All Activity

- Past hour

-

Banks must plan to support decentralized finance without disturbing their existing businesses. That's easier said than done. View the full article

-

In a stark reminder of the high stakes and stringent oversight surrounding COVID-19 relief funding, Gurjeet Bath, a Fresno businessman, has been sentenced to 14 months in prison for fraudulently obtaining over $825,000 through the Paycheck Protection Program (PPP). This case stands as a cautionary tale for small business owners navigating the complexities of government assistance during a crisis. The PPP was designed to provide essential financial support to small businesses struggling to keep employees on payroll. However, Bath exploited this federal program by falsifying employee records and inflating wage data—an act that fueled not only personal gain but also undermined the integrity of a lifeline meant for legitimate struggling enterprises. U.S. Attorney Eric Grant highlighted the gravity of Bath’s actions, stating, “During a time when legitimate businesses were struggling to survive, this defendant chose to exploit a program designed to keep workers employed.” Bath’s fraudulent actions involved applying for and receiving three PPP loans totaling more than $1 million for his trucking businesses, G.S. Bath Inc. and Complete Transportation Solutions. By fabricating records, he misrepresented the number of employees and their wages to secure the funds, ultimately diverting the money into purchasing agricultural land. The FBI’s investigation, in collaboration with the SBA Office of Inspector General, underscores the federal commitment to rooting out fraud in these vital programs. The ramifications of this case reach beyond Bath’s prison sentence. For small business owners, it serves as a crucial reminder to adhere strictly to eligibility requirements and maintain accurate documentation. The consequences of misinformation can be severe, ranging from fines to jail time and loss of access to future funding opportunities. Practical applications of this case’s lessons are manifold. Business owners seeking to apply for government assistance must understand that the relief funds come with strict regulations. Accurate record-keeping, honest representation of employee data, and transparent financial practices are essential to both secure funding and build long-term trust with financial institutions and government agencies. Additionally, the ongoing scrutiny by federal agencies should raise awareness about the importance of compliance for small businesses. This vigilance aims not only to prevent misuse but to ensure that the relief reaches those genuinely in need. The emphasis on accountability is reflected in the significant penalties imposed on fraudsters. Bath’s case stands as a warning: those who attempt to exploit programs designed for community support risk severe legal repercussions. While the PPP has provided necessary funding for numerous small enterprises, recent high-profile fraud cases indicate a tightening of scrutiny by government authorities. Business owners may want to brace themselves for increased audits and reviews of loan applications, especially as federal agencies continue to enhance oversight mechanisms. In light of these developments, small business owners are encouraged to seek out legal and financial advice before applying for relief programs. Ensuring compliance not only safeguards against legal troubles but can also foster healthier relationships with banks and lenders for future opportunities. As U.S. Attorney Grant aptly noted, Bath’s actions have irrevocably harmed the collective trust of the community in these essential programs. “He has since pleaded guilty and repaid the stolen funds, but that does not erase the harm caused.” This statement should resonate deeply within the small business community, highlighting the dual necessity of taking full advantage of available resources while eschewing any shortcuts that could lead to devastating consequences. For further details on the case, the full press release can be found here. Image via Google Gemini This article, "Fresno Man Sentenced for Stealing $825K in Pandemic Relief Funds" was first published on Small Business Trends View the full article

-

Google's Gary Illyes and Martin Splitt discuss page weight growth, the 15MB crawl limit, and whether structured data is adding bloat to web pages. The post Google: Pages Are Getting Larger & It Still Matters appeared first on Search Engine Journal. View the full article

-

We may earn a commission from links on this page. Deal pricing and availability subject to change after time of publication. With so many options on the market, it can be tough to differentiate between vacuum robots and mop hybrids. But if you’re on a budget, one major factor to consider is whether it has a roller mop. A roller mop cleans hard floors better by preventing dirty water from spreading and is more effective at removing heavy-duty messes, similar to wiping up a mess with a wet towel. The new Eufy Omni C28 is the “most budget-friendly roller mop robot vacuum,” according to Mashable, and right now it's 38% off for the Amazon Big Spring Sale, bringing it to a record-low price of $499.99 (originally $799.99). Eufy Omni C28 Robot Vacuum and Mop $799.99 at Amazon Get Deal Get Deal $799.99 at Amazon Along with being surprisingly affordable for its extra-long roller design, the C28 is a compact choice for apartments and smaller homes with a dock that takes up less space than other auto-washing and drying hybrid cleaners. The one drawback is the 15,000 Pa suction power, which, on the surface, appears underwhelming compared to higher-powered options costing four figures. Despite this, professional and consumer reviews consistently state that the C28 leaves floors sparkling and dust-free, especially when the wet, pressurized roller mop does double duty. It also performs well in smart mapping, with setup taking just a couple of minutes. While the 10.7-inch roller mop (which self-cleans with clean water nine times a second) is the main standout feature, the robot vacuum’s 4.5-inch height may not be slim enough to fit under some dishwashers and low-clearance furniture or cabinets. And despite 15,000 Pa suction, it can be a little noisy, particularly during the auto-empty process. It can cross thresholds up to 20 mm, and the roller mop lifts up to 10.8 mm when carpeting is detected. The five-in-one base station keeps the C28 hands-free for up to 75 days, handling mop cleaning, dust removal, water tank refilling, wastewater collection, and hot-air drying, which runs a bit faster than competitors thanks to a four-air duct system. If you want a genuinely hands-free setup with an effective self-cleaning roller mop, the mid-range Eufy Omni C28 robot vacuum and mop is a solid option, offering great value for near-high-end features at less than half the price, especially during the Amazon Big Spring Sale, when it’s at its lowest price ever. Our Best Editor-Vetted Amazon Big Spring Sale Deals Right Now Apple AirPods Pro 3 Noise Cancelling Heart Rate Wireless Earbuds — $199.00 (List Price $249.00) Apple iPad 11" 128GB A16 WiFi Tablet (Blue, 2025) — $299.00 (List Price $349.00) Samsung Galaxy Tab A11+ 128GB Wi-Fi 11" Tablet (Gray) — $202.00 (List Price $249.99) Sony WH1000XM6- Best Wireless Noise Canceling Headphones — $398.00 (List Price $459.99) Apple Watch Series 11 (GPS, 42mm, S/M Black Sport Band) — $299.00 (List Price $399.00) Blink Video Doorbell Wireless (Newest Model) + Sync Module Core — $35.99 (List Price $69.99) Fire TV Stick 4K Max Streaming Player With Remote — $34.99 (List Price $59.99) Amazon Kindle Colorsoft 16GB 7" eReader (Black) — $169.99 (List Price $249.99) Deals are selected by our commerce team View the full article

