All Activity

- Past hour

-

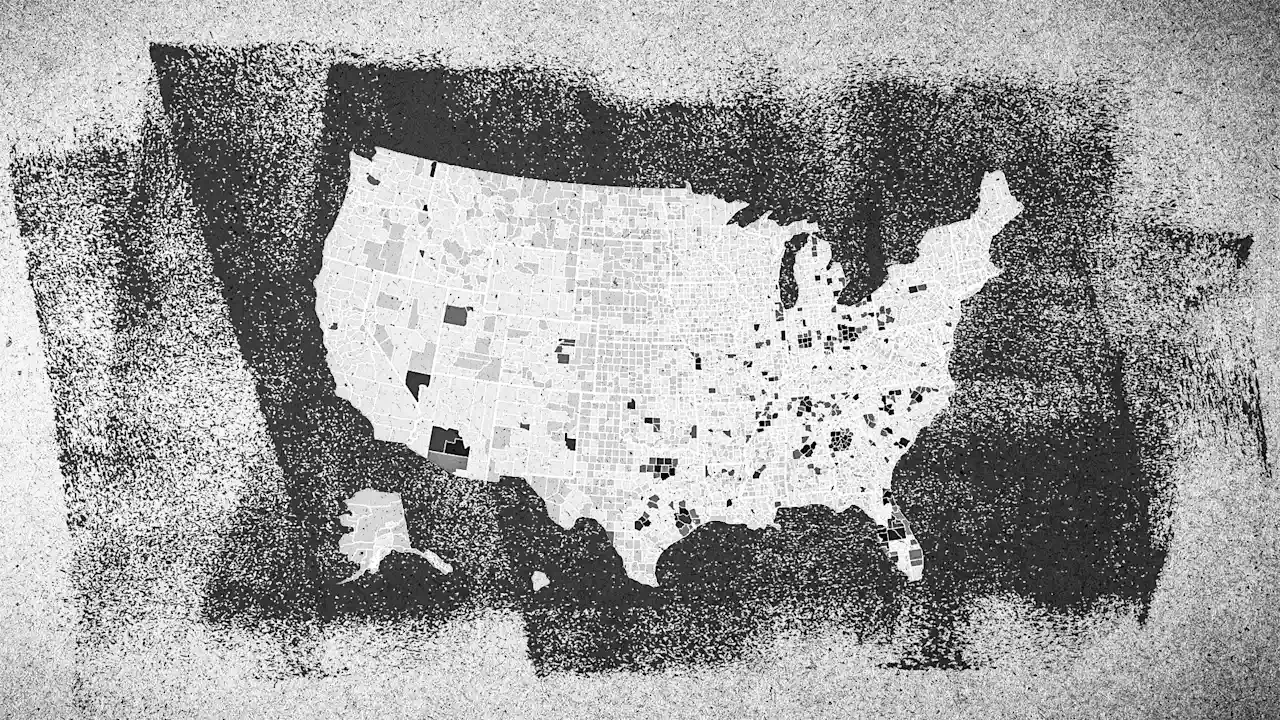

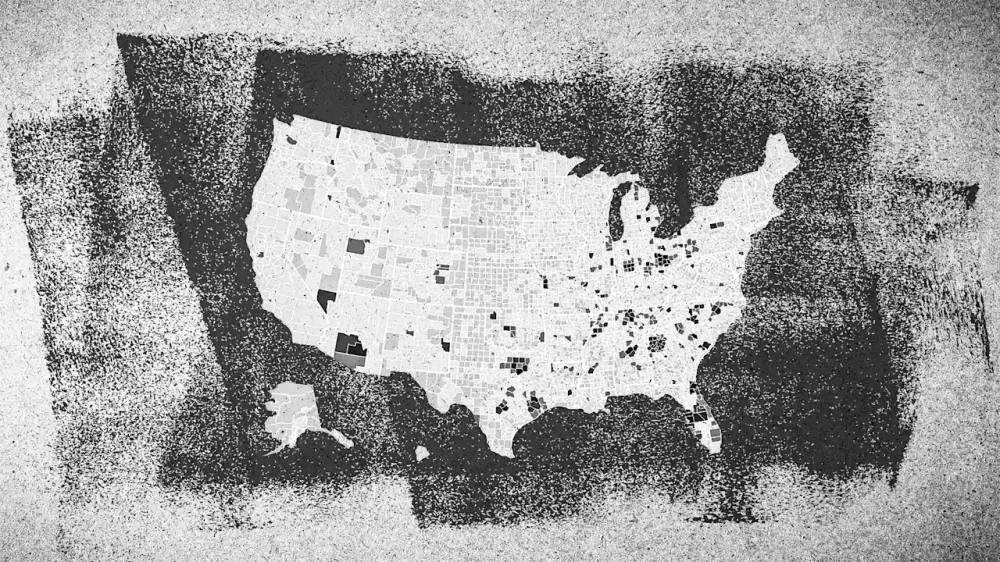

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. Back on January 7, President Donald The President announced: “I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it.” On January 20, The President went further, outlining elements of the proposed “ban.” The order directed multiple federal agencies—including HUD, the Department of Agriculture, the VA, the GSA, and the Federal Housing Finance Agency—to issue guidance within 60 days limiting the federal government’s role in facilitating institutional purchases of single-family homes that could otherwise be bought by owner-occupants. Specifically, within 60 days, the government-sponsored enterprises (Fannie Mae and Freddie Mac) would no longer be permitted to approve, insure, guarantee, or securitize single-family home purchases by “large institutional investors.” The order also stated that, within 30 days, the administration would define “large institutional investors” and that build-to-rent transactions would be exempt. On Thursday (February 19), the Wall Street Journal reported that the White House has settled on a key detail of its proposed ban—one it plans to send to Congress—prohibiting large investors, defined as entities owning 100 or more homes, from purchasing additional single-family houses. Because the threshold is set at 100 homes, the policy would affect not just major institutional landlords, but also some larger individual investors. The plan still includes the build-to-rent exemption and adds another carveout: large investors can continue to purchase homes in need of “significant repair.” Those two proposed exemptions are notable given that most institutional activity right now is in build-to-rent, and when purchasing scattered-site homes, institutional investors—at least when they are actively buying—tend to target properties that require sizable renovation spending. Notably, this proposal would not mandate large investors to liquidate existing holdings. The measure announced on Thursday would need congressional approval, and its prospects are uncertain. According to reporting from the Wall Street Journal, passage is still far from guaranteed. At the height of the Pandemic Housing Boom, large investors—those owning at least 100 single-family homes—made up an all-time high of 3.1% of home purchases in Q2 2022, according to John Burns Research and Consulting. That period, at the tail end of the boom, was when yields were particularly attractive as borrowing costs were ultra-low, home prices were soaring, and rents were climbing rapidly. However, since mortgage rates spiked and capital markets shifted, their share has fallen to around 1.0% of transactions over the past three years. The math isn’t as favorable right now. ResiClub members (paid tiers) can find an interactive version of the map below here On a national level, “large investors”—those owning at least 100 single-family homes—only own around 1% of total single-family housing stock. That said, in a handful of regional housing markets, institutional and large single-family landlords have a much larger presence. Markets like Phoenix and Atlanta became major hubs for institutional single-family rental investment following the 2008 housing crash as the asset class started to institutionalize. Firms such as Invitation Homes, Progress Residential, and AMH built sizable portfolios in these metros by acquiring distressed homes. That early activity helped establish a reliable local SFR ecosystem—including property management firms, leasing infrastructure, and contractor networks—that makes it easier to scale and expand single-family rental and build-to-rent operations today. View the full article

