyday use,” Parrish says. Longer-lasting bikes The redesign doesn’t solve only rider pain points. It also extends each bike’s lifespan by featuring modular elements that make replacing parts easier and quicker. Additionally, the bike is made with some of the same parts as the LimeGlider, the company’s e-scooter, making inventory management more efficient. “By building the two vehicles together, we were able to create a unified product experience for riders, simplify spare parts management and maintenance, and release two vehicles at once to drive innovation in our fleet,” Parrish says. As the fleet and offerings continue to expand, so do options for sustainable urban travel. According to UCLA Transportation, swapping a car ride for a bike ride can lower an individual’s emissions by 67%. Accessible scooter and bike designs are providing a greener option for riders regardless of their body type. View the full article

-

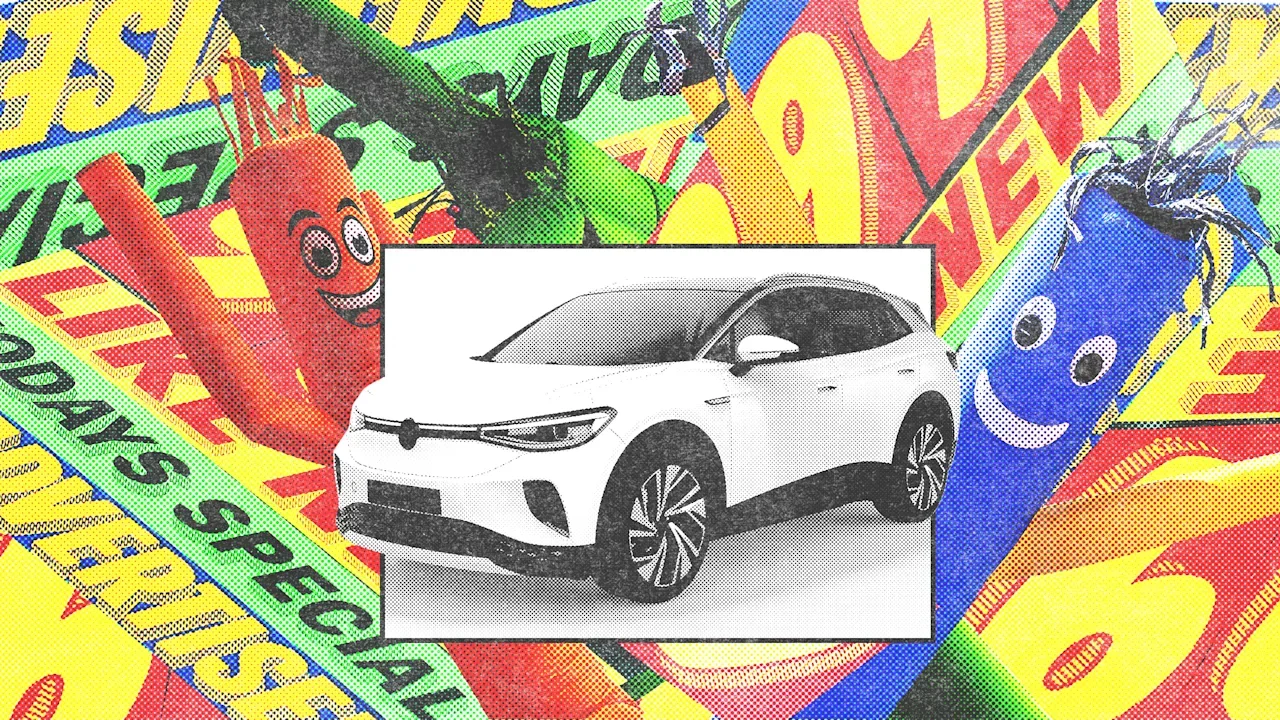

If you’re in the market for a car, you might be one of a growing number of people considering a used EV. In the past month alone, Cars.com says searches for used EVs jumped 25.5%, pointing to how quickly interest is shifting. Gas prices likely won’t drop much anytime soon, even if the Strait of Hormuz can stay open. And with hundreds of thousands of used EVs coming off lease this year, consumers have affordable options, even though the federal tax credit went away last year. You get more for your money than with used gas cars: for the same price as a five-year-old Toyota Camry or RAV4, you can get a newer Tesla Model 3 or Volkswagen ID4 with tens of thousands of fewer miles, according to Recurrent, a company that tracks EV data. Here’s what to know if you’re shopping for a used EV. Battery life is better than you think First, you don’t need to worry much about the battery. “EV batteries are lasting a lot longer than most people expected—even people that study electric car batteries every day,” says Andy Garberson, head of growth at research at Recurrent. The company tracks data from 30,000 EV owners across the U.S., and says that among cars that were made in 2022 or later, only 0.3% have needed battery replacements because of degradation or failure. If older EV with first-gen batteries are included, the number is still low, with 4% needing replacement. Performance is surprisingly good over time. Take the example of a 2023 Nissan Ariya, an EV that Recurrent recommends. Three years after it came out, its average real-life range is 226 miles on a full battery charge, a stat that’s better than its official EPA range. In another three years, it’s likely to drop only slightly to 220 miles on a charge. Range for any EV varies depending on conditions like cold weather (the Ariya performs well in the winter, too, keeping 83% of its range). You can access Recurrent’s data through dealerships or listings on Edmunds and Cars.com to see stats for any used model throughout the year in your own climate, along with estimates of how much you can save on fuel and maintenance. EV batteries aren’t the battery in a phone, which can see steep degradation. In an EV, the data shows that there’s actually a little more degradation in the beginning, but it slows down. “We’ve all had that phone that a few years old and the pace of degradation actually accelerates with time, and that’s just not the case with EVs that have sophisticated battery management systems and liquid cooling and just a lot of tech that’s there to preserve it,” Garberson says. When buying an EV, you can ask the dealership for a battery health report, or take a car from a private seller to repair shop for a test. After checking the expected range based on the car’s age, you can also see how it performs on a test drive. Before a test drive, you can ask the dealership to fully charge the battery overnight. If a battery does degrade significantly after you buy it, the manufacturer should replace it. Nearly all EVs sold in the U.S. include long battery warranties, typically lasting 8 years or 100,000 miles. (EPA performance rules require that EV batteries last at least that long.) If a battery drops to less than 70% of its capacity, the warranty should cover a replacement. Buy the newest used EV you can afford Newer models are a better choice than older EVs because EV technology has been improving so rapidly. Early EVs had different battery chemistry, but lithium ion phosphate (LFP) batteries became widespread in the 2020s—making batteries cheaper, safer, better at handling frequent charging, and longer lasting. The median range for an EV in 2023 was 270 miles on a charge; compare that to a 2017 Nissan Leaf, which started with around 84 miles of range. It makes sense to buy the newest used EV you can afford. Like all cars, newer models also have better tech in general, including safety features and more options for autonomous driving. The 2023 Nissan Ariya, for example, comes with ProPILOT Assist 2.0, semi-autonomous technology that can assist with lane changes or passing slower drivers. The EV was expensive when new, and didn’t sell particularly well for that reason. But used models now sell for only around $25,000. “The used price made that car very appealing, because you’re getting a lot of car for the money,” says Garberson. With a newer EV, you’ll also have more time left on the battery warranty if you need it. But buyers who choose older EVs do also have the option to pay for third party warranties through companies like Xcelerate Auto. Consider the EV’s history As with any used car, you’ll want to do a prepurchase inspection and also find out as much as you can about its past. An EV that was a rental car—like the thousands of Teslas dumped by Hertz—or a ridesharing or fleet vehicle, obviously would have seen more use. Still, that may be more of a negotiating tool than a reason not to buy it. Ridesharing EVs can hold up surprisingly well, like a 2022 Ford Mustang Mach-E that still had 92% battery life after 250,000 miles on the road. In theory, if the previous owner regularly used fast charging, that could degrade the battery faster, though Garberson says that real-life data hasn’t borne that out. “When we sit down with all of our PhDs that studied this stuff in school, they understand that at an academic level that fast charging degrades a battery faster,” he says. “That’s something that they know and can prove out in a lab environment. But when we look across all of the cars connected to Recurrent—and we even can segment by those that we know are fleet vehicles that are only fast charged—we can’t see that in the data.” Buyers should also consider potential perks that carry over with the vehicle. Some used Teslas, for example, come with free unlimited charging that the next owner can use. Some software subscriptions also transfer. In general, Garberson says, used EVs can offer buyers significant value, including cars that were expensive initially. “People are amazed that they can drive off a lot with a BMW SUV that has 350 miles of range for the price of a RAV4,” he says. “We’re at an interesting moment in time. This is going to be kind of an exciting year with some of the affordable new models that are coming out. But there are also going to be a lot of people trading in, and that’s going to put a lot of really nice used EVs on the market.” View the full article