-

BEST practices are often viewed as the key to success in the business world. Certifications to prove practitioners are competent in accordance with a best practice make sense at the surface. However, they’ve become psychological cover that create mediocre results at best. It’s reassuring to be able to point at the protocol and say, “I followed the best practice. It’s not my fault.” Take project management, for example. Most project managers I’ve met (my younger self included) come from technical backgrounds who love best practices. I genuinely thought project management was about following the best practice and forcing people to follow my plan. Spoiler alert: That didn’t work. With today’s disruption and volatility, “business as usual” means little when there’s no “usual” anywhere in sight. Although Disruption and Volatility would make great names for a law firm, they require an adaptive approach to ensure survival and sustainability. Best practices bring a false measure of certainty for keeping threats at bay. However, they’re largely irrelevant as they’re developed by looking in the rearview mirror according to what worked under the conditions at that time. The solution is enhancing critical thinking to navigate complexity in real time. These days, to be successful, you need to be adaptable. This requires developing the critical thinking skills to solve the unique challenges your situation presents. To do so, follow these tips: 1. Don’t Mistake Motion for Mastery Attending endless meetings, always agreeing with leadership, escalating decisions, and “checking the boxes” that show you observed the best practice are all compliance-based behavior. You feel like you’re providing value but are really providing only a superficial benefit. Busy work consumes energy. It moves the needle little in terms of value delivered. This puts your organization and yourself at risk. Mastery comes from thoughtful distillation to what matters. Condense your work down to its essence — the 1 percent that really moves the needle. This involves having the important coaching conversation to shift the thinking of a team member, sharing the contrarian viewpoint that no one else sees, or carving out time for learning and growth to build new thinking. These are all leverage plays that return far more over time than they consume. 2. Understand That Best Practices Become So in Hindsight I started my career in engineering and realized early on that the work I did was a “good enough” approximation of the real-world physics my designs operated in. This allowed me to build things that consistently worked at a reasonable cost. Best practices are an approximation of what works in the real world. However, they’re only a snapshot of what worked at one point in time in the past. The business environment evolves rapidly at an ever-increasing rate of change. Best practices are backward-looking and largely irrelevant to the modern environment in which we try to apply them. This is why we talk of “better” practices and not “best” practices. You should always be getting better in the system in which you operate. Once you think you’ve arrived at the “best,” there’s no point to continue getting better. That leads to complacency. 3. Realize That Value Lies Beneath the Surface Understand what the organization you work within truly values. I often find when working with clients, whatever leadership thinks provides value in terms of outcomes are in tension with what leaders actually show they value day to day. For example, they may say the organization needs to be the top innovator in its industry globally. Then, leaders micromanage, reinforce compliance, and criticize mistakes. You can’t get to innovation if you value compliance, shame risk-taking, and make it intimidating for people to pursue efforts that might come up short. Success comes to those who are brave and can push back against the behavioral norms despite the daily rhetoric. Speak up when it feels uncomfortable. Have one high-leverage conversation tomorrow that you’ve been putting off. I rarely meet leaders who don’t value results when you show them you can achieve them. People who can do this write their own ticket. That means you need to be ready for some social discomfort on your journey to delivering the results your organization truly wants. Best practices are misaligned with the needs of the modern business environment because they’re rooted in yesterday’s logic and provide convenient psychological cover. In a world that previously rewarded compliance, many professionals were never required to develop strong critical thinking. That world has shifted. Leaders must move beyond the comfort those practices once provided and focus instead on the high leverage work that creates real outcomes. The willingness to think, question, and adapt is now what separates compliance from true leadership. * * * Kursten Faller a leadership and project management advisor with more than 25 years of experience helping organizations navigate complexity, change, and transformation. Founder of Midgard, a consulting firm, he has worked with executives and teams across sectors, offering executive coaching, leadership development, and advisory services. Alan Weiss is a globally recognized consultant, speaker, and author, renowned for his expertise in organizational development and personal growth. As the founder of Summit Consulting Group, Inc., he has advised over 500 leading organizations worldwide, including Merck, Hewlett-Packard, GE, Mercedes-Benz, and the Federal Reserve. The Hidden Project Drivers: Building Behavior that Drives Success (Business Expert Press, April 3, 2026), shares how to deliver outcomes successfully by inspiring rather than controlling. * * * Follow us on Instagram and X for additional leadership and personal development ideas. * * * View the full article

-

Gen Z founders may not have spent as much time in the workplace when they started their companies as some older founders. But in some ways, that gives them unique insight that can be valuable for leaders. For Katie Diasti and Anam Lakhani, a disconnect from the work they were doing as interns has helped to shape their leadership style. Specifically, those experiences inspired them to ensure that all of their team members feel a sense of both ownership and impact for the work they’re doing. “I remember interning and creating a whole deck and making a whole presentation, but never being allowed to be in the room that the presentation was in,” recalled Diasti, founder and CEO of Viv Period Care, speaking at the Fast Company Grill at SXSW. “Now, as we have team members creating something, I want them to see the holistic approach—I want them to see every metric of the business and the goal, because that actually motivates them to feel that ownership and that trust.” Lakhani, meanwhile, was inspired to co-found the Alinea Invest app during college to make investing more accessible to her generation—and likewise, she drew on her experience interning in investment banking on Wall Street to ensure her company’s work felt both meaningful and impactful. “One thing I knew when starting my company is I wanted every day to feel like you were moving the company forward, that you were having an impact on the user experience, that you were driving something forward,” she said. Balancing what they know—and don’t know Being a disruptive founder—and especially at a young age—requires a balancing act of sorts. On the one hand, young founders don’t have the “baggage” of longheld expectations about how things are done. But they must also have good mentors, and a sense of humility to navigate managing people who are several decades older, said Liam Ryan, CEO of Streetleaf, which designs, installs, and maintains solar streetlights throughout the U.S. And while it’s important internally to foster a sense that everyone in the company is on the same team, interacting with outside stakeholders requires being confident in the expertise you as a leader have acquired when encountering outdated stigmas, Ryan added. “When we first started doing this like five, six, years ago, we’d come into the room and they’d roll their eyes like, ‘The Gen Z solar people are here,’” Ryan recalled. “But when we showed that our products are not only more economical, but also sustainable, it got more people listening to what we’re doing, not just one part of the equation.” View the full article

-

A bug in Google Ads Editor is causing structured snippet extensions copied between accounts to remain unintentionally linked. When advertisers change the language in one account, it can automatically update the same extension in another. Why we care. This bug creates hidden inconsistencies for advertisers managing multi-market campaigns, especially when different languages are required across accounts. What advertisers are seeing. The issue surfaced while managing Czech and Slovak e-commerce accounts by digital marketer Marcin Wsół. Changing the snippet language in one account triggered the same change in the other. The extensions appear separate but behave as if synced. Zoom in. Using the Google Ads web interface can temporarily correct the issue, however, further edits in Editor may cause the language settings to toggle again. Also. The bug isn’t limited to cross-account use. PPC News Feed founder, Hana Kobzová, founder that copying structured snippets within the same account can also lead to incorrect language settings after edits. Between the lines. Advertisers relying on bulk edits in Editor may unknowingly overwrite localization settings, leading to mismatched messaging across markets. Bottom line. Until fixed, advertisers should double-check structured snippet languages after copying or editing in Google Ads Editor—especially when working across accounts or regions. First seen. This error was first picked up by Wsół, which was picked up by PPC News Feed. View the full article

- Today

-

At SXSW, the future of music and culture is always on display. From packed showcases to surprise sets and branded activations, the festival offers a glimpse of what’s next. But behind every viral moment and seamless event is a workforce SXSW rarely acknowledges: freelancers. They are the sound engineers running live sets, the videographers capturing performances that travel the world, the stage managers keeping showcases on schedule, the photographers, producers, and crew who turn ideas into experiences. SXSW depends on them. I saw this up close at a Latino Victory Fund event during the festival, where filmmaker Robert Rodriguez took the stage to celebrate Los Lobos — an iconic band that has shaped generations of music and culture — and the documentary premiere, Native Sons. It was the kind of moment SXSW is known for: electric, cross-generational, deeply rooted in place. And like every showcase and panel, it was powered by freelancers—producers, technicians, videographers, and crews whose labor makes these moments possible, and who too often remain invisible. Independent workers now make up a massive share of the U.S. workforce, with more than 60 million Americans freelancing today—nearly two in five workers—up from roughly one in three pre-pandemic.¹ The “future of work” SXSW celebrates isn’t something on the horizon. It’s already here. And yet, the conditions under which many of these workers operate remain anything but forward-looking. And the stakes are not abstract. According to a recent Freelancers Union survey, 82% of freelancers say healthcare access influences how they vote—a powerful signal that economic insecurity in this sector is shaping political behavior in real time. With the world’s eyes on Texas during a pivotal election year, Congressman Greg Casar figured prominently at this year’s festival. Speaking at Axios House, he made a clear case that Democrats must prove they are delivering for working people —especially Latino workers — are driving much of the country’s economic growth. But at SXSW, that question isn’t abstract. It’s embodied by the freelancers powering the festival itself—workers whose economic realities too often fall outside the protections policymakers claim to champion. We cannot continue to celebrate the future of work on stage while ignoring the conditions of the people doing that work behind the scenes. In New York, we passed the Freelance Isn’t Free Act, guaranteeing freelancers the right to a written contract and timely payment. It’s simple: if you do the work, you should get paid—on time and in full. It works. But step outside New York, including to places like Texas where SXSW takes place, and those protections disappear. That gap matters—not just for freelancers, but for the future SXSW claims to represent, and a future we are not waiting for. Millions of Americans are already building careers as independent workers across the industries that power our cultural and economic life. The question isn’t whether freelance work will grow. It’s whether we will build an economy that respects it. Festivals like SXSW have an opportunity—and a responsibility—to lead. That means more than putting creators on stage. It means committing to fair standards behind the scenes: contracts, timely payment, and basic protections for the people who make the entire ecosystem possible. fIt also means policymakers must catch up. States across the country should adopt and expand laws like Freelance Isn’t Free so that a worker’s rights don’t end at a city or state line. If SXSW is where the future comes into focus, it should also be where we decide what kind of future we’re building—one where creativity is celebrated and protected, and where the workers behind the scenes are finally recognized as essential to the story. Congressman Greg Casar speaking at Axios House1 Upwork Research Institute, Freelance Forward 2023: The Growing Freelance Workforce in the United States, 2023, https://www.upwork.com/research/freelance-forward-2023-research-report; see also Gig Economy Data Hub (Rockefeller Institute of Government), “Freelance Forward Data Sources,” https://gigeconomydata.org/research/data-sources/freelance-forward.html. View the full article