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. Back on January 7, President Donald The President announced: “I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it.” On January 20, The President went further, outlining elements of the proposed “ban.” The order directed multiple federal agencies—including HUD, the Department of Agriculture, the VA, the GSA, and the Federal Housing Finance Agency—to issue guidance within 60 days limiting the federal government’s role in facilitating institutional purchases of single-family homes that could otherwise be bought by owner-occupants. Specifically, within 60 days, the government-sponsored enterprises (Fannie Mae and Freddie Mac) would no longer be permitted to approve, insure, guarantee, or securitize single-family home purchases by “large institutional investors.” The order also stated that, within 30 days, the administration would define “large institutional investors” and that build-to-rent transactions would be exempt. On Thursday (February 19), the Wall Street Journal reported that the White House has settled on a key detail of its proposed ban—one it plans to send to Congress—prohibiting large investors, defined as entities owning 100 or more homes, from purchasing additional single-family houses. Because the threshold is set at 100 homes, the policy would affect not just major institutional landlords, but also some larger individual investors. The plan still includes the build-to-rent exemption and adds another carveout: large investors can continue to purchase homes in need of “significant repair.” Those two proposed exemptions are notable given that most institutional activity right now is in build-to-rent, and when purchasing scattered-site homes, institutional investors—at least when they are actively buying—tend to target properties that require sizable renovation spending. Notably, this proposal would not mandate large investors to liquidate existing holdings. The measure announced on Thursday would need congressional approval, and its prospects are uncertain. According to reporting from the Wall Street Journal, passage is still far from guaranteed. At the height of the Pandemic Housing Boom, large investors—those owning at least 100 single-family homes—made up an all-time high of 3.1% of home purchases in Q2 2022, according to John Burns Research and Consulting. That period, at the tail end of the boom, was when yields were particularly attractive as borrowing costs were ultra-low, home prices were soaring, and rents were climbing rapidly. However, since mortgage rates spiked and capital markets shifted, their share has fallen to around 1.0% of transactions over the past three years. The math isn’t as favorable right now. ResiClub members (paid tiers) can find an interactive version of the map below here On a national level, “large investors”—those owning at least 100 single-family homes—only own around 1% of total single-family housing stock. That said, in a handful of regional housing markets, institutional and large single-family landlords have a much larger presence. Markets like Phoenix and Atlanta became major hubs for institutional single-family rental investment following the 2008 housing crash as the asset class started to institutionalize. Firms such as Invitation Homes, Progress Residential, and AMH built sizable portfolios in these metros by acquiring distressed homes. That early activity helped establish a reliable local SFR ecosystem—including property management firms, leasing infrastructure, and contractor networks—that makes it easier to scale and expand single-family rental and build-to-rent operations today. View the full article

- Today

-

A turf war has broken out between the fandoms of Breaking Bad and Game of Thrones over the highest-rated episode spot on IMDb. Released last month, the Game of Thrones spin-off A Knight of the Seven Kingdoms, set a century before the events of the HBO drama, has garnered much praise. A Guardian reviewer said it has “saved the Game of Thrones universe.” Fans appear to agree, as the fifth episode, In the Name of the Mother, which aired February 15, briefly secured a rare 10/10 rating on IMDb. Unfortunately for fans, it didn’t last long. For over a decade, “Ozymandias”—the 14th episode of the fifth and final season of Breaking Bad, and the climax of the series—had been the only television episode to secure a perfect 10 rating on IMDb. It’s an accolade fans weren’t prepared to give up lightly. Taking matters into their own hands, according to reports across Reddit and X, fans of the crime drama started review-bombing the A Knight of the Seven Kingdoms episode with one-star ratings to tank its score. The “Ozymandias” episode of ‘BREAKING BAD’ has dropped to a 9.9 on IMDb. It held a 10/10 rating on the platform for almost 13 years. pic.twitter.com/9zLtW00a01 — DiscussingFilm (@DiscussingFilm) February 20, 2026 One IMDb reviewer admitted as much, writing, “I like this episode. I like this show overall. Hell, I love this episode. But… its not 1% as good as the episode mentioned in the title of this review is. I therefore decide the leave this one star review in order to defend the number one episode.” What followed was an all-out review-bombing war between the two fandoms. On the IMDb review page for “Ozymandias,” a slew of reviews titled “The Lannisters Send Their Regards” or “Winter came for Breaking Bad! The North remembers” started appearing. Meanwhile, of the hundreds of one-star reviews A Knight of the Seven Kingdoms has accumulated on IMDb so far, many hit back “in the name of walter white” or “For Heisenberg.” For the first time in 13 years, the Breaking Bad episode lost its perfect score on the site. At the time of writing, neither episode is in the top 10 list on the platform—or even the top 100. A Knight of the Seven Kingdoms, now with an average score of 9.5, sits at number 519 on the best TV episode ranking. “Ozymandias,” now with an average score of 9.6, has dropped to number 461. The only winner here? Six Feet Under, which has now slipped into the top spot. View the full article

-

A reader writes: I’ve been job searching for a few months now. I just got a call from HR at an organization I applied to a few weeks ago asking me if they had a few minutes to chat — they wanted to go through the position with me, give me some quick updates on the role, and let me know the salary so they could see if I still wanted to be considered. I told them of course, but I only had 15 minutes before a meeting. They said that was fine. Cut to: they’re asking me about my background, my current role, my strengths and weaknesses, what I’m looking for in a new role, and why I’m excited about their mission. It became a 25-minute first round interview. Luckily, I was at a computer so I could quickly google their mission (I’d applied long ago and have applied to many places since then, I almost couldn’t remember their exact mission!). Is this normal? I’ve never had a spur-of-the-moment interview before. And would there have been a polite way to ask if we could reschedule the call? If I had known this was an interview, I would’ve rescheduled so I could’ve been more prepared, but she really made it seem like it would be just five minutes on the phone. I answer this question over at Inc. today, where I’m revisiting letters that have been buried in the archives here from years ago (and sometimes updating/expanding my answers to them). You can read it here. The post surprise phone interviews are the worst appeared first on Ask a Manager. View the full article

-

AI is reshaping how work gets done in institutions, both public and private. However, the impact is uneven—consumer AI chat interfaces like ChatGPT, Copilot, Claude, and Gemini are fundamentally mismatched to the realities of government work. That doesn’t mean government agencies aren’t turning to AI. They cannot hire their way to capacity, so they’re looking to technology to lighten the load. More than half of local governments report difficulty filling positions, a problem especially potent in larger metros. San Francisco’s local government, for example, has more than 4,700 open positions. Since 2020, state government employment has increased, but much of that is a bounce-back from the pandemic, not true growth needed to deliver services with the efficacy governments want. But drop-in chatbots can’t make a significant impact on operations because data within government agencies—and even within individual departments in agencies—is exceedingly siloed. State and local governments are managing budget constraints. IT teams are stretched thin. It’s no surprise, then, that consumer AI tools don’t meet their promise in government institutions. They fundamentally lack all the information they need to be effective in a public service context. THE TOOL GAP Commercial software tools, including AI chatbots, are built for private companies with hierarchies, contracts, and linear processes. Government work is inherently different. Public institutions are cross-organizational, the work is omnidirectional, and success necessitates constant collaboration across agencies, nonprofits, and community partners. Emergency management departments, for example, must identify points of contact within local police departments, fire departments, sheriff’s offices, emergency medical services, utility companies, FEMA regional offices, and community emergency response teams to effectively deliver their service—coordinating disaster response and recovery operations. The sum of these problems—from data siloes to budget constraints to technological roadblocks—is that consumer AI struggles in government institutions because these tools lack the necessary context. Try asking ChatGPT “Provide our current reimbursement process” or “Create a survey to gather feedback on the latest heat season coordination.” These are tasks that require explicit, non-public knowledge. To execute such tasks, AI needs not only access to data that lives across disparate systems, but also governance and rules specifying which definition is best suited for each purpose. And even if you get a good answer, traditional AI is not built to help users know what to do next. THE PATH FORWARD Embedding AI is the path forward to deploy AI in government, effectively overcoming data silos to tackle inter-organizational work. Embeddedness refers to AI that lives directly within the platforms where work happens, within coordination, memory, and decision-making systems—not inside a chatbot. Government is uniquely suited to benefit from AI that’s truly embedded because it has the perfect raw material to make AI maximally useful: conversations, decisions, workflows, institutional memory, and loads of information. In other words, government has context. Unfortunately, most AI chatbots today assume their users work inside of a single organization, and therefore only need context from one organization’s systems. For government, that’s not the reality. A homelessness coordinator in Essex County or an election administrator in New York isn’t just working “at” one organization: they’re juggling relationships, meetings, decisions, and shared knowledge across constantly shifting agencies, nonprofits, contractors, and community partners. The hardest parts are aligning, coordinating, remembering, onboarding, and maintaining shared understanding across people who come and go. Because government work is inherently lateral, true embedded AI has information not only across one organization’s systems but also across its partners’ systems, too. Taking the idea of embeddedness one step further, it’s vital for AI to seemingly “disappear” into public servants’ workflows. If AI is one more tool, one more thing government employees must be trained on, then AI is notembedded in the way it needs to be. Public servants don’t want or need another new widget. They need technology that helps them do what they do faster, better, and more accurately. That is embedded AI. Consider this example: It’s common for certain AI tools to send a summary and action items after a meeting. But embedded AI goes further. It would ask the user if they wanted a follow up email to socialize action items. It could draft the follow-up email, too. Then, after a couple of days, the embedded AI would surface engagement data, showing that someone assigned an action item hasn’t read the follow-up email, and the AI would ask the user if they want a follow-up email, and then draft the note. When a public servant is searching for information, the next step is usually to read it to send something to somebody or take an action. AI that supports that next step without explicit prompting or forcing the user to switch tools is the kind of technology that can help public servants better deliver services more quickly. This is the shift that accelerates action. THE END GOAL It’s vital we do not lose sight of the goal. State and local governments are where the rubber meets the road, turning rules into real services—from handling daily operations to helping low-income people get nutrition assistance, providing veterans services, supporting people experiencing homelessness, and everything in between. Yes, chatbots and similar tools can help one person be more effective. But when AI is embedded, benefits are magnified; people and entire programs are faster and more effective. That means the people who rely upon municipal government services are better served. And that is the ultimate promise of technology, like embedded AI efficiently deployed in government—better communities for all. Madeleine Smith is the CEO and cofounder of Civic Roundtable. View the full article