-

Google's Mueller answers whether links pass negative signals and says unhelpful links may be ignored. The post Google Answers If Outbound Links Pass “Poor Signals” appeared first on Search Engine Journal. View the full article

-

Ever find yourself behind the wheel watching all the other cars go by and think to yourself, “Man, I’m a much better driver than all these clowns on the road?” It’s a funny thing about this question. Pretty much everyone reading this is likely to say “yes.” It seems we all think we’re better drivers than the next guy. In a landmark 1981 study, psychologist Ola Svenson asked people in the U.S. and Sweden to rate their driving skills compared to the average person. The results? Around 80–93% rated themselves “above” average—statistically impossible—with an eye-popping 93% in the American sample doing so. Psychologists call this “illusory superiority,” the human tendency to think we are better than average at pretty much everything. We think we are smarter, kinder, more generous and even funnier than other people. And it turns out, this unbecoming bias sneaks right into how positively we think we show up for the people we lead. Research shows that leaders who consistently act as a genuine positive force build deeper trust, stronger commitment, greater resilience, and higher team performance—yet most of us overestimate how effectively we do it. Which leads to a question worth pondering: Would you consider yourself above average as a positive force for the people you lead? If your answer was “yes” (and let’s be real—most leaders consider themselves exactly that), the research has a gentle but eye-opening reality check coming. The Ratio That Separates Thriving Teams from Struggling Ones Renowned psychologist John Gottman, who spent decades studying successful marriages at the University of Washington, discovered something remarkable: thriving couples maintain roughly five positive interactions for every negative one. He called this the “magic ratio.” In short, consistent positivity (appreciation, encouragement, humor, support) far outweighs criticism or conflict in building trust, resilience, and lasting connection. For example, a couple might have a tense disagreement (even a heated argument), but if they quickly follow it with affirming words like “I value your perspective,” a warm touch, or shared laughter, the relationship remains strong, healthy and enduring. And, as Gottman later found, the exact same dynamic plays out in leadership and teams: When leaders foster far more positive interactions than negative ones—even amid tough debates or feedback—the group builds trust, stays resilient, and performs at a higher level. But here’s the catch that makes this especially challenging for leaders: the math is stacked against us from the start. Researcher Roy Baumeister’s work on negativity bias shows that negative experiences and feedback land four times harder on humans than positive ones of similar magnitude. If you wonder why, it’s because our brains were wired this way in our evolutionary past—to ensure threats got priority attention and helped our species survive. As leaders, this means every difficult conversation, performance critique, or unpopular decision lands with amplified force—easily overwhelming praise or encouragement unless we intentionally counterbalance it. And this imbalance explains why maintaining a high positivity ratio doesn’t happen by default. Instead, it requires deliberate, daily leadership practice rooted in genuine intention and sustained effort. And what’s the reward for this vigilance? Positive psychologist Barbara Fredrickson’s research shows that people who experience consistent positivity become more creative, resilient, collaborative, and better at solving complex problems. At the same time, negative workplaces do the opposite—they narrow focus, heighten defensiveness, and limit innovative thinking. In other words, positivity from leaders doesn’t just make people feel good—it expands what their brains can do, leading to greater creativity, collaboration, and performance. Neuroscience sharpens this point: chronic exposure to negative leadership—criticism, unpredictability, fear—elevates cortisol levels in measurable ways. Sustained high cortisol undermines focus and clear thinking. In other words, leaders who lean heavily negative (sadly, there are many) don’t just demoralize people—they biologically constrain what their teams can accomplish. These findings are part of the research foundation behind my book, The Power of Employee Well-Being. One of the central conclusions is simple but powerful: leaders shape the emotional climate their teams experience every day—and that climate (positive or negative) quietly determines how well people think, collaborate, and perform. What Being a Positive Force Actually Looks Like Contrary to what may be commonly assumed, being a positive force has nothing to do with being relentlessly cheerful, avoiding hard conversations or sugarcoating reality. The truth is leaders like this are mythical—and wouldn’t survive long in business were they real. Instead, leaning into positivity means being solutions-oriented rather than problem- or fault-obsessed. It means being genuinely curious about your people—truly interested in what matters to them—and consistently showing it. This shows up through encouragement, kindness, and the psychological and emotional safety that lets employees bring problems to you early, before they become crises. It also means actively looking for what’s working and praising it—rejecting the outdated belief that too much praise spoils motivation—more often than focusing on what isn’t. The behaviors that sustain the 5:1 ratio are deceptively simple. Showing genuine interest in your people. Expressing appreciation specifically and sincerely. Listening attentively rather than waiting to respond. Beginning team meetings by celebrating wins before tackling challenges. Asking “how are you—and how are you really?” and meaning it. Gottman found these same behaviors to be the glue that sustains marriages over decades. They work the same way between leaders and the people they lead—and over time they determine whether teams merely function or truly thrive. The Blind Spot You Need to Close Here is the uncomfortable truth that brings us back to where we started. In study after study, leaders rate themselves significantly more positive, approachable, and encouraging than their direct reports rate them. And, sadly, that gap is wide. Illusory superiority convinces most of us that other leaders need to improve their positivity—not themselves—a belief that keeps many from even trying. To that I say, your people already know if you are a positive influence in their lives. The only question is whether you do. So, go find out. Ask your team—genuinely and not performatively—how positive a force you are for them. Ask your most trusted colleagues, your peers and even your boss. If the news isn’t ideal, listen without defending. Then go use the feedback to change your presence and influence. Being a positive force is not a personality trait or a one-time fix—it is a daily leadership discipline that shapes the emotional climate your team breathes every day. Choose it intentionally, and you don’t just improve performance; you help people become more of who they’re capable of being and elevate their well-being. As I often say (and one of my core mantras): “The most powerful thing a leader can do is make people feel better about themselves when they leave your presence than when they arrived.” View the full article