-

At SXSW, the future of music and culture is always on display. From packed showcases to surprise sets and branded activations, the festival offers a glimpse of what’s next. But behind every viral moment and seamless event is a workforce SXSW rarely acknowledges: freelancers. They are the sound engineers running live sets, the videographers capturing performances that travel the world, the stage managers keeping showcases on schedule, the photographers, producers, and crew who turn ideas into experiences. SXSW depends on them. I saw this up close at a Latino Victory Fund event during the festival, where filmmaker Robert Rodriguez took the stage to celebrate Los Lobos — an iconic band that has shaped generations of music and culture — and the documentary premiere, Native Sons. It was the kind of moment SXSW is known for: electric, cross-generational, deeply rooted in place. And like every showcase and panel, it was powered by freelancers—producers, technicians, videographers, and crews whose labor makes these moments possible, and who too often remain invisible. Independent workers now make up a massive share of the U.S. workforce, with more than 60 million Americans freelancing today—nearly two in five workers—up from roughly one in three pre-pandemic.¹ The “future of work” SXSW celebrates isn’t something on the horizon. It’s already here. And yet, the conditions under which many of these workers operate remain anything but forward-looking. And the stakes are not abstract. According to a recent Freelancers Union survey, 82% of freelancers say healthcare access influences how they vote—a powerful signal that economic insecurity in this sector is shaping political behavior in real time. With the world’s eyes on Texas during a pivotal election year, Congressman Greg Casar figured prominently at this year’s festival. Speaking at Axios House, he made a clear case that Democrats must prove they are delivering for working people —especially Latino workers — are driving much of the country’s economic growth. But at SXSW, that question isn’t abstract. It’s embodied by the freelancers powering the festival itself—workers whose economic realities too often fall outside the protections policymakers claim to champion. We cannot continue to celebrate the future of work on stage while ignoring the conditions of the people doing that work behind the scenes. In New York, we passed the Freelance Isn’t Free Act, guaranteeing freelancers the right to a written contract and timely payment. It’s simple: if you do the work, you should get paid—on time and in full. It works. But step outside New York, including to places like Texas where SXSW takes place, and those protections disappear. That gap matters—not just for freelancers, but for the future SXSW claims to represent, and a future we are not waiting for. Millions of Americans are already building careers as independent workers across the industries that power our cultural and economic life. The question isn’t whether freelance work will grow. It’s whether we will build an economy that respects it. Festivals like SXSW have an opportunity—and a responsibility—to lead. That means more than putting creators on stage. It means committing to fair standards behind the scenes: contracts, timely payment, and basic protections for the people who make the entire ecosystem possible. fIt also means policymakers must catch up. States across the country should adopt and expand laws like Freelance Isn’t Free so that a worker’s rights don’t end at a city or state line. If SXSW is where the future comes into focus, it should also be where we decide what kind of future we’re building—one where creativity is celebrated and protected, and where the workers behind the scenes are finally recognized as essential to the story. Congressman Greg Casar speaking at Axios House1 Upwork Research Institute, Freelance Forward 2023: The Growing Freelance Workforce in the United States, 2023, https://www.upwork.com/research/freelance-forward-2023-research-report; see also Gig Economy Data Hub (Rockefeller Institute of Government), “Freelance Forward Data Sources,” https://gigeconomydata.org/research/data-sources/freelance-forward.html. View the full article