-

In terms of background checks, knowing which sites offer the best services can save you time and resources. The top five highest-rated options include Iprospectcheck, First Advantage, Checkr, HireRight, and Sterling. Each of these platforms has unique strengths, from rapid processing times to thorough offerings customized for large employers. Grasping what each site can provide is crucial, especially if you’re looking for efficiency and reliability. Let’s explore what sets these platforms apart. Key Takeaways Checkr: Known for rapid results, delivering 89% of checks within one hour, ideal for high-volume employers. Iprospectcheck: Offers personalized searches with competitive pricing and a free background check option, ensuring compliance with regulations. First Advantage: Specializes in large-scale screenings, providing customizable checks and quick turnaround times for multinational employers. HireRight: Features a strong BBB rating, customizable checks, and a focus on customer satisfaction with reliable turnaround times. Sterling: One of the oldest providers, known for extensive checks and strong enterprise-level service, enhancing its offerings post-acquisition by First Advantage. Iprospectcheck Regarding background screening, Iprospectcheck stands out as a reliable choice for businesses looking for customized solutions. Founded in 2009 and based in California, this family-owned provider offers personalized searches that comply with FCRA and local regulations. With pricing options from $24.95 for Basic checks to $79.95 for Premium checks, it accommodates businesses of all sizes. Iprospectcheck is known for its fast turnaround times, often delivering results within one to five business days, which can improve candidate retention in critical industries like staffing and healthcare. They additionally provide an absolutely free background check with no credit card required, allowing you to assess their services risk-free. As one of the highest rated background check sites, they prioritize compliance and ethical practices, ensuring you receive reliable and accurate information. You can further explore their BackgroundCheck free trial background check to experience their offerings firsthand. First Advantage In relation to background screening, First Advantage is a prominent choice for large-scale employers, particularly those operating on an international level. Founded in 2003 and based in Georgia, this global provider specializes in background screening services customized for enterprise-level and multinational corporations. Their pricing structure accommodates various needs, starting from $29 for basic checks to $75 for premium packages. You can likewise take advantage of a 7 day free trial background check to explore their offerings. First Advantage provides customizable searches, including drug screening and coordination of physicals and vaccinations, all in the process of ensuring compliance with FCRA regulations. The turnaround times for background checks typically range from one to four business days, which improves hiring efficiency. Furthermore, First Advantage integrates seamlessly with various applicant tracking systems (ATS), supporting HR functions for large-scale screenings and streamlining the hiring process for employers. Checkr Even though many companies seek efficient solutions for background screening, Checkr stands out as a strong option for high-volume employers. Founded in 2014 and based in San Francisco, Checkr automates the background screening process, enhancing efficiency and speed. With pricing starting at $29.99 for the Basic+ package, you can choose from higher tiers for more thorough checks customized to your needs. One of Checkr’s key advantages is its fast turnaround times, delivering 89% of checks within one hour, greatly improving the candidate experience. In addition, Checkr is FCRA-compliant, ensuring adherence to legal standards. The platform likewise offers customizable packages, allowing you to adjust the screening process to fit specific requirements. With an A+ rating from the Better Business Bureau and strong integration capabilities with various applicant tracking systems (ATS), Checkr positions itself as a reliable choice for employers looking for streamlined background checks. HireRight As you navigate the environment of background screening options, HireRight emerges as a prominent choice for employers seeking personalized solutions. Founded in 1995 and based in Nashville, this global provider offers a range of highly customizable background checks suited to your needs. With pricing starting at $39.95 for the Basic package, you can additionally opt for the Advantage and Advantage Plus packages at $69.95 and $79.95, respectively. HireRight boasts a strong BBB rating of A+, reflecting its commitment to customer satisfaction and quality service. The company guarantees fast turnaround times for background checks, typically ranging from one to five business days, which helps streamline your hiring process. Their thorough suite of services includes criminal background checks, employment verification, and drug testing, all compliant with FCRA and relevant regulations. This makes HireRight a reliable partner in your background screening efforts. Sterling Sterling stands out as one of the oldest background screening providers, having been established in 1975. Specializing in personalized searches and extensive background checks, it caters primarily to enterprise-level companies. With over 103,000 checks completed annually, Sterling demonstrates considerable experience in the background screening industry. The company offers a wide range of services, including criminal background checks, employment verification, and drug testing, all customized to meet the high-volume needs of large organizations. Pricing for Sterling‘s services varies greatly, starting from under $50 to several hundred dollars per check, depending on the complexity and customization required. In 2024, Sterling announced its acquisition by First Advantage, which is expected to improve its capabilities and expand its service offerings within the background screening market. This acquisition may enhance the efficiency and reliability of their services, making Sterling a compelling choice for businesses seeking thorough and adaptable background checks. Frequently Asked Questions Is Been Verified or Truthfinder Better? When deciding between Been Verified and TruthFinder, consider your needs. Been Verified offers unlimited reports for a monthly fee, which can save you money if you need multiple checks. Conversely, TruthFinder thrives in providing detailed public records and features like reverse phone lookup. Both services have positive ratings, but if you value extensive data, TruthFinder might suit you better, whereas Been Verified offers more cost-effective options for frequent users. Which Background Check Is Legit? To determine which background check service is legit, look for providers that comply with the Fair Credit Reporting Act (FCRA) and state regulations. Services like Checkr and iProspectCheck are known for their legal practices. Whereas TruthFinder and Intelius offer extensive public records access, they’re not FCRA-compliant for employment checks. Always check customer reviews and ratings, in addition to certifications from organizations like the Better Business Bureau, to guarantee reliability and trustworthiness. What Is the Most Used Background Check? The most used background check service is Checkr, known for its fast, automated screening process. It boasts an impressive completion rate of 89% of checks within one hour, making it a go-to for many employers. Other services, like iprospectcheck and First Advantage, cater to specific business needs, but Checkr’s efficiency and speed set it apart. Its ability to provide quick, reliable results helps businesses streamline their hiring processes effectively. What Is the Hardest Background Check to Pass? The hardest background check to pass often involves criminal history checks, where felony convictions can impact your chances of employment or housing. Furthermore, extensive employment verification checks can be tough if your resume contains discrepancies in job titles or dates. Credit history checks pose challenges for those with poor credit scores. Finally, international checks can be complex because of varying laws, making it difficult if you have overseas work or residency history. Conclusion To conclude, choosing the right background check service depends on your specific needs. Iprospectcheck offers affordability and speed, whereas First Advantage caters to larger employers with extensive requirements. Checkr is ideal for quick processing times, and HireRight shines with its customer service. Sterling, with its long-standing reputation, provides thorough checks suited for enterprise-level clients. Evaluating these options will help you select the best fit for your background screening needs, ensuring a reliable hiring process. Image via Google Gemini This article, "Top 5 Highest Rated Background Check Sites" was first published on Small Business Trends View the full article