-

For decades, the millions of American women who dye their hair had two options: They could spend three hours and upwards of $300 in a salon or grab a $10 box off the drugstore shelf, squint at the ingredient list, and hope for the best. There was no middle ground. Amy Errett thought that was absurd. “There was no prestige product that a woman could buy for at-home use,” the founder and CEO of hair color startup Madison Reed tells me. “Just because you color at home does not mean you can’t afford good color. That was, in my opinion, a very elitist viewpoint.” Errett established Madison Reed in 2013, right as the direct-to-consumer wave was cresting. But while brands like Warby Parker and Dollar Shave Club were mostly rethinking distribution—taking existing product categories online and cutting out the middleman—Errett wanted to do something more fundamental. She wanted to reformulate hair color from the ground up, rethinking how it reaches consumers. The result is a company that is profitable and has raised approximately $250 million in venture capital. Across the U.S. Madison Reed operates 98 Hair Color Bars—which exclusively offer hair coloring services—and sells through Ulta, Amazon, and its own website. The brand is now poised to take market share from competitors that have been around decades longer, like L’Oreal, Schwarzkopf, and Wella. “A lot of the DTC models were picking off a very narrow aspect of something and trying to build a commerce brand,” says Jon Callaghan, cofounder and managing partner of True Ventures, which has backed Madison Reed since 2013, along with Norwest Venture Partners, Comcast Ventures, and Jay-Z’s Marcy Ventures. “Amy’s tackling something substantially larger—a fundamental activity in beauty and wellness that women do every four to six weeks.” Callaghan describes Madison Reed as a classic disruption story. “The industry was dominated by large incumbents, very low innovation, poor-quality product,” he says. “Amy sort of flipped the script on every aspect of that.” Anthropological research Madison Reed’s origin story begins with a woman and a bathroom. Errett, a serial entrepreneur and former venture capitalist, recorded about 50 women at home doing their hair with drugstore box dye and observed them. The experience left a lot to be desired. The instructions were unreadable. The smell was off-putting. The shade ranges—often only eight or so colors—bore no resemblance to the complexity of actual human hair. “Dark hair has a multitude of colors,” Errett says. Her first breakthrough was upending the product itself. Errett set out to reformulate home hair color without ammonia and other harsh chemicals that were standard across the category. Madison Reed’s boxes, which retail for $35, contain hair dye made in Italy using a production process the company controls end-to-end. Today, the brand offers roughly 90 shades of color, 55 of which are available to consumers as permanent color. The second breakthrough was matching the right color to the customer. Half of American women color their hair at home, Errett points out, but the fundamental challenge of the at-home market is that you can’t see the customer. “There’s a lot of science in hair color,” she says. “I have to know what her natural color is, how gray is she, the texture of her hair.” From the beginning, Madison Reed developed AI to bridge that gap. Customers answer an 18-question quiz, then the system recommends two shades most likely to suit them. The process is working. The company now has roughly 17 million profiles, which gather data points about the color and texture of consumers’ hair. Customer retention rates, Errett says, run at 70% and above, which matters enormously in a business predicated entirely on repeat usage. “If I don’t get you to come back, this doesn’t work,” she says. Errett had always suspected that many women dyed their hair in salons not out of preference, but because there wasn’t a high-quality at-home hair dye they trusted. But when COVID-19 hit and the world shut down, many women scrambled for an alternative. Madison Reed offered a solution. The brand touted its high-quality, less-toxic ingredients. And the boxes provided everything needed to do the job at home, from plastic gloves to wipes. Madison Reed received an influx of new customers during the pandemic. For many, it was a revelation that they could have an enjoyable experience doing their hair at home—at a fraction of the cost and time of a salon visit. Many never went back. A multichannel business The DIY customer is only part of the market. Many women prefer to have someone else dye their hair, and Errett wanted to make sure Madison Reed was serving them, too. Shortly after launching the at-home color part of the business, Errett debuted a new concept called a Hair Color Bar. Optimized for speed, these salons specialize in color only (no haircuts), so customers are in and out as quickly as possible. Most women don’t even opt for a blowout; they dry their hair when they get home or use hair dryers provided in the salon. Before COVID, there were just eight of these locations. But after the pandemic, Errett invested in growing the network of storefronts exponentially. “There was a pent-up demand to get out of your house and go into a store,” she says. What makes Madison Reed unusual is what Errett calls the “blurring of lines” between channels, which gives women the flexibility to dye their hair in many different ways, depending on their lifestyle and schedule, all while achieving consistent results. The company assumes that women may choose to pop into a salon sometimes, and use an at-home box at other times. Every color applied in a Hair Color Bar is logged in the company’s backend system and linked to an email address. A customer can walk into any of the brand’s locations and get the exact color that was applied at a different bar previously. She can go online and order that same box delivered to her door. “She owns that color,” Errett says. “It’s hers. She can do it wherever she wants, whenever she wants.” The company also sells products through big-box retailers, which is another way to offer convenience for customers—and an opportunity for the brand to continually introduce itself to new consumers. While the conventional wisdom is that a brand’s sales may cannibalize those of third-party retail partners, Errett has found that the opposite is true. In markets where Madison Reed has more than two locations, nearby retail sales at partners like Ulta run 20% to 30% higher out of brand recognition. “You walk by the [Madison Reed] store at the Oakbrook Mall in Chicago, you see it’s full, then you pop into Ulta eight stores down and you see Madison Reed on the shelf,” Errett says, noting the effect is, “‘Oh, I recognize that. That must be good.’” The Hair Color Bars function, in Errett’s framing, as permanent billboards: 98 stores, 1.3 million services expected this year, all generating awareness that no marketing budget can replicate. Running three businesses simultaneously—direct-to-consumer subscriptions, nearly 100 physical service locations, and a wholesale presence at major retailers—is, Errett acknowledges, operationally brutal. “You’re running three completely different businesses,” she says. But the hero of all three is the same product, which is what makes the model defensible rather than just complicated. Thriving in the trade-down economy The current economic moment has turned out to be well-suited to what Madison Reed sells. Consumer confidence is shaky. People feel the pinch of inflation. Many consumers, even those who are affluent, are eager to stretch their budget. A $300 salon appointment can feel hard to justify when a $35 box—or a $45 Hair Color Bar visit—delivers comparable results. “People want quality, but they want value,” Errett says. “They’re not trading going out to dinner all the time to McDonald’s. They may not be going to the five-star restaurant, but they still want a great meal.” (She notes that the household income of Madison Reed’s Hair Color Bar customers averages $150,000 and above; in some markets, it’s closer to $175,000.) It’s a profile that maps closely to what retail analysts have watched unfold across other categories: Walmart’s stunning turnaround among middle- and upper-middle-class shoppers, Ulta’s resilience, the durability of TJ Maxx. The brands winning right now aren’t the ones promising pure luxury or pure value; they’re the ones that have found the gap between the two. Madison Reed has real estate studies suggesting it could support 700 to 800 Hair Color Bars in the U.S. alone. It’s currently only in 15 markets, so it has a lot of room for growth. But Errett says she’s created a business where 72% of revenue is recurring, through a combination of membership plans to the Color Bars and subscriptions to the at-home product. Errett likes to think of her company as generating “SaaS-like revenue,” even though it’s a consumer business. When Errett describes the nature of the business to me—heavy physical assets, low obsolescence, a service too intimate to be automated—she also articulates something broader about what it takes to build a durable consumer brand right now: You need a product that solves a problem. You need to meet customers wherever they happen to be. And you need a reason for them to come back. “Hair is confidence,” Errett says. “It is a relatively inexpensive way to feel good about yourself.” In a moment when people are squirrelly about their dollars, that’s a powerful thing to be selling. View the full article

-

Jumbo loans demand more scrutiny and documentation, but automation is streamlining the process — and lenders who master the product stand to gain in a moderately bullish market. View the full article