-

Grasping the current environment of commercial real estate loan rates is essential for anyone considering investment options. Rates can vary considerably based on property type and loan structure. For instance, multifamily properties over $6 million carry a rate of 5.16%, whereas those under see a higher rate of 5.60%. Nevertheless, other factors like borrower creditworthiness likewise play an important role in determining these rates. What other elements should you consider when maneuvering through this complex market? Key Takeaways Multifamily property loans over $6 million have an interest rate of 5.16% with 80% LTV, while those under $6 million are at 5.60%. Commercial retail mortgages feature a 6.07% interest rate and a 75% loan-to-value (LTV) ratio. SBA 504 loans offer rates between 5.65% and 6.50%, with a higher LTV of 90%. Bridge loans are available at a 9.00% interest rate with an 80% LTV, suitable for short-term financing. Fannie Mae and Freddie Mac small balance loans range from 5.60% to 7.15% and 5.93% to 6.12%, respectively. Current Commercial Mortgage Rates as of December 1, 2025 As of December 1, 2025, comprehending the current commercial mortgage rates can greatly impact your investment decisions. For those interested in multifamily properties, loans over $6 million have an interest rate of 5.16%, with a loan-to-value (LTV) ratio of up to 80%. If you’re considering loans under $6 million, the rate stands at 5.60%, additionally allowing for an LTV of 80%. Within the sector of commercial retail, mortgages are available at a rate of 6.07%, capped at a 75% LTV. For SBA 504 loans, expect an interest rate of 6.50%, permitting an LTV of up to 90%. If you need short-term financing, bridge loans are currently priced at 9.00%, with an LTV ratio of up to 80%. Consulting a commercial property mortgage broker can provide further insights into these commercial real estate loan rates and help you navigate commercial loans in California effectively. Understanding Different Types of Commercial Mortgages Grasping the different types of commercial mortgages is important for anyone looking to finance a commercial property. You’ll encounter various options, such as conventional loans, SBA loans, CMBS loans, and agency loans. Conventional loans typically offer interest rates between 5% and 10%, depending on your creditworthiness and loan terms. If you’re considering owner-occupied properties, SBA 504 loans might suit you, offering rates of 5% to 7% with a lower down payment requirement. CMBS loans focus more on the property’s strength rather than your credit, making them ideal for assets with long lease terms. Finally, agency loans from Fannie Mae and Freddie Mac are popular for multifamily properties, featuring rates from 5.60% to 7.15% and LTV ratios up to 80%. Consulting a commercial real estate mortgage broker or celoc lenders can help you navigate these options effectively, especially in the competitive environment of commercial real estate loans California. Factors Influencing Commercial Mortgage Rates Comprehending the factors influencing commercial mortgage rates is essential for making informed financing decisions. Various elements can impact investment real estate loans rates, including property type, borrower creditworthiness, loan-to-value (LTV) ratios, economic conditions, and the debt service coverage ratio (DSCR). Factor Description Property Type Multifamily loans usually have lower rates than office or retail properties. Borrower’s Creditworthiness Stronger credit profiles secure more favorable terms. Loan-to-Value (LTV) Ratio Lower LTVs indicate reduced risk, leading to lower rates. Economic Conditions Inflation trends and Federal Reserve policies affect rates. Debt Service Coverage Ratio Higher DSCRs are viewed as less risky, resulting in better interest rates. Understanding these factors helps you navigate the average commercial loan term effectively, positioning you for better financing options. Current Interest Rates for Various Loan Types When considering various commercial loan types, it’s crucial to understand the current interest rates that can greatly impact your financing options. Multifamily loan rates typically fall in line with conventional loans, whereas SBA options, like the 504 and 7(a) loans, offer competitive rates with specific terms. Furthermore, if you’re looking into short-term financing, bridge loans can present a range of costs that vary based on your circumstances and property type. Multifamily Loan Rates Multifamily loan rates have become a critical consideration for investors and property owners seeking financing options in today’s market. As of December 1, 2025, rates for loans exceeding $6 million are set at 5.16%, with a loan-to-value (LTV) ratio of up to 80%. For loans under $6 million, the interest rate is slightly higher at 5.60%, additionally maintaining an 80% LTV. Fannie Mae Small Balance loans offer fixed rates between 5.60% and 7.15% for amounts ranging from $1,500,000 to $6,000,000. Conversely, Freddie Mac Small Balance loans feature rates from 5.93% to 6.12%, providing similar amounts and LTV ratios. Nonrecourse financing options are available, appealing to seasoned investors seeking lower debt service. SBA Loan Options SBA loan options offer valuable financing solutions for small businesses, especially as traditional lending avenues may not be accessible. Two popular types are the SBA 504 and SBA 7(a) loans, each with distinct features. Loan Type Interest Rate Range Max Loan Amount Min Down Payment LTV Ratio SBA 504 5.65% – 5.93% $5 million 10%-20% 90% SBA 7(a) 5.50% – 9.00% $5 million 10% 85% The SBA 504 loan is best for purchasing fixed assets like real estate, whereas the SBA 7(a) loan can cover various business needs, including working capital. Remember, your creditworthiness and property type influence the final interest rate you’ll receive. Bridge Loan Costs Bridge loans serve as a valuable financing option for those seeking quick access to capital, particularly in the commercial real estate sector. Currently, interest rates for bridge loans range from 9.00% with a Loan-to-Value (LTV) ratio of up to 80%. These loans are typically short-term solutions designed for immediate needs, such as property acquisitions or renovations. Because of their short-term nature and associated risks, bridge loans usually have higher interest rates compared to long-term financing options. Their interest-only structure helps you manage cash flow effectively during the loan term. Although bridge loans offer flexibility and speed, be aware that they may come with increased costs compared to traditional financing, making them a critical choice for urgent funding needs. Insights on SBA Loans for Commercial Real Estate When seeking financing for commercial real estate, comprehension of your options can be crucial, especially if you’re a small business owner. Two popular choices are SBA 504 and SBA 7(a) loans. SBA 504 loans typically offer fixed interest rates ranging from 5% to 7%, with a maximum loan amount of $5 million and a down payment requirement of 10% to 20% for owner-occupied properties. Conversely, SBA 7(a) loans have interest rates that can go up to 12.5%, additionally requiring at least a 10% down payment. Both loan types allow for high loan-to-value (LTV) ratios, with SBA 504 permitting up to 90% LTV and SBA 7(a) allowing up to 85%. The SBA guarantees a portion of these loans, which helps lower risks for lenders, often leading to more favorable terms like lower interest rates and longer repayment periods, making them ideal for financing commercial real estate. Current Trends in Commercial Mortgage Market The commercial mortgage market is currently experiencing notable shifts as borrowers adjust to evolving economic conditions. As of December 1, 2025, rates for multifamily loans over $6 million are at 5.16%, whereas those under $6 million stand at 5.60%. Recent Federal Reserve cuts in the federal funds rate have lowered financing costs, even as long-term treasury rates rise. Here’s a snapshot of current trends: Loan Type Interest Rate Multifamily > $6M 5.16% Multifamily 5.60% Bridge Loans Up to 9.00% Short-Term Deals Lower Prepayment Market conditions now favor Bank of America and credit union loans because of attractive terms, with borrowers increasingly opting for short-term deals. The demand for bridge loans is likewise rising, reflecting a need for quick financing solutions. Importance of Loan-to-Value Ratios Grasping Loan-to-Value (LTV) ratios is vital for anyone traversing the commercial mortgage environment. LTV ratios indicate the percentage of a property’s value financed through a loan, and lower ratios are typically perceived as less risky by lenders. Usually, LTV ratios for commercial mortgages range from 55% to 90%, depending on the loan type and property category, with multifamily properties often qualifying for higher ratios up to 80%. A lower LTV ratio can help you secure more favorable interest rates, showing a stronger equity position that reduces lender risk. LTV ratios greatly influence underwriting decisions, affecting both loan approval and the terms offered, including interest rates and amounts. Maintaining a healthy LTV ratio is imperative, as higher ratios can lead to increased costs, such as heightened interest rates and possible challenges in refinancing your loan. Comprehending this ratio is key to making informed financial decisions in real estate. Evaluating Borrower Creditworthiness Evaluating borrower creditworthiness is essential for securing favorable commercial mortgage