-

For years, retail investors were dismissed by some on Wall Street as “dumb money.” That typically referred to those prone to trading on hype, or chasing trends rather than company or industry fundamentals, or responding late to big market moves. That’s no longer the case. An analysis of where retail investors put their money last year shows they outperformed two of the most popular, professionally managed index funds, SPY and QQQ, whose goal is to mirror the performance of the S&P 500 and Nasdaq 100, respectively. Retail investors accounted for $5.4 trillion in trading activity in 2025 across stocks and exchange-traded funds, or ETFs, according to Vanda, an independent data and research firm. That’s a nearly 47% increase from the previous year and the most going back to at least 2014. “I personally want to dispel the myth of retail being dumb money, because it’s not dumb money anymore,” said Joe Mazzola, head trading and derivatives strategist at Charles Schwab, at an investor education event held in Anaheim, California, last November that drew around 800 of the financial services company’s clients. Many Americans have long invested in the stock market, although largely hands-off through managed funds in retirement plans, such as a 401(k). But over the last decade, the advent of mobile trading apps, zero-commission trading, stock market-focused communities on social media and online tools for education and research has helped usher in a new era of do-it-yourself trading in stocks, crypto and other investments. The COVID-19 lockdowns were an inflection point. A new crop of investors, many young newcomers using investing apps like Robinhood, helped drive the “meme stock” frenzy that catapulted the price of GameStop, AMC Entertainment and other stocks. Meme stocks aside, years of mostly uninterrupted, strong stock market gains provided an attractive backdrop for more people to take up investing. The benchmark S&P 500 has posted an annual loss only three times going back to 2015. By early last year, the number of people moving money from checking accounts to investment accounts reached its highest levels since 2021, according to a report by JPMorgan Chase. Some may have been younger Americans who couldn’t afford to buy a house and instead put the money in stocks, the report suggests. All told, money coming into the market from individual investors jumped about 50% from 2023 to early 2025, according to the report. “I would say they are considerably more important as a force in markets right now,” said Steve Sosnick, chief strategist at Interactive Brokers. “Markets used to be really dominated by institutional investors, but if you put enough ants together, they can move a very big log.” Buying the dip Frank Sabia from Encino, California, started dabbling in investing in 2018. Over the years, he’s leveled up his market and trading knowledge by joining private investor chat groups online or attending investing seminars like Schwab’s. “I learned a lot more about options strategies and charting and everything from there,” he said in an interview in November. “Now I’m independent. I just look for my own trades. I have my own strategy. I hunt on my own.” Sabia, a high school registrar, said he trades in cryptocurrencies and other assets, but that his “bread and butter” is options trading. That involves trading contracts to buy or sell a stock at a specific price before a specified date. This can be less costly upfront than buying stocks, but can also be riskier, because options expire and a small move in a stock’s price can translate into a big swing in the value of options contracts. Last April, Sabia opened a Roth IRA account and bought into the market as stocks tanked after President Donald The President announced a sweeping set of tariffs that were more severe than investors expected. The announcement sent the S&P 500 into a two-day tailspin of more than 10%, the type of plunge not seen since the 2020 COVID crash. “I just bought the dip,” Sabia said. He was wasn’t alone. Retail investors seized on the market skid, buying more than $5 billion in stocks over the two days, according to Vanda. “In April, it was retail (investors) that bought the dip,” Mazzola said. “They were the ones that were willing to step in front. They saw the opportunity.” Retail investors also had one of their biggest buy-the-dip days of the year on Oct. 10, when the market dropped 2.7% after The President threatened a “massive increase on tariffs” on China. The AI trade and silver Retail investors haven’t slowed down this year. Their trading activity hit an all-time high on a rolling monthly basis last month, according to J.P. Morgan. They were particularly active in the last week of January, coinciding with the S&P 500 climbing to an all-time high. Retail traders also had a hand in turbocharging the price of silver last month to record highs by buying a record amount of silver ETFs, according to data from Vanda. A recent analysis by Charles Schwab of trading and stock positions by its millions of retail investor clients found they were net buyers of stocks in January, with Microsoft, Netflix and Tesla among the most popular stock buys. Some take on more risk Many retail investors have gone beyond stocks or ETFs and into other investment vehicles. Options trading, which can expose them to higher risk, accounted for about $650 billion of retail investors’ trading last year and has been mostly rising steadily going back to at least 2019, according to Vanda. Noah Goodwin, a junior in high school in the L.A. suburb of Castaic, started options trading on Robinhood Markets early last year using in his mother’s custodial account. It paid off right away. He bought $148 worth of Nvidia options on Jan. 20, 2025, the same day shares of the tech giant plunged on news of AI advances by Chinese startup DeepSeek. Goodwin sold his options later that day. “I made a $200 profit. My very first trade!” Goodwin said in an interview in November. Not all his trades have gone his way. In July, he thought he could capitalize on market volatility caused by more uncertainty over tariffs, but he miscalculated. “I lost a lot of money, like probably like around $600 to $800,” he said. “So, a horrible month for me.” “For the most part, with only some exceptions, buying the dip has tended to be a very profitable tactic for many retail investors,” said Sosnick. But he cautioned that the strategy had led to retail investors making trading decisions without giving full consideration to the risks and rewards. “The risk to it is that for many of them it’s become sort of mechanical,” he said. Balancing short-term and long-term trading It’s not uncommon for retail investors to strike a balance between higher-risk moves and making trades to build out a long-term investment portfolio. Andy Hu, a financial analyst in Los Angeles who attended the Schwab event in November, said he had 50% of his investment portfolio in the SPDR S&P 500 ETF Trust, a popular fund that aims to track the performance of the S&P 500. For his short-term trades, he tends to buy micro-cap stocks, which are very small publicly traded companies that can see big swings in price because of small trading volume. The approach had his active trading account up by around 20% through the first 11 months of last year, he said. Hu stopped making trades toward the end of last year when a pullback in big tech companies helped drag the S&P 500 to a monthly loss in December, clouding sentiment on Wall Street. “I haven’t made a single trade in the last two months,” Hu said. —Alex Veiga, AP Business Writer View the full article

-

Move comes after details of peer’s relationship with Jeffrey Epstein revealed in US justice department documentsView the full article