-

Industry group warns EU that reserves are running lowView the full article

-

With most of New York City surrounded by water, climate change poses a grave threat to its infrastructure, as devastating storm surges and coastal flooding have shown. Inland blocks are in danger, too. Researchers at the New York Botanical Garden have created a new interactive map of the city showing the areas most at risk of flooding. They’re calling them “Blue Zones,” places where water is, used to be, or will be due to climate change. More than one-fifth of the city is in a Blue Zone, according to a paper published in the Annals of the New York Academy of Sciences. “Everybody was startled, including us,” Eric Sanderson, vice president of urban conservation at the New York Botanical Garden and an author of the paper, told The City. nybg.org The hope is that this information will help city officials, planners, and residents better prepare for the effects of climate change. While resiliency infrastructure has hardened the coastline, some of the most disruptive and deadly floods have happened in inland areas where aging infrastructure isn’t able to handle heavy rainfall. To identify the Blue Zones, researchers studied more than 500 years’ worth of flood data and integrated intel from 311 service calls and flood maps from the New York City Department of Environmental Protection and the Federal Emergency Management Agency. Critically, they also examined maps of the city’s natural hydrology. Even though urbanization paved over ponds, streams, and salt marshes, these geographic elements continue to influence flooding today. nybg.org “Understanding the historical ecology—particularly the geographic distribution of streams and wetlands prior to the construction of the city—can help reframe the way we see the current urban landscape, promote ideas about how we adapt to current realities, and prepare for future contingencies,” the researchers wrote in their paper. Some areas identified as Blue Zones may seem surprising, especially those that are far away from visible bodies of water. “It shows how large scale this is and it lets you look at the city as a landscape,” Lucinda Royte, manager of urban conservation, data tools, and outreach at the New York Botanical Garden and coauthor of the paper, told The City. “We currently view the city through its political boundaries. We care about neighborhoods and zip codes, but water doesn’t care about those boundaries.” View the full article