rates. Lenders primarily assess your credit score, financial history, and overall financial stability to gauge risk. A strong credit score, typically above 700, can considerably improve your chances of obtaining lower interest rates and better loan terms. Additionally, lenders often require a detailed review of your personal financial statement (PFS) to evaluate liquidity, net worth, and income sources, all critical for underwriting decisions. Another key metric is the Debt Service Coverage Ratio (DSCR), which measures your ability to cover debt obligations with operating income. A DSCR of 1.25 or higher is usually preferred by lenders. Recent market trends show that borrowers with a proven track record of successful investments and strong financial profiles are more likely to access favorable financing options, including non-recourse loans. Comprehending these factors can empower you in your loan application process. The Role of Economic Conditions in Rate Determination When economic conditions shift, they can have a significant impact on commercial mortgage rates, as lenders adjust their pricing strategies to align with the broader financial environment. Factors like inflation and Federal Reserve policies play vital roles in this process. Recently, the Fed has raised interest rates to combat inflation, resulting in higher commercial mortgage rates compared to previous years. As of December 2025, the federal funds rate sits between 3.75% and 4.00%, directly affecting your borrowing costs for commercial real estate loans. Furthermore, economic stability and growth influence borrower creditworthiness, which can determine the interest rates that lenders offer you. Finally, fluctuations in market demand for commercial lending can lead to varying rates across different property types and loan products, making it important for you to stay informed about the economic terrain when seeking financing options in today’s market. Long-Term vs. Short-Term Financing Options Grasping the differences between long-term and short-term financing options is essential for maneuvering the commercial real estate market effectively. Long-term financing, such as conventional loans, typically offers fixed interest rates between 5% and 10%, with terms lasting five to ten years. This option is ideal for stable investments like multifamily properties, providing lower monthly payments and stability against interest rate fluctuations. On the other hand, short-term financing options, including bridge loans, often come with higher interest rates ranging from 7% to 14%. These loans are designed for quick financing needs, lasting from six months to three years. During short-term loans may involve interest-only payments, they usually require refinancing or selling the property within a brief timeframe. Choosing between these financing types greatly impacts your investment strategy, cash flow management, and exposure to financial risk in commercial real estate. Advantages of Working With Commercial Mortgage Brokers When you’re considering a commercial mortgage, working with a broker can provide you access to a variety of lenders and loan options that you mightn’t find on your own. These professionals have the expertise to negotiate better terms and rates, leveraging their knowledge of the market to benefit you. Access to Diverse Options Accessing diverse financing options is one of the key advantages of working with commercial mortgage brokers. They provide you with access to a wide range of capital sources, which can often lead to better loan terms and options than going solo. Here are some benefits: Expert Guidance: Brokers help you navigate complex loan products, ensuring you understand each option’s nuances. Established Relationships: They often have connections with lenders, which can result in more favorable rates, especially in competitive markets. Time-Saving: Brokers handle paperwork and communication, streamlining the entire loan application process for you. Market Insights: Many provide valuable information on current trends, helping you make informed decisions based on the latest financing conditions. Expert Negotiation Skills Working with commercial mortgage brokers not just provides access to diverse financing options but furthermore leverages their expert negotiation skills to secure favorable loan terms. These brokers have extensive knowledge of the lending environment, enabling them to identify lenders offering competitive rates customized to your specific profile and property type. By utilizing their established relationships with lenders, they can negotiate better terms, such as lower interest rates and reduced fees, eventually lowering your overall loan costs. Brokers also access a wider range of financing options, including niche products not directly advertised to borrowers. Their expertise streamlines the application process, saving you time and effort during providing valuable insights into market trends, ensuring you make informed decisions regarding your financing. How to Secure the Best Rates for Your Commercial Loan Securing the best rates for your commercial loan is vital for maximizing your investment’s potential returns, so it’s important to approach the process with a strategic mindset. Here are some steps you can take: Shop Around: Compare offers from various lenders, as rates can differ based on your property type and qualifications. Negotiate Terms: Leverage competitive offers. Well-qualified borrowers often negotiate better rates or lower fees, which can greatly reduce overall costs. Consider a Broker: Working with a commercial mortgage broker can simplify the application process and provide access to exclusive loan products. Stay Informed: Understand the factors influencing loan rates, including your creditworthiness and current economic conditions. Timing your application with favorable market rates can likewise be beneficial. Resources for Further Information on Commercial Mortgages When exploring resources for further information on commercial mortgages, you’ll find a variety of tools and materials that can aid your comprehension of the lending environment. Start with commercial mortgage brokers, who can connect you to diverse capital sources and help you navigate complex loan options. They often have insights on different loan types, like Fannie Mae loans for multifamily properties, which feature competitive rates and non-recourse options. It’s also crucial to understand how factors such as property type, borrower creditworthiness, and current economic conditions influence mortgage rates. Keeping track of market trends and lender policies is fundamental for securing favorable loan rates in a fluctuating financial setting. Online platforms and industry publications can provide up-to-date information on current rates, and attending workshops or seminars can further improve your knowledge about commercial mortgages, ensuring you’re well-informed when making decisions. Frequently Asked Questions What Are Current US Commercial Loan Rates? You’re likely looking at a range of commercial loan rates in the U.S., which typically fall between 5.63% and 9.00%. For multifamily loans over $6 million, expect rates around 5.16%, whereas loans under that amount are usually at 5.60%. Commercial retail mortgages average 6.07%, and SBA 504 loans are at 6.50%. Bridge loans are more expensive, often reaching 9.00%, depending on the property type and borrower’s creditworthiness. What Is the Interest Rate on Commercial Property? The interest rate on commercial property loans varies based on several factors, such as the loan type and your creditworthiness. Typically, you might see rates ranging from about 5% to upwards of 14%. For example, multifamily loans over $6 million often carry a rate around 5.16%, whereas SBA 504 loans can be around 6.50%. Retail mortgages usually sit at approximately 6.07%, reflecting the diverse options available in the commercial real estate sector. What Is a Typical Interest Rate on a Commercial Loan? A typical interest rate on a commercial loan varies widely, often ranging from 5% to 14%. Conventional loans usually fall between 6% and 10%, requiring a down payment of 20% to 25%. For SBA 504 loans, you might see fixed rates from 5% to 7% with a lower down payment of 10% to 20%. If you consider bridge loans or construction loans, expect rates from 7% to 14% and 8% to 13%, respectively. What Is the Loan Interest Rate for Commercial Property? When considering a loan for commercial property, interest rates vary based on several factors, including property type and loan amount. Typically, these rates range from 6% to 10%, depending on the lender and market conditions. For multifamily loans over $6 million, rates are around 5.16%, whereas smaller loans may see rates at 5.60%. Bridge loans, often used for short-term financing, tend to have higher rates, reaching up to 9%. Conclusion In conclusion, grasping current commercial real estate loan rates is vital for making informed financing decisions. With rates varying by property type and loan structure, it’s important to take into account factors like borrower creditworthiness and economic conditions. Whether you’re exploring multifamily, retail, or SBA loans, knowing the specifics can help you secure favorable terms. By working with knowledgeable brokers and staying updated on market trends, you can navigate the intricacies of commercial mortgages effectively. Image via Google Gemini This article, "Current Commercial Real Estate Loan Rates" was first published on Small Business Trends View the full article