-

Google’s Gemini app is stepping into the spotlight with its latest feature: enhanced audio verification capabilities that could significantly benefit small business owners. With a focus on responsible AI use, Gemini aims to streamline content creation while ensuring copyright compliance—a crucial balance in today’s digital landscape. At the heart of this innovation is the integration of SynthID, Google’s imperceptible watermark that identifies AI-generated content across various media formats, including audio. For small business owners who rely on original content to promote their brands, this is an important tool. By uploading audio files into the Gemini app, users can now quickly verify whether the content was generated using Google AI, helping to prevent the unintentional use of copyrighted materials. “This new verification feature helps creators know if their content is safe to use,” said a Google representative. “It broadens the capacities of the Gemini app and reinforces our commitment to responsible AI development.” The Gemini app has evolved since its inception, focusing on collaboration with the music community. Lyria 3, the latest iteration of their music generation tool, is designed not to mimic existing artists but to generate original compositions inspired by broader creative styles. This is particularly advantageous for businesses looking to craft unique soundtracks or jingles without running afoul of copyright laws. Small business owners can utilize Lyria 3 in various ways: Custom Soundtracks: Whether it’s a promotional video or a podcast, generating unique music can enhance engagement with customers. Branding: A distinctive audio signature can help businesses stand out in a crowded marketplace. Cost Efficiency: Hiring professional musicians or purchasing licenses can be expensive; leveraging AI-generated music may reduce these costs. However, while these tools offer exciting opportunities, they come with potential challenges that owners should consider. First, the verification process does not guarantee that every AI-generated track is free from copyright issues. As stated, users can report any content that may infringe on rights, indicating that the system is not foolproof. Moreover, complying with Google’s Terms of Service and generative AI policies is a must. Small business owners must ensure that their use of AI-generated content does not violate the intellectual property rights of others. This means being diligent in content creation while navigating the evolving AI landscape. Importantly, Lyria 3 is accessible to users aged 18 and older across multiple languages, including English and Spanish, making it versatile for a global audience. Businesses looking to leverage this tool can start experimenting right away by visiting gemini.google.com/music. In a world where content creation is vital, Google is committed to providing resources that help small businesses thrive. As AI tools advance, the potential for creativity, engagement, and efficiency in marketing will only expand. Small business owners should remain cognizant of the ongoing developments in AI technology and the implications for their own operations. To learn more about these features and how to navigate the world of AI content creation responsibly, visit the original post here. Image via Google Gemini This article, "Google Gemini Enhances Music Creation with New Audio Verification Tools" was first published on Small Business Trends View the full article

-

The American promise is one of equal opportunity, but in most of our communities today, access to the resources that enable prosperity are too far out of reach. That’s because there is one unseen factor that influences who is able to thrive and who cannot: capital. The flow of capital into communities has a dramatic effect on which kind of people can open small businesses, buy homes, and generally participate in the American Dream. Places that are already thriving are able to easily access capital. Banks see these neighborhoods as a “safe bet” and will readily support the opening of new businesses, construction of new homes, and mortgage lending. But those places that are struggling—and have been struggling—do not receive the same treatment. These are the inner-city neighborhoods, the rural communities, and the suburban areas that have been abandoned. There are some capital options for these under-resourced communities. Nonprofit and community banks offer concessionary loans, and government grants help fill gaps. For example, the Bipartisan Infrastructure Law helped drive $28.3 billion in federal grants to over 1,500 cities, according to the National League of Cities. But this is not enough. We need a different way to think about capital to drive the prosperity that has been out of reach for too many for too long. THE 3 TYPES OF CAPITAL Decades of redlining, exclusionary lending, and the uneven distribution of government funds have created entrenched divisions in American communities. Despite legal reforms, barriers to capital still persist, including higher burdens for lending placed on marginalized groups, discrimination against those groups, and capital providers simply not showing up for these places. Over 12 million Americans live in a “banking desert,” with no bank close by. These deserts are rural and urban, but also overwhelmingly suburban: two thirds of banking deserts are in suburban areas. Overcoming these barriers is not as simple as getting more money out to communities that need it. Communities need ways to not only absorb the capital, but use it. Offering money is not enough; the dollars must be combined with expertise and knowledge to help get it to the people who actually need it. At Living Cities, we have identified three different types of capital that lead to prosperity: 1. Financial capital: Funds, credit, and investment needed to start businesses, buy homes, and generally support community growth. Systemic gaps in creditworthiness, collateral requirements, and bias in financing limit the spread of financial capital. 2. Social capital: Networks of trust, mentorship, and informal connections that open doors to opportunity. Research shows social capital is strongly associated with upward mobility and improved economic outcomes, with limited networks leading to lower rates of entrepreneurship and employment. Not all communities have equal access. Decades of segregation and underinvestment have eroded social infrastructure in marginalized neighborhoods. 3. Knowledge capital: Information, skills, and know-how required to navigate business, government, and civic systems. When you have financial capital, but lack knowledge of regulatory systems, market trends, and grant opportunities, the capital can’t get to where it’s most needed and most effective. Knowledge capital is a multiplier: pairing capital with business training or legal literacy increases success rates for entrepreneurs. THE “CAPITAL EQUATION” IN ACTION Only when all three types of capital come together can the cycle of exclusion be broken. Offering only one isn’t enough. For example, small business programs that blend loans (financial), local business incubators (social), and technical training (knowledge) see higher success rates than those providing only cash infusions. Our Breaking Barriers to Business cohort is leveraging all three types of capital to create and execute projects that create jobs through hands-on small business assistance. Cities should audit procurement, zoning, and economic development policies to identify the gaps in all types of capital access, not only financial capital. Any federal and philanthropic interventions should require grantees to demonstrate not only financial investment but strategies for bridging social and knowledge capital divides. TOWARD INCLUSIVE GROWTH Equitable capital flow is about more than headline numbers. It’s about shifting the deeper patterns that determine who gets to build the future. By understanding and reshaping capital flows, cities can fire up new engines of shared prosperity. Joe Scantlebury is president and CEO of Living Cities. View the full article