-

A Chart of Accounts setup is crucial for any business, as it organizes all financial accounts in a structured manner. By categorizing accounts into assets, liabilities, equity, revenues, and expenses, you create a framework that allows for efficient tracking of transactions. Each category is assigned specific numerical codes, which aids in accurate reporting and analysis. Comprehending how to properly establish and maintain your Chart of Accounts can greatly impact your financial management practices. What are the key components you should consider? Key Takeaways A Chart of Accounts (COA) is a systematic list of financial account titles organized into categories: assets, liabilities, equity, revenue, and expenses. Each account in the COA is assigned a unique numerical code for easy identification and retrieval, facilitating effective transaction recording. The structure includes main categories with sub-accounts for detailed tracking tailored to specific business needs and financial reporting. Regular updates and reviews of the COA ensure it remains relevant, effective, and aligned with evolving business requirements and compliance standards. Accounting software can simplify COA setup, offering templates and tools for organization, automation, and collaboration in real-time. Understanding Chart of Accounts The chart of accounts (COA) serves as the backbone of an organization’s financial reporting system, providing a structured framework for categorizing all financial transactions. Fundamentally, the chart of accounts definition refers to a systematic list of all financial account titles used in your general ledger. This list is categorized into five primary sections: assets, liabilities, equity, revenues, and expenses. Each account in the COA is assigned a unique numerical code, often following a structured numbering system, which simplifies classification and retrieval. This structure not only improves clarity in financial reporting but also supports budgeting and forecasting. By using a well-structured COA customized to your organization’s specific needs, you can guarantee effective transaction recording and gain detailed insights into your financial performance over various periods. In the end, a well-organized COA is vital for maintaining accurate records and complying with accounting standards. Key Components of a Chart of Accounts Comprehending the structure of a chart of accounts is critical for effective financial management. A typical chart of accounts setup includes five main account categories: Assets, Liabilities, Equity, Revenue, and Expenses. Each account is assigned a unique numerical code, often following a specific chart of accounts format—for example, 100-199 for assets and 200-299 for liabilities. This coding system facilitates easy identification and retrieval of accounts. Additionally, you can create sub-accounts under main categories to provide more detail and organization, allowing you to track specific transactions by business function or division. During the setup process, it’s crucial to take into account your business’s operational needs, ensuring the chart accommodates future growth and financial reporting changes. Regular reviews and updates to the chart are critical, as they maintain its relevance and effectiveness in accurately reflecting your company’s financial activities. Importance of a Well-Structured COA A well-structured chart of accounts (COA) improves financial clarity by organizing transactions into distinct categories, which makes it easier for you to track your financial performance. This organization supports accurate reporting, ensuring compliance with accounting standards and providing stakeholders with reliable insights into the company’s health. Furthermore, a properly set up COA facilitates efficient analysis, allowing you to make informed decisions and improve operational efficiency. Enhances Financial Clarity When you implement a well-structured Chart of Accounts (COA), it greatly improves financial clarity for your business. A clear COA systematically categorizes financial transactions, making it easier to analyze data. Here are four key benefits: Organized Structure: By grouping accounts into assets, liabilities, equity, revenue, and expenses, you create a thorough framework for financial analysis. Performance Tracking: A clear COA supports budgeting and forecasting, allowing you to identify cost control areas. Quick Identification: A numeric coding system boosts the retrieval of financial information, streamlining reporting processes. Ongoing Relevance: Regular updates to the COA guarantee it remains aligned with your operations, preventing confusion in financial reporting. Supports Accurate Reporting Accurate reporting is vital for any business, and a well-structured Chart of Accounts (COA) plays an important role in achieving this goal. A well-organized chart of accounts list categorizes financial transactions into specific accounts, enhancing clarity in reporting. By systematically classifying assets, liabilities, equity, revenues, and expenses, the COA allows for detailed financial analysis, which is critical for informed decision-making. Furthermore, a properly configured COA supports compliance with accounting standards, guaranteeing consistency across reporting periods. It likewise aids in budgeting and forecasting, helping you pinpoint areas for cost control and operational improvements. Regular reviews and updates confirm the COA remains aligned with your evolving business needs, thereby maintaining the accuracy and relevance of your financial reports. Facilitates Efficient Analysis Even though you might think of a Chart of Accounts (COA) as just a list of account names, its role in facilitating efficient financial analysis is far more significant. A well-structured COA improves your comprehension of business performance by: Categorizing transactions for clear visibility into revenue, expenses, and assets. Enabling accurate budget forecasting and variance analysis to identify trends. Streamlining reporting through standardized account codes for quick access to financial info. Supporting compliance with accounting regulations, reducing misstatement risks. Categories Within the Chart of Accounts Grasping the categories within the chart of accounts (COA) is essential for effective financial management, as they provide a structured way to organize a business’s financial data. The COA consists of five primary categories: Assets, Liabilities, Equity, Revenue, and Expenses. Assets represent resources like cash and inventory, classified as current or non-current based on liquidity. Liabilities include obligations to external parties, such as loans and accounts payable, categorized into current and long-term liabilities. Equity reflects the owner’s interest in the business, including common stock and retained earnings. Revenue accounts track income from business operations, whereas chart of accounts expense categories record costs incurred to generate that revenue. Comprehending these categories helps you assess financial performance and make informed decisions, ensuring your business remains financially healthy and organized. Setting Up Your Chart of Accounts Setting up your chart of accounts starts with establishing clear account naming conventions that reflect the nature of each account. You’ll need a numerical coding system, typically five digits, to categorize accounts effectively, ensuring each code indicates its primary category. Organizing your accounts into main categories like Assets and Liabilities, along with thoughtful subcategories, will improve your financial tracking and reporting. Account Naming Conventions When you’re establishing your chart of accounts, having clear and consistent account naming conventions is crucial for effective financial management. Prioritizing clarity and simplicity helps everyone understand the purpose of each account, especially those without accounting backgrounds. Here are some key points to take into account: Use prefixes or common abbreviations (e.g., “Rev” for revenue, “Exp” for expenses) to improve organization. Maintain consistency in naming across the chart of accounts; similar accounts should follow the same structure. Avoid overly complex or lengthy names; concise, descriptive names maintain clarity. Periodically review and update account names to reflect changes in business operations or industry standards. Implementing these strategies will streamline your chart of accounts numbering and enhance financial reporting. Numerical Coding System A well-structured numerical coding system is fundamental for organizing your chart of accounts effectively. This system typically assigns a range of numbers to categorize accounts, with assets coded from 100-199, liabilities from 200-299, equity from 300-399, revenues from 400-499, and expenses from 500-599. Each account receives a unique identifier, facilitating easy organization and retrieval of financial data. The first digit indicates the main category, whereas subsequent digits can represent subcategories or specific accounts, thereby creating a hierarchical structure. Gaps between account numbers are often left intentionally for future additions. When setting up your chart of accounts, verify the coding aligns with your company’s operations and reporting needs, aiding both internal management and external compliance. Organizing Account Categories Organizing account categories is crucial for an efficient chart of accounts, as it improves clarity and structure in financial reporting. To effectively set up a chart of accounts for a business firm, consider these key categories: Assets: Items owned by the business. Liabilities: Obligations owed to others. Equity: Owner’s interest in the business. Revenue and Expenses: Income generated and costs incurred. Assign unique numerical codes to each account, starting with a digit representing its category. Create sub-accounts for detailed tracking, like operational expenses for salaries, rent, and utilities. Tailor the chart to your firm’s specific needs and review it regularly to make sure it remains relevant and effective for accurate financial analysis. Common Challenges in COA Management Managing a chart of accounts (COA) presents several common challenges that can considerably impact financial accuracy and reporting. One major issue is overcomplication, which can lead to data entry errors and hinder staff from accurately recording transactions. Furthermore, a lack of standardization in account naming and structure can create reconciliation problems, resulting in discrepancies that affect financial analysis. Duplicate categories further complicate your ability to compare financial data effectively, making it tough to assess business performance. Misalignment of the chart of accounts with your financial reports can lead to compliance issues, as inaccurate classifications may violate accounting standards or tax regulations. Regular maintenance is crucial to avoid clutter and inconsistencies, ensuring your chart of accounts accurately reflects the current state of the business and supports necessary financial reporting needs. Addressing these challenges proactively can help streamline your financial processes and improve overall accuracy. Best Practices for Maintaining a COA To maintain an effective chart of accounts (COA), you should regularly update it, ideally at least once a year, to guarantee it aligns with your current business operations. Simplifying account structures by using standardized naming conventions can improve consistency and make navigation easier for users. Regular Updates Required Regular updates to your chart of accounts (COA) are crucial for accurately reflecting the financial status of your organization, especially as business operations evolve. To maintain a relevant and effective table of accounts, consider these best practices: Perform periodic reviews—ideally quarterly or annually—to assess the COA’s effectiveness. Maintain consistency in account naming conventions and structures to improve clarity in financial reporting. Incorporate feedback from team members and stakeholders during reviews to identify potential improvements or new account needs. Utilize accounting software to automate updates, ensuring that changes are efficiently implemented and the COA remains organized. Simplify Account Structures When simplifying account structures, it’s essential to create account names that are clear and concise, as this helps minimize confusion during data entry and analysis. Establish a logical numbering system for your standard chart of accounts, categorizing accounts by type—like using 1 for assets and 2 for liabilities. This approach allows for future additions without disrupting the existing structure. Regularly review your chart of accounts to eliminate obsolete accounts and consolidate similar ones, maintaining relevance. Implementing sub-accounts can help categorize detailed transactions without complicating main categories. Furthermore, utilizing accounting software streamlines management, offering automation, real-time updates, and improved insights into financial performance, making your system more efficient and organized. Examples of Chart of Accounts Comprehending the examples of a chart of accounts is essential for effective financial management, as it provides a structured framework for organizing a business’s financial information. A well-structured chart includes various categories, each with specific examples. Here are some common examples of chart of accounts: Asset Accounts: Cash (101) Accounts Receivable (102) Inventory (103) Liability Accounts: Accounts Payable (201) Short-Term Loans (202) Revenue Accounts: Sales Revenue (401) Service Income (402) Expense Accounts: Rent Expense (501) Salaries Expense (502) Advertising Expense (503) These examples of chart of accounts help you categorize and track your business’s financial activities, ensuring accurate reporting and analysis. Impact of COA on Financial Reporting The impact of a well-structured Chart of Accounts (COA) on financial reporting is significant, as it lays the groundwork for accurate and clear financial statements. A properly organized accounting chart of accounts categorizes transactions into distinct accounts, minimizing misclassifications that could distort your financial data. This structure not just aids in compliance with accounting standards but furthermore guarantees consistent recording of all transactions, making it simpler to generate compliant reports for stakeholders. Tools and Resources for Effective COA Management A well-organized Chart of Accounts (COA) is only as effective as the tools and resources used to manage it. To learn how to make a chart of accounts that meets your needs, consider the following resources: Accounting Software: Programs like QuickBooks and Xero offer built-in templates, simplifying COA setup and ensuring compliance with standards. Online Guidelines: The U.S. Small Business Administration provides useful examples to help you tailor your COA to your business operations. Educational Platforms: Websites like AccountingCoach offer materials and quizzes to deepen your comprehension of COA principles. Cloud Solutions: Using cloud-based accounting allows for real-time updates and collaboration, ensuring your COA remains organized and accurate. Additionally, regular training for your staff on COA usage can improve data entry accuracy and support better financial reporting, eventually leading to enhanced compliance and decision-making. Frequently Asked Questions What Is the Chart of Accounts Setup? A chart of accounts setup is a structured list of financial accounts that categorizes your business’s financial transactions. You’ll use unique numerical codes to identify assets, liabilities, equity, revenue, and expenses clearly. By organizing accounts systematically, you guarantee easy tracking and reporting. It’s essential to establish a logical hierarchy, making it simpler to analyze financial data. Regularly review and update your accounts to adapt to your business’s evolving needs and maintain accuracy in reporting. What Is a Chart of Accounts in Simple Terms? A chart of accounts (COA) is fundamentally an organized list that categorizes your company’s financial accounts. You’ll find accounts grouped into assets, liabilities, equity, revenue, and expenses. Each account gets a unique alphanumeric code, making it easy for you to track transactions. The structure of the COA aligns with your financial statements, providing clarity in reporting and aiding in budgeting. A well-structured COA is vital for effective financial management and compliance. What Does the Chart of Accounts Structure Set? The chart of accounts structure sets a systematic framework for organizing financial transactions by categorizing them into five main areas: Assets, Liabilities, Equity, Revenue, and Expenses. Each category has a unique numerical code for easy identification and organization. Subcategories further refine these accounts, aiding clarity in financial reporting. This structure not merely aligns with financial statements but additionally improves compliance, tracking, and informed decision-making, ensuring a thorough overview of your financial environment. What Are the 5 Levels of the Chart of Accounts? The five levels of a chart of accounts include assets, liabilities, equity, revenue, and expenses. Assets, numbered 100-199, represent resources you own. Liabilities, ranging from 200-299, are your obligations to others. Equity accounts, assigned numbers 300-399, show your ownership interest. Revenue, falling between 400-499, tracks income from operations, whereas expenses, coded 600-699, record costs incurred. Each level provides a structured way to organize and analyze your financial transactions effectively. Conclusion To conclude, a well-structured Chart of Accounts is crucial for effective financial management. By categorizing accounts into assets, liabilities, equity, revenues, and expenses, you improve your ability to track transactions and generate precise reports. Establishing a COA requires careful planning and adherence to best practices, ensuring it meets your business needs. Regular maintenance and utilizing appropriate tools can further streamline the process, in the end supporting informed decision-making and compliance with accounting standards. Image via Google Gemini This article, "What Is a Chart of Accounts Setup?" was first published on Small Business Trends View the full article