-

We may earn a commission from links on this page. Deal pricing and availability subject to change after time of publication. Apple products are notoriously expensive. Whether you're an Apple fan or an Apple hater, we can all agree: These things aren't cheap. That's why shopping holidays, like Amazon's Big Spring Sale, can be a great time to save on typically pricey devices. While this Spring Sale doesn't have deals on most of Apple's latest iPhones or Apple Watches, there are some great discounts on previous-gen devices—as well as one sale on a brand-new iPad. iPad A16 (256GB) $359.10 at Amazon $499.00 Save $139.90 Get Deal Get Deal $359.10 at Amazon $499.00 Save $139.90 Apple Watch Ultra 2 $399.49 at Amazon $450.00 Save $50.51 Get Deal Get Deal $399.49 at Amazon $450.00 Save $50.51 Apple Watch Series 10 (GPS + Cellular) $499.00 at Amazon $799.00 Save $300.00 Get Deal Get Deal $499.00 at Amazon $799.00 Save $300.00 iPhone 13 (Renewed Premium) $296.05 at Amazon $346.88 Save $50.83 Get Deal Get Deal $296.05 at Amazon $346.88 Save $50.83 iPhone 14 (Renewed Premium) $358.26 at Amazon $383.34 Save $25.08 Get Deal Get Deal $358.26 at Amazon $383.34 Save $25.08 AirPods 4 with Active Noise Cancellation (Renewed Premium) $118.15 at Amazon $149.00 Save $30.85 Get Deal Get Deal $118.15 at Amazon $149.00 Save $30.85 SEE 3 MORE iPad A16 dealApple sells a lot of different iPads, some with fancy features and inflated price tags. But most of us really just need Apple's basic slab of glass, which Apple plainly calls "iPad." To be more specific, many call this the iPad A16, as that's the chipset this tablet comes with. It's no M-series SoC, of course, but the A16 has no trouble running iPadOS 26, and I imagine it won't have issues running the latest updates for years to come. This particular iPad only has 128GB of storage, which isn't much for a tablet in 2026. That said, if you can practice some storage management, and keep your iPad use to streaming and cloud storage for the most part, you can snag a cellular iPad for just $359.10. You can pay for a network plan if you want to, giving you the opportunity to use your iPad anywhere you can get cell service. Apple Watch Ultra 2 dealThe Apple Watch Ultra line is designed for extreme use cases, like intense hiking, diving, or swimming. But its features can also be good for casual athletes, or anyone who wants the biggest watch display Apple makes. While Apple's Ultra 3 is $799, you can save a lot of money by buying the previous generation model—especially with this Amazon sale. Right now, Amazon is selling the Apple Watch Ultra 2 for just $399.49. That's a great deal. While you don't get the Ultra 3's S10 chip or 5G connectivity, the Ultra 2 comes with most of the same fitness features, including a depth gauge to 40m and a siren. It also comes with cellular capabilities baked in—you'd have to spend an extra $100 to get the cellular version of the Apple Watch Series 11. Apple Watch Series 10 (GPS + Cellular) dealThe Apple Watch Series 10, like the Ultra 2, is the last-gen Apple Watch model. And like the Ultra 2, it's perfectly usable today. In fact, it might be a better value than the Series 11, as it offers a similar suite of features for a discounted price. The real advantage with this model right now, however, is you can score Apple's "premium" Titanium material at a huge discount. Usually, the Titanium Apple Watch starts at $799 for the 46mm option. But during Amazon's Big Spring Sale, you can pick one up for $499. My Apple Watch Series 6 is still going strong, but if it were showing even the slightest sign of failure, I'd be retiring it in favor of this watch in a heartbeat. iPhone 13 (Renewed Premium) dealIf you need a new iPhone, you don't have to go through Apple, or even your carrier. Instead, you can opt for an unlocked, refurbished iPhone, for a fraction of the cost of a brand new unit. In this case, the iPhone 13 might just be a great value: Amazon has Big Spring Deals on the 256GB variant, and prices vary by color. Right now, the cheapest option is the red version, a color Apple doesn't offer anymore on new iPhones, for $296.05. This isn't a brand new iPhone with all the latest bells and whistles, of course, but it's a solid device—even in 2026. It has Apple's A15 Bionic chip, the company's standard 6.1-inch OLED display, two 12MP camera (one wide, one ultra-wide), and full compatibility with the latest version of iOS. Amazon says its Renewed Premium products do not have scratches on the display, nor any cosmetic damage you can see from 12 inches way, and battery life that is great than 90% of the capacity of the product when it was new. iPhone 14 (Renewed Premium) dealAmazon also has a Big Spring Deal on the iPhone 14, if you're willing to pay slightly more for a slightly newer iPhone. That said, the iPhone 14 also uses Apple's A15 Bionic chip, though it has one extra GPU core than the iPhone 13. (You might notice a slight advantage in graphics-intensive apps and games.) The iPhone 14's camera is a bit better, but doesn't break any ground, and it supports Bluetooth 5.3 while the iPhone 13 supports Bluetooth 5. In fact, the only other major difference here is the iPhone 14's lack of physical SIM slot. If you need SIM card support, stick with the iPhone 13. AirPods 4 with Active Noise Cancellation (Renewed Premium) dealApple's AirPods 4 with Active Noise Cancellation also get a decent discount during the Big Spring Sale—if you're okay buying a pair of Renewed Premium earbuds. Right now, the earbuds are 21% off, meaning you can get a pair of noise cancelling AirPods for just $118.15. That comes with modern AirPods features, like Transparency Mode, Adaptive Audio (which adjusts the volume based on your environment), and Conversation Awareness (which automatically lowers the volume when it detects you're speaking). The only hitch here is that these AirPods are not "brand new." Again, these are Renewed Premium, which Amazon asserts have high standards for a refurbished product. That's all well and good for iPhones, but AirPods are another story, since no one wants someone's previously worn earbuds. My hope is that in this case, these are "open box" items, in which someone returned unused AirPods after breaking the seal on the packaging. But as it's impossible to know for sure, it's the risk you take to buy AirPods at a 21% discount. Our Best Editor-Vetted Amazon Big Spring Sale Deals Right Now Apple AirPods Pro 3 Noise Cancelling Heart Rate Wireless Earbuds — $199.00 (List Price $249.00) Apple iPad 11" 128GB A16 WiFi Tablet (Blue, 2025) — $299.00 (List Price $349.00) Samsung Galaxy Tab A11+ 128GB Wi-Fi 11" Tablet (Gray) — $202.00 (List Price $249.99) Sony WH1000XM6- Best Wireless Noise Canceling Headphones — $398.00 (List Price $459.99) Apple Watch Series 11 (GPS, 42mm, S/M Black Sport Band) — $299.00 (List Price $399.00) Blink Video Doorbell Wireless (Newest Model) + Sync Module Core — $35.99 (List Price $69.99) Fire TV Stick 4K Max Streaming Player With Remote — $34.99 (List Price $59.99) Amazon Kindle Colorsoft 16GB 7" eReader (Black) — $169.99 (List Price $249.99) Deals are selected by our commerce team View the full article