-

WhatsApp is the most popular messaging app in most parts of the world, and in my decade or so of using it, I've learned a few important tips that make it a much more convenient and secure experience. I use the following WhatsApp hacks to keep my account safe, stop the app from overloading my notifications and storage, and save myself a lot of time. If you're like me, and your entire social circle is on WhatsApp, then you're absolutely going to need tips like these to stop from feeling overwhelmed. Use advanced chat privacy to block exports and Meta AIWhatsApp has end-to-end encryption, which means that the company itself cannot read the contents of your messages, but that doesn't stop recipients from easily exporting your conversations. If you don't want anyone to export your message history, make sure to enable Advanced Chat Privacy in WhatsApp. This feature needs to be enabled individually for each chat (including group chats). With Advanced Chat Privacy enabled, photos won't be automatically saved to recipients' phones, AI features will be disabled, and no one will be able to export that chat's history to their devices. Note that people can still forward your messages and take screenshots or screen recordings of them, but every little bit helps. You can enable Advanced Chat Privacy by opening any chat in WhatsApp, tapping the name of the contact or group, and going to Advanced Chat Privacy. You can lock individual chats, tooEveryone knows that you can put an app lock on WhatsApp, which means that you'll need a passcode (or biometric authentication) to view your messages whenever you open the app. A lesser known feature is that you can lock individual chats, too. This allows you to put chats with certain people or groups into a hidden folder. These hidden chats won't show up in your list of WhatsApp conversations and can only be found by searching for the name of the contact or group. Even if someone else gains access to your WhatsApp, they also won't be able to open these chats without an additional passcode or biometric authentication. To use this, open any chat in WhatsApp, tap the name of the contact or group, and enable Lock chat. Make your WhatsApp account more secure Credit: Pranay Parab There are a few easy steps you can take in the WhatsApp settings to reduce the chances of unauthorized access to your WhatsApp account. Get started by going to WhatsApp Settings > Account. First, tap on Two-step verification and enable it. WhatsApp will ask you to create a 6-digit PIN, and the next time you log in to the app on a different device, you'll be prompted to enter this PIN in addition to your other credentials. When you set up two-step verification, the app will also ask you to add an email address to help recover the PIN in case you forget it. Once you've done that, feel free to add a passkey via the same account settings page, if you wish. The final step in securing your WhatsApp account involves locking your SIM card. Go to your phone's cellular service settings and set up a SIM PIN there. This locks your SIM card or eSIM, and means that if someone tries to add your number to another device, they'll need this PIN to get in. Since WhatsApp requires your phone number for activation, this step could prevent unauthorized access to your account. Optionally, you can also add a password to your WhatsApp backups. Go to WhatsApp Settings > Chats > Chat backup > End-to-end encryption. You can either set up a passkey or a password to encrypt your backups. No one will be able to access your WhatsApp backups without this password, which will help keep your extra copies of important messages secure. Stop unknown people from adding you to groupsAs a heavy WhatsApp user, one of the biggest annoyances I used to face was people adding me to WhatsApp groups without my permission. I wasn't too bothered when my friends did this, but eventually I started getting added to random spam groups by strangers, which is when I decided to put an end to it. You can keep strangers from adding you to WhatsApp groups by going to WhatsApp Settings > Privacy > Groups and selecting My contacts. This allows only saved contacts to add you to groups. Feel free to choose My contacts except… if you want to block specific people from adding you to groups. The best WhatsApp hack for sending voice notesIf you like sending voice notes on WhatsApp, then I've got a few quick tips for you that will make your life easier. You might know that you can open any chat and hold the microphone icon to send a voice note. But did you know that if you slide this icon upwards towards the lock icon, you can let go of it and keep recording? This way, you don't have to keep holding the mic icon while recording long voice notes. You can also hit the pause button to pause the recording and come back to it later, in case there's an interruption while you're recording a voice note. Once you're done recording, you can also press the 1 button if you want your voice note to be deleted after the recipient hears it once. I'll admit, though, that I sometimes tend to ignore long voice notes. Instead, I use transcripts to quickly skim through them, and decide if they need an immediate response. Voice note transcripts are disabled by default, but you can enable them by going to WhatsApp Settings > Chats > Voice message transcripts > Manually. While you're here, also tap Transcript language and select the language that you want to see your transcripts in. Archive unwanted chats and groupsIf you're getting too many messages from certain WhatsApp chats or groups, they'll always show up at the top in the list of your chats. To get these off the main window, head to the chat list and press and hold on the chats you want to banish. Then tap Mute. To ensure that these archived chats don't reappear in the main window when you receive a new message from them, go to WhatsApp Settings > Chats and enable Keep chats archived. Reduce notification spam Credit: Pranay Parab It's really easy to get overwhelmed by notifications in WhatsApp. If you're an even moderately social person, you'll quickly find yourself receiving way more messages than you can reasonably be expected to handle. I've found that disabling WhatsApp notifications entirely works best to counter the problem, but that's not the best solution for everyone. Instead, you can try a few things to seriously reduce the amount of pings you get from WhatsApp. Go to WhatsApp Settings > Notifications and review every setting on this page. Personally, I've disabled all notifications for emoji reactions, group messages, and reminders. This way, I only get notified when individuals message me. Create chat folders to manage message overloadWhatsApp's chat folders are a great way to triage your conversations. In your chat list, press and hold on any conversation. From there, you can select either Add to Favorites or Add to list to get started. The first option adds these messages to the Favorites folder, and the second one lets you choose a custom folder name. These chat folders will appear above all your conversations, and you can quickly tap any of them to focus on specific conversations. The real hack is to reorder these folders to your liking. You can do that by holding the name on any of these chat folders and selecting Reorder lists. I've used this to prioritize messages from loved ones, my meditation group, running friends, and so on. How to stop "WhatsApp storage full" errorsUnfortunately, I know too many people whose phone storage is almost full because of WhatsApp. If you're in this situation, go to WhatsApp Settings > Storage and data > Manage storage to start the cleanup. Tap Larger than 5 MB and you'll be able to review everything that takes up a lot of storage space on your device. In the bottom-left corner, there's a button that lets you sort these files by recency or storage size. I've used this to identify lots of duplicate files and delete all but one copy of such items. You can also see a list of the chats occupying the most storage space on your device. Tap each item to manually review your files. It's pretty easy to set up a few preventative measures to stop this error, too. You can go to WhatsApp Settings > Storage and data and turn off everything under Media auto-download. Double check settings and privacyIt's important to note that if you use WhatsApp's apps on both your desktop and your phone, any settings changes you've made on one device might not sync to the other. You should review all settings to see if everything is syncing correctly. While you're double checking account details, you should also review your WhatsApp privacy settings. Go to WhatsApp Settings > Privacy, scroll to the bottom and select Privacy checkup for a quick overview. This is a step-by-step guide to enabling the most important privacy settings in WhatsApp, and is much faster than doing it manually. View the full article

-

Demand Gen marks a shift in Google Ads toward visual advertising beyond keywords and text. Relying on traditional strategies when testing it wastes budget, hurts performance, and limits opportunity. To succeed, you have to think more like a social advertiser than a search advertiser. At SMX Next, Industrious Marketing owner Jack Hepp explained why many businesses struggle with demand gen campaigns — especially in B2B and lead generation — while also sharing insights relevant to ecommerce. Understanding the Shift: From Intent to Interruption Demand Gen reflects Google’s shift from intent-first search advertising to visual, discovery-based campaigns. Instead of targeting users actively searching for your service, you reach them as they scroll through YouTube, Gmail, or Discovery feeds. This changes your approach: visual creative becomes the new keyword, replacing traditional targeting. Common misalignments in Demand Gen strategy Applying outdated search strategies can lead to failure with Demand Gen. The four main mistakes: Expecting bottom-of-funnel CPAs from mid-funnel traffic. Using overly broad, “spray and pray” targeting. Running bland, generic creative. Not knowing how to optimize without negative keywords. Success requires a social advertising mindset. Campaign structure: Understanding the hierarchy Demand Gen uses a two-level structure. Campaign-level settings control broad parameters like bidding strategy, conversion goals, and device targeting. Ad group–level settings control audiences, locations, and channels. Each ad group learns independently—insights don’t transfer—allowing precise audience segmentation with tailored creative. Creating interruption-based creative You must stop their scroll within 3-4 seconds. Your creative must capture attention immediately, speak to a specific pain point, and present your solution. Unlike search ads — where users are actively looking for you — Demand Gen interrupts browsing, so your message must be instantly compelling and problem-focused. Aligning visuals to the customer journey Match your offer to audience readiness. Cold audiences need educational content like free guides or diagnostic tools. Warm audiences respond to case studies, webinars, and comparison tools. Hot audiences are ready for demos and direct purchase offers. Misaligning them — like pushing demos to cold audiences — guarantees failure from the start. The power of problem-focused creative Generic ads with stock photos and basic headlines get scrolled past. Winning creative uses bold headlines, striking visuals, and problem-focused messaging. For example, “43% of cyberattacks target small businesses” speaks to a specific pain point, making the ad stand out and prompting engagement instead of a scroll. Bidding and budget strategies Demand Gen uses campaign goals rather than traditional bidding strategies: conversion-focused, click-focused, or conversion–value–focused. Aim for 50+ conversions per month and budget 10–15x your target CPA to build enough data. For click-based bidding, set budget based on desired traffic volume and target CPC. Demand Gen is highly data-reliant, so hitting these thresholds is critical to performance. Can Demand Gen work with small budgets? Yes, with strategic planning. Focus on mid- or upper-funnel audiences and optimize for MQLs instead of bottom-funnel conversions. This helps you reach 50+ monthly conversions for data density, even with smaller budgets. Align your goals, targeting, and budget to generate enough conversion data. Building the right audience Avoid two extremes: Audiences that are too broad (billions of impressions) where Google can’t identify your target. Audiences too narrow (a few thousand impressions) where you can’t build data density. The sweet spot: start with custom segments based on search terms or competitor websites, then layer in lookalike segments and strategic first-party data. Avoid optimized targeting at first — it works best to expand already successful campaigns. The role of creative in targeting Your creative shapes who Google targets. The people who engage with your ads teach Google who to show them to next. Performance peaks when your creative speaks to your ideal customer profile. Align messaging to the buyer’s stage — cold audiences need different messaging than hot prospects. Strategic exclusions Use exclusions surgically, not broadly. It’s tempting to exclude like negative keywords, but over-excluding shrinks your audience too much. Focus only on clear non-converters (e.g., specific age groups, locations, or audiences you know won’t respond). Give Google room to find engaged users within your parameters, rather than narrowing to the point of ineffectiveness. Optimization: Where to focus Without negative keywords, optimize through three levers: creative, audience, and offer. Test multiple formats (video, image, carousel) and styles (UGC, testimonials, problem-focused messaging). Continuously refine what works with new hooks and data points. Test offers to match audience readiness — cold audiences need educational content, while hot audiences need direct CTAs. Prioritize post-click optimization: improve landing pages, strengthen tracking with CRM integration, and ensure clean data feeds Google’s learning. Real-world case study A telecommunications company targeting B2B managed IT services drove strong results by aligning all three elements. Offer: An interactive quiz showing businesses how managed IT could reduce costs. Targeting: Custom segments based on proven search terms and competitor website visitors. Creative: Problem-focused messaging about cybersecurity threats to small businesses. Results: $10 cost per MQL. 3.8% conversion rate. 40% of quiz takers became SQLs. 20% increase in total SQLs. Key takeaways As you plan your next campaign: Match your creative to your customer and their stage in the journey. Target the right audience at the right point in that journey. Test and optimize creative and offers to find what resonates and drives action. View the full article