-

A Chart of Accounts setup is crucial for any business, as it organizes all financial accounts in a structured manner. By categorizing accounts into assets, liabilities, equity, revenues, and expenses, you create a framework that allows for efficient tracking of transactions. Each category is assigned specific numerical codes, which aids in accurate reporting and analysis. Comprehending how to properly establish and maintain your Chart of Accounts can greatly impact your financial management practices. What are the key components you should consider? Key Takeaways A Chart of Accounts (COA) is a systematic list of financial account titles organized into categories: assets, liabilities, equity, revenue, and expenses. Each account in the COA is assigned a unique numerical code for easy identification and retrieval, facilitating effective transaction recording. The structure includes main categories with sub-accounts for detailed tracking tailored to specific business needs and financial reporting. Regular updates and reviews of the COA ensure it remains relevant, effective, and aligned with evolving business requirements and compliance standards. Accounting software can simplify COA setup, offering templates and tools for organization, automation, and collaboration in real-time. Understanding Chart of Accounts The chart of accounts (COA) serves as the backbone of an organization’s financial reporting system, providing a structured framework for categorizing all financial transactions. Fundamentally, the chart of accounts definition refers to a systematic list of all financial account titles used in your general ledger. This list is categorized into five primary sections: assets, liabilities, equity, revenues, and expenses. Each account in the COA is assigned a unique numerical code, often following a structured numbering system, which simplifies classification and retrieval. This structure not only improves clarity in financial reporting but also supports budgeting and forecasting. By using a well-structured COA customized to your organization’s specific needs, you can guarantee effective transaction recording and gain detailed insights into your financial performance over various periods. In the end, a well-organized COA is vital for maintaining accurate records and complying with accounting standards. Key Components of a Chart of Accounts Comprehending the structure of a chart of accounts is critical for effective financial management. A typical chart of accounts setup includes five main account categories: Assets, Liabilities, Equity, Revenue, and Expenses. Each account is assigned a unique numerical code, often following a specific chart of accounts format—for example, 100-199 for assets and 200-299 for liabilities. This coding system facilitates easy identification and retrieval of accounts. Additionally, you can create sub-accounts under main categories to provide more detail and organization, allowing you to track specific transactions by business function or division. During the setup process, it’s crucial to take into account your business’s operational needs, ensuring the chart accommodates future growth and financial reporting changes. Regular reviews and updates to the chart are critical, as they maintain its relevance and effectiveness in accurately reflecting your company’s financial activities. Importance of a Well-Structured COA A well-structured chart of accounts (COA) improves financial clarity by organizing transactions into distinct categories, which makes it easier for you to track your financial performance. This organization supports accurate reporting, ensuring compliance with accounting standards and providing stakeholders with reliable insights into the company’s health. Furthermore, a properly set up COA facilitates efficient analysis, allowing you to make informed decisions and improve operational efficiency. Enhances Financial Clarity When you implement a well-structured Chart of Accounts (COA), it greatly improves financial clarity for your business. A clear COA systematically categorizes financial transactions, making it easier to analyze data. Here are four key benefits: Organized Structure: By grouping accounts into assets, liabilities, equity, revenue, and expenses, you create a thorough framework for financial analysis. Performance Tracking: A clear COA supports budgeting and forecasting, allowing you to identify cost control areas. Quick Identification: A numeric coding system boosts the retrieval of financial information, streamlining reporting processes. Ongoing Relevance: Regular updates to the COA guarantee it remains aligned with your operations, preventing confusion in financial reporting. Supports Accurate Reporting Accurate reporting is vital for any business, and a well-structured Chart of Accounts (COA) plays an important role in achieving this goal. A well-organized chart of accounts list categorizes financial transactions into specific accounts, enhancing clarity in reporting. By systematically classifying assets, liabilities, equity, revenues, and expenses, the COA allows for detailed financial analysis, which is critical for informed decision-making. Furthermore, a properly configured COA supports compliance with accounting standards, guaranteeing consistency across reporting periods. It likewise aids in budgeting and forecasting, helping you pinpoint areas for cost control and operational improvements. Regular reviews and updates confirm the COA remains aligned with your evolving business needs, thereby maintaining the accuracy and relevance of your financial reports. Facilitates Efficient Analysis Even though you might think of a Chart of Accounts (COA) as just a list of account names, its role in facilitating efficient financial analysis is far more significant. A well-structured COA improves your comprehension of business performance by: Categorizing transactions for clear visibility into revenue, expenses, and assets. Enabling accurate budget forecasting and variance analysis to identify trends. Streamlining reporting through standardized account codes for quick access to financial info. Supporting compliance with accounting regulations, reducing misstatement risks. Categories Within the Chart of Accounts Grasping the categories within the chart of accounts (COA) is essential for effective financial management, as they provide a structured way to organize a business’s financial data. The COA consists of five primary categories: Assets, Liabilities, Equity, Revenue, and Expenses. Assets represent resources like cash and inventory, classified as current or non-current based on liquidity. Liabilities include obligations to external parties, such as loans and accounts payable, categorized into current and long-term liabilities. Equity reflects the owner’s interest in the business, including common stock and retained earnings. Revenue accounts track income from business operations, whereas chart of accounts expense categories record costs incurred to generate that revenue. Comprehending these categories helps you assess financial performance and make informed decisions, ensuring your business remains financially healthy and organized. Setting Up Your Chart of Accounts Setting up your chart of accounts starts with establishing clear account naming conventions that reflect the nature of each account. You’ll need a numerical coding system, typically five digits, to categorize accounts effectively, ensuring each code indicates its primary category. Organizing your accounts into main categories like Assets and Liabilities, along with thoughtful subcategories, will improve your financial tracking and reporting. Account Naming Conventions When you’re establishing your chart of accounts, having clear and consistent account naming conventions is crucial for effective financial management. Prioritizing clarity and simplicity helps everyone understand the purpose of each account, especially those without accounting backgrounds. Here are some key points to take into account: Use prefixes or common abbreviations (e.g., “Rev” for revenue, “Exp” for expenses) to improve organization. Maintain consistency in naming across the chart of accounts; similar accounts should follow the same structure. Avoid overly complex or lengthy names; concise, descriptive names maintain clarity. Periodically review and update account names to reflect changes in business operations or industry standards. Implementing these strategies will streamline your chart of accounts numbering and enhance financial reporting. Numerical Coding System A well-structured numerical coding system is fundamental for organizing your chart of accounts effectively. This system typically assigns a range of numbers to categorize accounts, with assets coded from 100-199, liabilities from 200-299, equity from 300-399, revenues from 400-499, and expenses from 500-599. Each account receives a unique identifier, facilitating easy organization and retrieval of financial data. The first digit indicates the main category, whereas subsequent digits can represent subcategories or specific accounts, thereby creating a hierarchical structure. Gaps between account numbers are often left intentionally for future additions. When setting up your chart of accounts, verify the coding