-

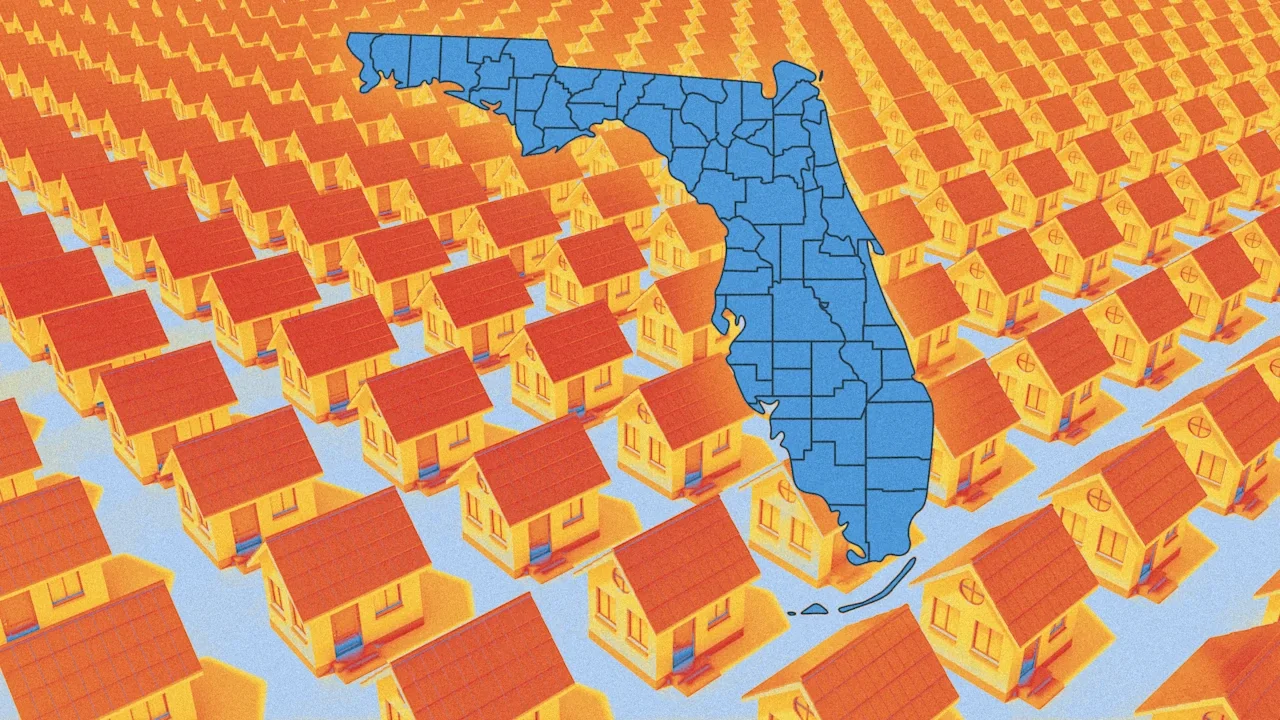

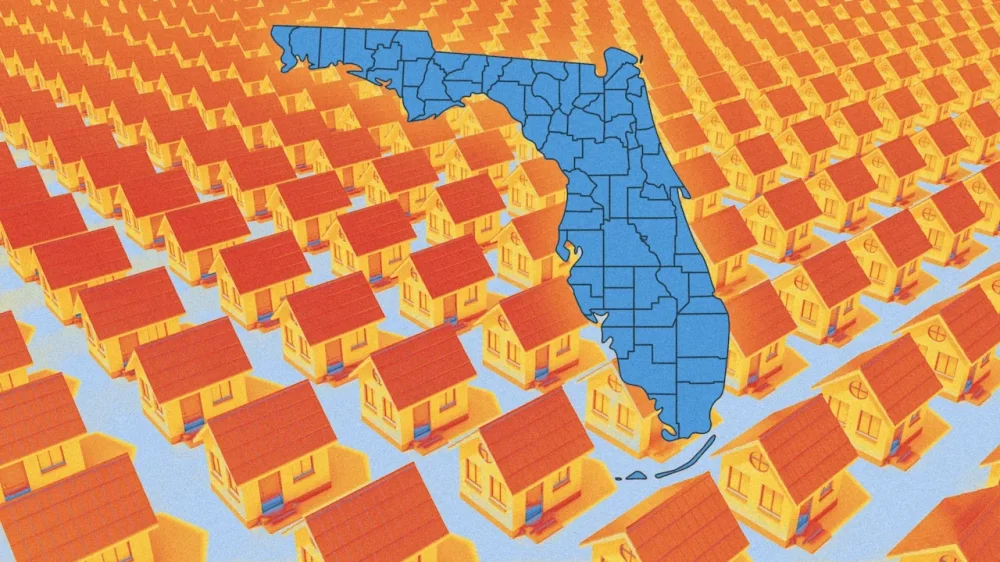

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. Florida’s particularly intense overheating during the Pandemic Housing Boom is the key reason for its downside pricing vulnerability. While U.S. home prices rose +41% between March 2020 and June 2022, Florida home prices surged +51% over the same period—leaving some parts of the state significantly overvalued. Only, it takes a large enough shift in the supply-demand equilibrium for that vulnerability to manifest into falling prices. Of course, over the past three years, 5 factors have come together to create a supply-demand equilibrium shift large enough to reveal some of that downside risk and push certain pockets of Florida into post-Pandemic Housing Boom corrections. The Pandemic Housing Boom’s migration surge to Florida has fizzled out. Indeed, Florida saw net domestic migration of +23K in 2025, compared to +314K in 2022. Without that larger influx of deep-pocketed buyers from up North, Florida home prices have had to rely more on local incomes. Surfside condo fallout. Following the Surfside condo collapse in June 2021, which killed 98 people, Florida passed new structural safety rules, requiring more inspections and additional funds for repairs to be set aside by the end of 2024. That has led to Florida HOAs issuing sky-high special assessments and monthly HOA fee increases to cover these costs. This has had a greater impact on older coastal Florida condo buildings. Hurricane Ian spurred a greater SWFL softening. Markets like Cape Coral and Punta Gorda, which were hard-hit by Hurricane Ian in September 2022, saw thousands of damaged homes, and the subsequent need for renovations. According to the National Oceanic and Atmospheric Administration, Hurricane Ian caused an estimated $112.9 billion worth of total damage, making Ian the third-costliest U.S. hurricane on record. That event helped create additional softening in SWFL. Supply elasticity. Unlike many housing markets in the Northeast and Midwest, Florida has a higher level of homebuilding and multifamily construction. As that new supply entered the market in the post-Pandemic Housing Boom affordability-strained environment, builders used bigger affordability adjustments—such as mortgage rate buydowns and price cuts—where needed to move it. That helped cool the Florida resale market further by drawing buyers who might have otherwise purchased existing homes toward new construction. As a result, this put additional upward pressure on Florida’s resale inventory after the Pandemic Housing Boom ended. Home insurance shocks. Over the past three years, the median annual U.S. home insurance premium has jumped around 30%, but Florida homeowners have been hit even harder. The surge in Florida home insurance rates is partly driven by rising replacement costs—home prices and construction costs soared during the boom—and partly by increased hurricane risks and insurance payouts. Florida’s sharp rise in insurance costs, combined with one of the biggest home price increases during the Pandemic Housing Boom, has led to one of the biggest housing affordability deteriorations. Everything above, ResiClub has detailed closely over the past few years—and when I was working at Fortune Magazine back in spring 2022 I detailed why Florida had elevated risk of a Pandemic Housing Boom correction. Let’s shift from the backward-looking drivers and examine what the real-time inventory and pricing indicators across Florida are telling us about the next phase of the state’s housing cycle. While active housing inventory is still rising in most U.S. housing markets on a year-over-year basis, the pace of growth continues to decelerate across much of the country. In fact, Florida—home to many of the weakest regional housing markets over the past two years—is now seeing active inventory edge down slightly year-over-year (-4%). What’s interesting is that many of Florida’s housing markets where home prices have fallen the most during the post-Pandemic Housing Boom recalibration period—including Punta Gorda and Cape Coral—are currently seeing some of the largest year-over-year declines in active inventory for sale. The fact that inventory isn’t bursting upward anymore in Punta Gorda and Cape Coral, and is actually declining somewhat, suggests that those markets may slowly be finding their footing and, at the very least, that the intensity of their corrections is easing. Click here for an interactive of the chart below In the side-by-side maps below you can clearly see that the inventory burst in Southwest Florida—arguably the epicenter of U.S. housing market weakness over the past 24 months—is no longer happening. Indeed, most ZIP Codes in SWFL are down a little year-over-year for active inventory. The screenshots below are pulled from the ResiClub Terminal. LEFT: Year-over-year shift in active housing inventory for sale between Feb. 2024 to Feb. 2025 RIGHT: Year-over-year shift in active housing inventory for sale between Feb. 2025 to Feb. 2026 Big picture: Softness—and even outright weakness—remains across many parts of Florida’s housing market. However, the intensity of the downturn in Florida has eased somewhat in recent months. ResiClub members who’d like to view our deep dive into Florida housing markets, should go here. View the full article

-

If you could earn thousands of dollars more a year just by having a two-minute conversation, would you do it? That might sound like an easy “yes,” but for a lot of people, the answer, surprisingly, is no. At Slate today, I wrote about people who literally never negotiate their salary when they’re offered a job or haven’t had a raise in a long time. Instead, they accept the first number an employer offers, because they’re worried that they’ll look greedy or mercenary — even though the whole reason we work is for pay! You can read it here. The post there’s only one way to get more money at work, and some people won’t do it appeared first on Ask a Manager. View the full article

-

Tufts index projects 9M U.S. jobs at risk from AI. Writers and Authors, Computer Programmers, and Web and Digital Interface Designers top the risk list. The post New AI Jobs Index Ranks 784 Occupations By Loss Risk appeared first on Search Engine Journal. View the full article

-

Financial Conduct Authority lowers estimate for loans eligible for compensation schemeView the full article

-

Google says a new compression algorithm, called TurboQuant, can compress and search massive AI data sets with near-zero indexing time, potentially removing one of the biggest speed limits in modern search systems. What it is. TurboQuant is a way to shrink and organize the data that powers AI and search without losing accuracy. It reduces memory use while keeping results precise and cuts the time to build searchable AI indexes to “virtually zero,” according to the research paper. How it works. Modern search converts content into vectors (lists of numbers that represent meaning). Similar ideas sit close together in this numeric space, and search finds the closest matches. However, these vectors are large and expensive to store and search. TurboQuant addresses this by using much smaller data that behaves almost exactly like the original, through: Smart compression. It rotates the data mathematically to compress it cleanly, like organizing messy items into neat boxes. Error correction. It adds a 1-bit signal to fix small compression errors and preserve accuracy. What it means. Vector search — the system behind semantic search and AI answers — has been slow and expensive at scale. TurboQuant makes it faster and cheaper. Google says it enables faster similarity search, lower memory costs, and real-time processing of massive datasets. Why we care. Google can evaluate far more documents per query, not just a small subset. If/when Google adopts this in Search, AI Overviews could pull from a broader, more precise set of sources, making it easier to generate instant summaries from large data pools. More about TurboQuant: Google: TurboQuant: Redefining AI efficiency with extreme compression Research paper (arXiv): TurboQuant: Online Vector Quantization with Near-optimal Distortion Rate Marie Haynes: TurboQuant has the potential to fundamentally change how Search (and AI) works View the full article