-

Be sure to provide details. By Ed Mendlowitz Tax Season Opportunity Guide Go PRO for members-only access to more Edward Mendlowitz. View the full article

-

Be sure to provide details. By Ed Mendlowitz Tax Season Opportunity Guide Go PRO for members-only access to more Edward Mendlowitz. View the full article

-

Authoritarian acolytes will tell you that, to be strong, a country must “demonstrate force.” White House advisor Stephen Miller recently put that worldview plainly on CNN, arguing that “the real world…is governed by strength…by force…by power”—a claim belied, as it were, by history. America did not become a superpower primarily by proving it could dominate. It became a superpower by proving it could partner. After World War II, the United States stood unrivaled militarily. Yet it did not rely on force alone to secure its position. Instead, it invested in rebuilding a shattered world. The Marshall Plan was not charity—it was a strategy, linking economic recovery with political stability and turning war-torn nations into long-term allies. By helping others prosper, the U.S. increased its own security and economic future. That is soft power at work. Dwight Eisenhower, a five-star general, advanced the idea that diplomacy is not the sole province of governments, and that when people know you, they are less likely to fear you. And when they trust you, they are more likely to collaborate with you. John F. Kennedy carried that logic forward with the Peace Corps. The program sent a clear signal that American power included service, partnership, and humility. In a Cold War offering competing models to aspire to, that mattered, and it continues to matter today. THE ROLE OF SOFT POWER Soft power was never intended to be solely a government project. After the collapse of the Soviet Union, the United States again faced a pivotal choice: declare victory and walk away or support the hard work of transition. Out of that moment emerged citizen diplomacy initiatives like what later became Pyxera Global—formed at the behest of the George H.W. Bush White House that called for a “Citizens Democracy Corps” to mobilize private-sector volunteer expertise to help planned-economy societies build market economies and democratic institutions. Alongside these efforts, agencies like USAID institutionalized development as a pillar of U.S. foreign policy—investing for decades in health, education, food security, and economic growth as tools of stability and influence. That model—public purpose paired with private capability—has always been central to America’s soft power. There are certainly many situations and geographies where U.S. engagement fell woefully short. Still, taken together, these efforts point to a simple conclusion: America’s influence has been strongest when it was most useful—not most intimidating. Soft power was never a weakness—it was leverage. That history matters now. When the U.S. government pulls back from development, diplomacy, and partnership, the vacuum does not remain empty. Other forces are surely eager to fill it with transactional relationships, debt dependence, and authoritarian influence. If Washington is narrowing its role now, the private sector faces a choice of its own. It can retreat inward, treating global instability as someone else’s problem. Or it can recognize a simple truth: A stable world is a prerequisite for sustainable business. Soft power is not philanthropy. It is long-term risk management. HOW BUSINESS CAN STEP INTO THE GAP None of the following actions is a substitute for government. But they represent a sampling of ways that global business now has the opportunity—and the capacity—to step into the vacuum. Normalize board service as leadership—not a side project. Encouraging executives to serve on nonprofit and civic boards strengthens institutions at a time of severe resource constraints, when we need them to function well. It also builds empathy, governance skills, and real-world decision-making capacity, qualities companies claim to value in leaders. Scale skills-based volunteering. Finance, compliance, cybersecurity, HR, and logistics are some of the skills that many public and nonprofit institutions cannot easily access. Deploying them fills a dire resource gap while meeting employee demand for purpose-driven work that uses real expertise. Double down on supply-chain resilience as a form of stability. Diversifying suppliers, investing in transparency, and ensuring local equity reduce exposure to disruption and coercion. Resilient supply chains are not just good business—they help anchor opportunity and stability in the places where companies operate. Expand community-driven initiatives where companies operate. Corporate success cannot sustainably outpace community well-being. Health, nutrition, education pipelines, workforce training, and local economic development are not public relations gestures—they are investments in human capital, social cohesion, and long-term operational continuity. THE POWER OF PARTNERING Taken together, and implemented at scale, these actions underscore a simple truth: strength is not only the ability to strike—it is the ability to attract, rebuild, and partner. And if Washington continues to pull back from soft power, global business can advance something new, durable, and worth trusting. Deirdre White is the CEO of Pyxera Global. View the full article

-

Move past the lip service. By Domenick J. Esposito 8 Steps to Great Go PRO for members-only access to more Dom Esposito. View the full article

-

Move past the lip service. By Domenick J. Esposito 8 Steps to Great Go PRO for members-only access to more Dom Esposito. View the full article

-

Jose Alejandro Zamora Yrala’s ‘utterly inexcusable’ actions put 60,000 suspect parts into the global aviation supply chainView the full article

-

Military intelligence followed a ‘romantic partner’ of cartel leader Nemesio ‘El Mencho’ Oseguera before deadly shootoutView the full article