aligns with your company’s operations and reporting needs, aiding both internal management and external compliance. Organizing Account Categories Organizing account categories is crucial for an efficient chart of accounts, as it improves clarity and structure in financial reporting. To effectively set up a chart of accounts for a business firm, consider these key categories: Assets: Items owned by the business. Liabilities: Obligations owed to others. Equity: Owner’s interest in the business. Revenue and Expenses: Income generated and costs incurred. Assign unique numerical codes to each account, starting with a digit representing its category. Create sub-accounts for detailed tracking, like operational expenses for salaries, rent, and utilities. Tailor the chart to your firm’s specific needs and review it regularly to make sure it remains relevant and effective for accurate financial analysis. Common Challenges in COA Management Managing a chart of accounts (COA) presents several common challenges that can considerably impact financial accuracy and reporting. One major issue is overcomplication, which can lead to data entry errors and hinder staff from accurately recording transactions. Furthermore, a lack of standardization in account naming and structure can create reconciliation problems, resulting in discrepancies that affect financial analysis. Duplicate categories further complicate your ability to compare financial data effectively, making it tough to assess business performance. Misalignment of the chart of accounts with your financial reports can lead to compliance issues, as inaccurate classifications may violate accounting standards or tax regulations. Regular maintenance is crucial to avoid clutter and inconsistencies, ensuring your chart of accounts accurately reflects the current state of the business and supports necessary financial reporting needs. Addressing these challenges proactively can help streamline your financial processes and improve overall accuracy. Best Practices for Maintaining a COA To maintain an effective chart of accounts (COA), you should regularly update it, ideally at least once a year, to guarantee it aligns with your current business operations. Simplifying account structures by using standardized naming conventions can improve consistency and make navigation easier for users. Regular Updates Required Regular updates to your chart of accounts (COA) are crucial for accurately reflecting the financial status of your organization, especially as business operations evolve. To maintain a relevant and effective table of accounts, consider these best practices: Perform periodic reviews—ideally quarterly or annually—to assess the COA’s effectiveness. Maintain consistency in account naming conventions and structures to improve clarity in financial reporting. Incorporate feedback from team members and stakeholders during reviews to identify potential improvements or new account needs. Utilize accounting software to automate updates, ensuring that changes are efficiently implemented and the COA remains organized. Simplify Account Structures When simplifying account structures, it’s essential to create account names that are clear and concise, as this helps minimize confusion during data entry and analysis. Establish a logical numbering system for your standard chart of accounts, categorizing accounts by type—like using 1 for assets and 2 for liabilities. This approach allows for future additions without disrupting the existing structure. Regularly review your chart of accounts to eliminate obsolete accounts and consolidate similar ones, maintaining relevance. Implementing sub-accounts can help categorize detailed transactions without complicating main categories. Furthermore, utilizing accounting software streamlines management, offering automation, real-time updates, and improved insights into financial performance, making your system more efficient and organized. Examples of Chart of Accounts Comprehending the examples of a chart of accounts is essential for effective financial management, as it provides a structured framework for organizing a business’s financial information. A well-structured chart includes various categories, each with specific examples. Here are some common examples of chart of accounts: Asset Accounts: Cash (101) Accounts Receivable (102) Inventory (103) Liability Accounts: Accounts Payable (201) Short-Term Loans (202) Revenue Accounts: Sales Revenue (401) Service Income (402) Expense Accounts: Rent Expense (501) Salaries Expense (502) Advertising Expense (503) These examples of chart of accounts help you categorize and track your business’s financial activities, ensuring accurate reporting and analysis. Impact of COA on Financial Reporting The impact of a well-structured Chart of Accounts (COA) on financial reporting is significant, as it lays the groundwork for accurate and clear financial statements. A properly organized accounting chart of accounts categorizes transactions into distinct accounts, minimizing misclassifications that could distort your financial data. This structure not just aids in compliance with accounting standards but furthermore guarantees consistent recording of all transactions, making it simpler to generate compliant reports for stakeholders. Tools and Resources for Effective COA Management A well-organized Chart of Accounts (COA) is only as effective as the tools and resources used to manage it. To learn how to make a chart of accounts that meets your needs, consider the following resources: Accounting Software: Programs like QuickBooks and Xero offer built-in templates, simplifying COA setup and ensuring compliance with standards. Online Guidelines: The U.S. Small Business Administration provides useful examples to help you tailor your COA to your business operations. Educational Platforms: Websites like AccountingCoach offer materials and quizzes to deepen your comprehension of COA principles. Cloud Solutions: Using cloud-based accounting allows for real-time updates and collaboration, ensuring your COA remains organized and accurate. Additionally, regular training for your staff on COA usage can improve data entry accuracy and support better financial reporting, eventually leading to enhanced compliance and decision-making. Frequently Asked Questions What Is the Chart of Accounts Setup? A chart of accounts setup is a structured list of financial accounts that categorizes your business’s financial transactions. You’ll use unique numerical codes to identify assets, liabilities, equity, revenue, and expenses clearly. By organizing accounts systematically, you guarantee easy tracking and reporting. It’s essential to establish a logical hierarchy, making it simpler to analyze financial data. Regularly review and update your accounts to adapt to your business’s evolving needs and maintain accuracy in reporting. What Is a Chart of Accounts in Simple Terms? A chart of accounts (COA) is fundamentally an organized list that categorizes your company’s financial accounts. You’ll find accounts grouped into assets, liabilities, equity, revenue, and expenses. Each account gets a unique alphanumeric code, making it easy for you to track transactions. The structure of the COA aligns with your financial statements, providing clarity in reporting and aiding in budgeting. A well-structured COA is vital for effective financial management and compliance. What Does the Chart of Accounts Structure Set? The chart of accounts structure sets a systematic framework for organizing financial transactions by categorizing them into five main areas: Assets, Liabilities, Equity, Revenue, and Expenses. Each category has a unique numerical code for easy identification and organization. Subcategories further refine these accounts, aiding clarity in financial reporting. This structure not merely aligns with financial statements but additionally improves compliance, tracking, and informed decision-making, ensuring a thorough overview of your financial environment. What Are the 5 Levels of the Chart of Accounts? The five levels of a chart of accounts include assets, liabilities, equity, revenue, and expenses. Assets, numbered 100-199, represent resources you own. Liabilities, ranging from 200-299, are your obligations to others. Equity accounts, assigned numbers 300-399, show your ownership interest. Revenue, falling between 400-499, tracks income from operations, whereas expenses, coded 600-699, record costs incurred. Each level provides a structured way to organize and analyze your financial transactions effectively. Conclusion To conclude, a well-structured Chart of Accounts is crucial for effective financial management. By categorizing accounts into assets, liabilities, equity, revenues, and expenses, you improve your ability to track transactions and generate precise reports. Establishing a COA requires careful planning and adherence to best practices, ensuring it meets your business needs. Regular maintenance and utilizing appropriate tools can further streamline the process, in the end supporting informed decision-making and compliance with accounting standards. Image via Google Gemini This article, "What Is a Chart of Accounts Setup?" was first published on Small Business Trends View the full article