-

We may earn a commission from links on this page. Deal pricing and availability subject to change after time of publication. Amazon's Big Spring Sale is nearing its end, but there's still time to take advantage of solid deals for all your fitness needs—here are all the best fitness deals under $100 that are still available. Deals on strength training equipmentIt seems like the heavier you want to lift, the more expensive it's going to get. In the meantime, there are great deals on starter dumbbells, storage solutions, and more: UNNMIIY 5 in 1 adjustable dumbbells, $79.98, down from $109.99 PLKOW storage and weight rack, $79.98, down from $129.99 NICEPEOPLE adjustable weight bench, $64.59, down from $75.99 Resistance bands, $24.98, down from $37.99 If you're willing to go slightly above your $100 budget, I recommend opting for these Lifepro adjustable dumbbells, currently on sale for $150.09, down from $189.99. UNNMIIY Adjustable Dumbbells, 20/30/45/70/90lbs Free Weight Set with Connector,5 in1 Dumbbells Set Used as Barbell, Kettlebells, Push up Stand, Fitness Exercises for Home Gym Suitable Men/Women $79.98 at Amazon $109.99 Save $30.01 Get Deal Get Deal $79.98 at Amazon $109.99 Save $30.01 Deals on fitness trackersThe Fitbit Inspire 3 is on sale for $69.95, down from $99.95. If you want a simple, minimalist fitness tracker, this is a great way to grab one on the cheap. The Inspire 3 is, in many ways, a pared-down Charge 6, and I simply have to mention that the Fitbit Charge 6 is currently $119.95, down from $159.95. If you're stuck deciding between these two budget options, I recommend reading my colleague Beth Skwarecki's review of the Charge 6 here. For a reliable chest strap, the Polar H10—widely regarded as the best heart rate monitor out there—is on sale for $76.99, down from $104.99. Fitbit Inspire 3 $69.95 at Walmart $89.95 Save $20.00 Get Deal Get Deal $69.95 at Walmart $89.95 Save $20.00 Deals on muscle recovery and stretching equipmentIf you're looking for a travel-sized massage gun, the Bob and Brad Q2 Ultra Mini Massage Gun is on sale for $78.82, down from $99.99. For me, the real selling point of this massage gun—which I reviewed in-depth here—is how great the heat therapy feels. Plus, its compact size makes it perfect for travel or bringing to the gym—something I never considered with my full-sized TheraGun Therabody. Some more deals in this realm: 5 in 1 Foam Roller Set, $32.99, down from $39.95 1-Inch Thick Yoga Mat, $29.99, down from $36.99 TriggerPoint Grid 1.0 Foam Roller, $27.99, was $39.99 Bob and Brad Q2 Ultra Mini Massage Gun $78.82 at Amazon $99.99 Save $21.17 Get Deal Get Deal $78.82 at Amazon $99.99 Save $21.17 Deals on headphones and earbudsThe original Shokz OpenRun are available for $89.94, down from a list price of $129.95. They might not have as powerful bass or as long a battery life compared to my favorites, the OpenRun Pro 2 (also on sale right now, for $139.95), but they're still a top choice of open-ear bone conduction headphones. If you're eyeing Sony noise-cancelling headphones that won't put you out hundreds of dollars, the Sony WH-CH720N are available for $94 (originally $179.99) on Amazon right now. For more great deals on home gym equipment (even though, fair warning, many of them exceed this post's $100 benchmark), check out my round-up here. Shokz OpenRun $89.94 at Amazon $129.95 Save $40.01 Get Deal Get Deal $89.94 at Amazon $129.95 Save $40.01 Our Best Editor-Vetted Amazon Big Spring Sale Deals Right Now Apple AirPods Pro 3 Noise Cancelling Heart Rate Wireless Earbuds — $199.00 (List Price $249.00) Apple iPad 11" 128GB A16 WiFi Tablet (Blue, 2025) — $299.00 (List Price $349.00) Samsung Galaxy Tab A11+ 128GB Wi-Fi 11" Tablet (Gray) — $202.00 (List Price $249.99) Sony WH1000XM6- Best Wireless Noise Canceling Headphones — $398.00 (List Price $459.99) Apple Watch Series 11 (GPS, 42mm, S/M Black Sport Band) — $299.00 (List Price $399.00) Blink Video Doorbell Wireless (Newest Model) + Sync Module Core — $35.99 (List Price $69.99) Fire TV Stick 4K Max Streaming Player With Remote — $34.99 (List Price $59.99) Amazon Kindle Colorsoft 16GB 7" eReader (Black) — $169.99 (List Price $249.99) Deals are selected by our commerce team View the full article

-

Measure brand awareness online by tracking brand mentions, monitoring AI search visibility, and more. View the full article

-

You can’t afford to take them for granted. By Ed Mendlowitz Tax Season Opportunity Guide Go PRO for members-only access to more Edward Mendlowitz. View the full article

-

You can’t afford to take them for granted. By Ed Mendlowitz Tax Season Opportunity Guide Go PRO for members-only access to more Edward Mendlowitz. View the full article

-

Golden Pass plant owned by QatarEnergy and ExxonMobil may help replace shortages hit by Hormuz crisis View the full article

-

A pair of landmark court cases found Meta and YouTube guilty last week of harming young users by designing algorithms that were addictive and led to mental health distress. The damages assessed against the companies amounted to a fraction of a percent of their annual earnings. The long-term implications, however, could be far more significant. The rulings found that programmed algorithms are not protected by Section 230, the federal law that shields social media companies from liability for user-posted content. That represents a crack in a legal defense these companies have relied on for years. And thousands of similar cases are already pending. Section 230 has been under scrutiny for some time. Lawmakers have repeatedly called for its repeal, though efforts so far have failed to gain traction. Many in Congress appear to view the threat of repeal as leverage, hoping it will push tech companies to negotiate changes that reflect how the internet has evolved since the law was passed. “Section 230 was created during the early advent of the internet, when lawmakers were trying to give emerging online companies room to innovate and experiment with technologies the public and policymakers barely understood,” says J.B. Branch, AI Governance and Technology Policy Counsel at Public Citizen. “It was never intended to operate as a permanent legal shield for some of the most powerful corporations in the world.” Reframing the argument Has Section 230 lost its protective power? Not yet. The core premise of the law still holds: companies are not liable for user-generated content. What has changed is how plaintiffs can work around that protection. The new cases focus less on what users post and more on how platforms are designed. In other words, product design may be the greater legal vulnerability. “CEOs like Mark Zuckerberg, Tim Cook, and Evan Spiegel have to rethink how they design products that kids use because they can no longer hide fully behind Section 230,” says Sarah Gardner, CEO of Heat Initiative, an organization focused on online safety for children. That shift assumes the rulings survive appeals. Meta and YouTube are expected to challenge the decisions, likely setting up a years-long legal battle that could ultimately reach the Supreme Court. Even so, the broader debate has already begun. Forced accountability The implications are significant, particularly when it comes to younger users. The rulings push companies toward a level of accountability that, in some ways, mirrors the trajectory of the adult entertainment industry. It’s an imperfect comparison, but there are parallels, says Ramnath Chellappa, a professor at Emory University’s Goizueta School of Business. Adult sites have increasingly been required to verify users’ ages. Similar mechanisms could emerge for social media. “The mechanism for monitoring … to ensure that a minor is a minor and so on is already a very complex topic,” he says. “What does that involve? Does that involve a third party, or does one need to share their driver’s license information?” Lexi Hazam of Lieff Cabraser Heimann & Bernstein, LLP, co-lead of the Social Media MDL, agrees the rulings could force major operational changes, though she stops short of drawing a direct comparison. “The implications are significant and show these tech giants that no company is above accountability when it comes to our children,” she says. “The companies will have to reassess how they design and operate their platforms moving forward … potentially requiring the companies make real changes, including safer platform design, effective age verification, and parental controls that actually work to protect young users.” Not everyone sees weakening Section 230 as beneficial. Critics argue the current debate overemphasizes harms while overlooking benefits. “Public debate about social media and youth mental health focuses almost exclusively on potential harms,” wrote the International Center for Law & Economics’ Ben Sperry and Sabrina Pekarovic in a recent essay, arguing that this emphasis downplays the ways platforms can enable self-expression and connect teens to broader communities. They add that treating all teenagers as equally vulnerable oversimplifies the issue and isn’t supported by the evidence. “Blanket bans assume that all teenagers face similar risks and should be treated alike,” they wrote. “The evidence suggests otherwise.” A Big Tobacco moment Some observers have compared the rulings to a “Big Tobacco” moment for social media, a long-awaited reckoning that could lead to sweeping regulation. That could include changes to Section 230 or a broader overhaul of how platforms operate. Either outcome would carry major financial consequences for companies that have long been dominant players on Wall Street. The potential impact on investors is substantial. One report from the Computer and Communications Industry Association estimates that repealing Section 230 could cost investors $2.2 trillion and lead to roughly 1.1 million lawsuits per year against digital service companies. Some analysts believe the direction is already clear. “The consequences for social networks will be devastating,” says Igor Pejic, a tech investing strategist and author of Tech Money. “Regulation will escalate as it did with the tobacco industry and one day we might see things like required ID authentication. This regulatory trend will not kill social media, but I believe that in a couple of years they will at least lose their status as a Big Tech company.” View the full article

-

Five considerations for bringing in an outside perspective. By Domenick J. Esposito 8 Steps to Great Go PRO for members-only access to more Dom Esposito. View the full article

-