-

The Ford Mustang Mach-E cruises down a London road choked with traffic, using its onboard AI system to avoid jaywalkers and cyclists, and navigate roadwork as it drives to its destination. The autonomous vehicle from British startup Wayve Technologies is on a test run ahead of the U.K. government’s robotaxi trials set to launch in the spring. Tech companies including U.S. company Waymo and China’s Baidu also plan to take part in the pilot program, making London the latest arena in the global robotaxi competition. While self-driving cabs aren’t new, London’s ancient road layout and busy streetscapes could pose special challenges for the technology. There’s also skepticism from London’s famed black cab drivers, who must pass a grueling training course known as “The Knowledge,” which requires memorizing hundreds of routes and takes years to complete. They’ve previously opposed technology that’s disrupted their industry, and protested the arrival of Uber. Self-driving taxis are “a solution looking for a problem,” said Steven McNamara, general secretary of the Licensed Taxi Drivers’ Association, which represents black cabbies. He doubts that robotaxis would have any advantage on London’s road network, which is laid out in a convoluted spiderweb that dates back to Roman times — unlike the grid layout in American cities like San Francisco and Phoenix where Waymo operates. The British capital is notorious for being one of the world’s most congested cities and its streets are already clogged with other modes of transport, including private cars, buses, motor scooters, bicycles and electric rental bikes. McNamara and many others have noted that robotaxis face another challenge from pedestrians crossing the streets. While jaywalking is illegal in the United States and many other countries, it’s not an offense in Britain. “It’s virtually impossible to drive anywhere (in London) without somebody walking in front of you,” McNamara said. In London, with a population of nearly 10 million, he wondered “how these cars are going to deal with those volumes of people?” The robotaxi companies say there’s room for the new technology. “I think Londoners are going to love autonomous driving. It’s going to be another choice alongside the Tube, cycling, walking, “said Wayve CEO Alex Kendall in a recent interview at the company’s workshop. Wayve is teaming up with Uber for the taxi trials, which are part of Britain’s move to adopt national regulations for self-driving vehicles. The nation is seeking to position itself as a world leader in the technology. Chinese tech company Baidu is also teaming up with Uber, as well as its ride-hailing rival Lyft, to operate its Apollo Go autonomous vehicle service in the London pilot. Waymo, owned by Google parent Alphabet, will also take part and plans to launch a London passenger service by the third quarter of 2026, company representatives told reporters last month. Waymo officials sought to ease concerns that the company would suddenly flood London streets with robotaxis, noting that it has operated 1,000 total vehicles in San Francisco since going into full service in 2024. “We’re not here to replace anyone,” Waymo spokesman Ethan Teicher said. “We’re here to add another option for people who will choose to take black cabs or other modes of transportation when it suits them and choose to take Waymo, when it makes sense.” Waymo’s self-driving Jaguar I-Pace sedans have been spotted doing test runs around London. Wayve’s Ford Mustang Mach-E vehicles have also been doing road tests with human backup drivers sitting behind the wheel, ready to intervene if needed. On a recent demo ride for The Associated Press, Wayve’s Ford steered automatically through a three-mile (five kilometer) loop in North London without any problems. Cruising down a straight and open stretch of road, the car maintained a steady pace of 19 miles (30 kilometers) per hour, a tick under the speed limit. A traffic light changed as the car approached, forcing it to brake firmly and lightly jolting the passengers forward — the only moment that the driving was less than smooth. Kendall said Wayve takes a different approach from traditional self-driving technology. It doesn’t rely on “high definition” maps and “hand-coded” safety systems rules written by programmers anticipating every scenario. Instead, it uses an AI trained on millions of hours of data gathered by its cars to learn and understand how the world works. “This is the key thing for self-driving, because every time you drive on the road, you’re going to experience something different,” Kendall said. “You can’t rely on a self-driving car being told how to behave in every scenario it encounters.” He said Wayve is positioning itself as a technology company providing hardware and software that can be added to any vehicle to make it autonomous. It signed a deal with Nissan in December to build self-driving cars that will go on sale in Japan and North America by 2027. Kendall wouldn’t reveal any more specific details about the robotaxi service it will operate in collaboration with Uber, such as pricing. Waymo, which has its own app to hail rides, will have “competitive” prices and fares will be in line with the market, officials said last month, while adding that it is often able to “demand more premium pricing.” Experts say there’s a role for robotaxis in Britain, but it might be a niche one. They’re best poised to fill gaps in Britain’s public transport network, such as serving villages that have lost bus services connecting them to bigger towns and cities because of budget cuts, said Kevin Vincent, director of the Centre for Connected and Autonomous Automotive Research at Coventry University. There will still be demand for human drivers, especially from out-of-town visitors and tourists, he said. If you find a “cab driver who knows the area, you can ask him questions. You feel confident and comfortable you’re going where you need to go,” which is a service that won’t be easily replaced in the short term, Vincent said. Self-driving taxis can’t replicate the human touch, said Frank O’Beirne, who has been driving black cabs for 14 years. For example, one of his recent fares was a pair of blind passengers going to touristy Leicester Square. He ended up parking at a cab rank and walking them across the street to their destination, a Chinese restaurant that turned out to be in the basement of a casino. “They would never have found that, ever, (on their own),” said O’Beirne. “There’s nothing like us. I can’t see the space where autonomous taxis can operate, really.” —Kelvin Chan, AP Business Writer View the full article

-

Private capital groups also hit as traders digest fallout from president The President’s 15% global tariffView the full article

-

For the last several years, enterprises have treated AI as something to test. A pilot here, a proof of concept there. That era is ending. According to new global DeepL research, a survey of 5,000 global executives on the impact of AI agents reshaping business, 69% expect AI agents to fundamentally change how their companies operate in 2026. Nearly half anticipate major transformation, while another quarter say that change is already underway. This moment didn’t arrive overnight. While 2025 was the year agentic AI moved from theory to application, enterprises are making the shift structural this year. Leaders are no longer asking whether AI works but rather deciding where AI agents belong inside their operating model. As tools mature and agentic systems become capable of coordinating work across functions, AI agents are unlocking new opportunities—not just automating tasks. By eliminating manual coordination, AI agents enable organizations to move faster and smarter, enabling the creativity, problem-solving depth, and judgment that turn velocity into measurable value. Yet, when it comes to scaling agents and validating their investment, most organizations remain stuck in pilot mode. McKinsey reports that while 62% of companies are experimenting with agents, only 10% are scaling them across a single function, and just 32% of leaders report an impact on EBIT at the enterprise level. The gap between early adopters and those who hold out will widen in 2026—not because of trial and error, but execution. Three shifts will define this gap—how enterprises automate core operations, deploy AI for growth, and build the communication infrastructure agents require. AUTOMATE THE CORE AI agents are no longer confined to experimentation or pilots. Enterprises are deploying them into operational workflows like processing returns in customer service, investigating customer complaints, automating approvals and ticketing, supporting prospect and competitor research in sales and marketing, and optimizing working capital in finance. What’s changing is continuity. Instead of accelerating individual tasks, organizations are increasingly making agents responsible for managing handoffs between them—reducing friction. Looking at AI agent adoption more broadly, DeepL’s research shows global executives cite proven ROI and efficiency (22%), workforce adaptability (18%), and enterprise readiness (18%) as the primary reasons they feel confident expanding agent deployment. Results, not optimism, are driving this shift. At the same time, known barriers are beginning to soften. Cost (16%), workforce preparedness (13%), and technology maturity (12%) remain challenges, but enterprises are actively addressing them as they gain experience operating agents in production environments. The real risk now is inaction. Organizations that fail to identify which workflows should be automated first keep valuable talent focused on low-leverage work—while competitors redesign operations around intelligent systems. Customer service offers a clear example. Companies like Perk are deploying AI agents to take on routine operational work in customer support, while human agents focus on complex, relationship-driven scenarios. As Tom Davis, senior director of operational excellence at Perk, notes: “When we’ve got travelers stuck in airports, we want our humans focused on those moments—and in the background, a machine of AI handling the grunt work.” That division allows human agents to focus on high-stakes relationship work while AI agents manage operational tasks at scale. AI AS A GROWTH ENGINE AI is no longer confined to cost reduction. It’s becoming a driver of growth. The broader AI landscape shows strong momentum: 67% of executives reported measurable impact from AI initiatives in 2025, and 52% expect AI to contribute more to company growth than any other technology in 2026. Enterprises seeing the strongest returns are applying AI across revenue-generating functions—customer service, marketing, sales, finance, legal, HR, and IT support—rather than limiting it to back-office automation. The competitive advantage comes from scale and integration, not just isolated use cases. But the real gain isn’t just efficiency—it’s faster, higher-quality decision making. As b2ventures noted in their work with AI agents, the technology helps them make higher-quality investment decisions faster because agents excel at evaluating companies and surfacing insights that inform critical choices. According to DeepL’s research, leaders in the UK (80%), Germany (78%), and the U.S. (71%) are seeing measurable performance gains from AI initiatives. This underscores that execution and organizational readiness are just as important as access to technology when it comes to turning AI into a strategic advantage. Ignoring AI in growth-critical areas is no longer conservative. It’s a strategic risk, particularly in sectors where margins and customer expectations are shifting fast. LANGUAGE AND VOICE AI As AI agents move deeper into enterprise workflows, they’re changing how people interact with software itself. Instead of clicking through dashboards or submitting forms, employees increasingly instruct systems through natural language. In an agent-driven operating model, language becomes the primary user interface. This is the mechanism through which work gets done. That shift raises the stakes for fluency and accuracy. When language is the interface, a mistranslated prompt or misunderstood instruction doesn’t just slow down communication; it can derail an entire workflow. For enterprises scaling agents across teams and regions, language precision becomes a requirement, not a nice-to-have. This is reflected in enterprise priorities where 64% of companies plan to increase investment in language AI in 2026, while organizations expect adoption of real-time voice translation to rise to 54%. These investments aren’t standalone initiatives. They are foundational to making AI agents reliable, scalable, and effective. EXECUTION, NOT EXPERIMENTATION This year, the organizations experiencing the biggest impacts will stop experimenting with AI and start embedding AI agents into core operations and applying them across growth-critical functions. By turning AI into a strategic advantage, these companies will streamline operations, make better decisions, and unlock measurable business value. Those who delay will watch the gap grow as early adopters accelerate ahead. Jarek Kutylowski is the CEO and founder of DeepL. View the full article

-