-

SEO ranking is a webpage’s organic position for a search engine query. Here‘s what influences it. View the full article

-

Twenty years ago, honeybees first started to disappear in mysteriously large numbers. Stories in the media were everywhere, as were solutions to try to save the bees. But today, you hear less about the crisis. Has it simply been drowned out by the constant hum of breaking world news, or is the bee crisis over? There are some people who argue that we have “saved” the bees, while others say honeybees never needed saving in the first place. In truth, the problem hasn’t gone away. “Our losses have been getting higher and higher over the last few years,” says Zac Browning, a fourth-generation beekeeper from North Dakota. This winter, he lost more than half of his bees. Nationwide, commercial beekeepers lost an average of 62% of their colonies last winter. Honeybees may not need saving from extinction. But commercial beekeeping may one day no longer be economically sustainable—and the same environmental pressures facing managed bees are also pushing wild pollinators toward collapse. The situation isn’t quite the same as it was in 2006, when beekeepers started reporting a strange new phenomenon: Adult bees were suddenly disappearing from their hives. That became known as colony collapse disorder. That specific scenario is rarer now, but scores of bees have been dying off every winter since then. “We’re still seeing unsustainable losses,” says Christina Grozinger, an entomology professor at Penn State University. Over the last two decades, beekeepers have often lost up to 30% to 40% of their colonies over the winter, and that’s “very difficult for beekeepers to manage,” she says. As previously mentioned, honeybees aren’t likely to go extinct. Beekeepers can manage their populations by “splitting” a hive to produce more bees, or by purchasing more bees when there’s a large loss. But it’s hard to keep going. “Generally, when you lose 50% of your hives, it’s a sign that the operation is weak,” Browning says. “It’s suffering from some sort of disease or other malady. And so that’s not a recipe for having healthy bees that split well. From an economic perspective, it’s absolutely not sustainable for a beekeeping operation to lose more than 25% of its hives in one year.” With inflation, and the interest on money borrowed to repeatedly rebuild hives, “everything compounds,” he says. “The general economic viability of the industry, and certainly the operation, is less and less. You see operations failing if they have more than 25% losses year over year. You can certainly rebuild, but you can’t sustain rebuilding every year.” If beekeepers lose too many bees, it also makes it challenging to provide pollination services. At an almond orchard, for example, insurance companies require two hives per acre to make sure that trees are fully pollinated. (California’s almond crop uses an estimated 1.7 million hives, with 80 billion bees.) Beekeepering companies have been forced to partner with others to meet the obligations in their contracts. Browning says that’s why, so far, farmers are still able to produce crops that rely on honeybees for pollination, from almonds to blueberries. The question isn’t whether honeybees will disappear, but whether the business model that supports them can survive. For wild pollinators that don’t have support from human managers, the situation is more complex. A recent Washington Post article argued that we’ve been worrying about honeybees when we should have been worrying about wild bees. All bees are dealing with a reduction in habitat and less access to the flowers they need to survive, along with more exposure to pesticides. Climate change is also affecting when flowers bloom. Honeybees have some extra stress when they travel long distances to provide pollination—some colonies are trucked 2,000 miles to pollinate almonds—and because they often have poor nutrition from feeding on flowers from a single crop. They are also vulnerable to Varroa mites, a pest that causes disease. (Both managed and wild honeybees face clear challenges, and most of the problems overlap. “It’s not a helpful narrative, because they’re really facing the same issues,” Grozinger says.) When colony collapse disorder first got headlines, it helped bring more attention to other bees—though it’s true that the spotlight was still on honeybees. “I think the first thing it did was to wake up a lot of people to the fact that pollinators were really important to both agriculture and to ecosystems,” says Scott Black, executive director of the nonprofit Xerces Society for Invertebrate Conservation. “So that’s number one. But number two, everyone thought, ‘Pollinators equal honeybees.’” Some “solutions” that became popular to help bees were misguided—like bee hotels, which some scientists have called “beewashing,” or adding hives to corporate rooftops. But this doesn’t do anything to help farmers. Since honeybees aren’t native to the U.S., having them in the wrong places can mean that they overgraze flowers. Consequently, not enough pollen is left for native pollinators, Black says. (In an ideal world for native bees, maybe honeybees shouldn’t have been imported to North America in the first place. It’s inarguable, though, that they’re a necessary part of the food system as it currently exists.) All of the various plans to help honeybees can help wild pollinators as well. This includes reducing pesticide use—both on farms and the 40 million acres of lawns in the U.S.— and restoring wildflowers, Black says. Whatever the solution, the lack of focus on bee health isn’t because the issues are fixed: Both managed and wild bees clearly need help. Hundreds of native North American pollinators are now at risk of extinction. The question isn’t whether honeybees need saving. It’s whether we’re willing to fix the conditions that are hurting all pollinators. View the full article

-

The best PR tools include Semrush‘s AI PR Toolkit, PitchFriendly, GlobeNewswire, and Media Monitoring. View the full article

-

Ukraine’s president says military teams dispatched across the Gulf had delivered ‘positive’ resultsView the full article

-

SISTRIX analyzed German search results after the March core update and found uneven visibility shifts across categories, with some site types hit harder than others. The post Google March Core Update Left 4 Losers For Every Winner In Germany appeared first on Search Engine Journal. View the full article

-

Meeting in Beijing with Chinese president first of its kind in a decadeView the full article

-

Nobody wants to sound weak. We all have a desire to be heard and taken seriously when we speak in meetings and other situations. But so many people pack their prose with words that discourage people from taking them seriously. Avoid the following words if you want to come across as a strong, convincing speaker. 1) JUST This word is an attention killer! Yet it is used all the time by speakers. For example “I just want to say,” or “It’s just a thought,” or “Let me just add that….” In all these instances the word “just” reduces the speaker by suggesting that what follows is of little value. A throwaway gift to the audience. By removing “just” from your speaking you will give more weight to your ideas. And you’ll find when you do this, removing the word “just” leads you to remove the weak words that surround it. So “It’s just a thought” might become ‘It is something I have thought a lot about.” 2) Only This word minimizes what you are saying, and reduces your impact. Examples of this are “I only said that because,” or “I only meant,” or “It’s only a thought.” These expressions diminish the speaker by creating an apologetic tone, thereby making the speaker sound unsure. 3) SORRY “I’m sorry” comes out of the mouth of a speaker when he or she has slipped up in some way. It might be when the speaker has missed a slide or bungled some aspect of a presentation. But calling attention to that, rather than simply moving on, undercuts the speaker. Suppose you are giving a presentation and you realize you have missed a slide. Well, don’t apologize . . . say “there was actually a slide that came before this one.” Then show it. Be positive, even when you have messed up. 4) Apologies in general Speakers often apologize for anything and everything, and in so doing they direct the audience’s attention to what they view as a flaw in their performance. They apologize for their tardiness (“apologies for my lateness, I had a meeting that went overtime), their behavior (“my apologies for cancelling last week’s meeting) or their directives (“apologies that you had to do this project on the weekend”). The problem with apologizing is that it places the focus on something negative about you. And your audience will see you through that lens. 5) Not sure We often hear speakers say “I’m not sure about this” or “I’m not sure we can do that.” While their intention may be good—“not sure” casts a negative note. If you’re not sure about something, say “We may be able to proceed. Here’s where I stand on this.” Then share your thinking. In this way you turn the negative into a positive. You’ll come across as thoughtful, rather than unsure. 6) Think, want, feel Verbs are supposed to be high energy words, but some verbs will make you sound weak. You’ll want to part with these three. “I think” makes you sound like you are not sure of yourself. A boss who says “I think we should move forward with this plan” sounds tentative. More convincing would be “I’m convinced we should move forward with this plan” or “I know we should proceed.” “Want” is another verb that makes you sound weak. If your boss says “I want to promote you”, you’ll wonder if she will. Much stronger would be “I have decided to promote you.” Saying you “feel” the program is not workable makes you sound tentative. Instead say “I am convinced the program is not workable.” So resist the temptation to use these low energy words. 7) YOU KNOW, LIKE, UM, THAT’S A GOOD QUESTION How often do we hear speakers attempt to buy more time by using filler words to plug their pauses when they are thinking through their next thought? For example someone answering an interview question might reply “You know… I think a lot about that . . . um . . . because I am always . . . like . . . thinking about how to manage my team.” The speaker’s filler words convey a hesitancy that distracts from the larger idea. Another annoying use of a filler expression is “that’s a good question” when the speaker is about to answer. It is a buy time strategy that doesn’t work because you have been asked to answer the question, not evaluate it. Instead of filling your pauses with empty words when you are thinking through what to say, pause in silence and avoid filler expressions. You will sound more confident, and your silence will give your listener time to process your previous thought. To take your communications to a higher level, avoid these words that weaken the impression you create. Leadership at every level requires the projection of confidence. View the full article

-

An analysis of 400+ websites found five characteristics associated with estimated organic traffic gains. The post What 400 Sites Reveal About Organic Traffic Gains appeared first on Search Engine Journal. View the full article

-

Producer price index for the world’s dominant manufacturer turns positive year on year for the first time since 2022View the full article

-