All Activity

- Past hour

-

Oracle has unveiled enhanced AI capabilities in collaboration with Google Cloud, opening doors for small businesses looking to supercharge their data operations. The latest upgrade introduces the Oracle AI Database Agent for Gemini Enterprise, making it easier to interact with Oracle databases using natural language. This update aims to bolster the operational efficiency and innovation potential of small businesses, offering an accessible pathway to utilize AI-driven insights from their enterprise data. Nathan Thomas, Oracle Cloud Infrastructure’s senior vice president of product management, expressed the company’s commitment to integrating AI into data management processes. “We’re making it easier for customers to use natural language to access, understand, and act on enterprise data,” he said. This functionality allows small business owners to tap into their data with minimal technical expertise, which can lead to smarter decision-making and improved strategies without the complexity typically associated with data analysis. The advantages of the Oracle AI Database Agent are manifold. For small business owners, the ability to query data using everyday language rather than complex programming or SQL commands can dramatically streamline operational processes. For instance, businesses can quickly analyze revenue trends or customer behavior, enabling them to adjust pricing strategies or optimize marketing efforts in real-time. By interpreting requests and delivering context-aware answers, this tool helps business owners focus on strategy rather than getting bogged down by data management complexities. As the platform now integrates with Google Cloud, small businesses can leverage additional AI tools to automate workflows, enhancing their capacity to perform data extraction and visualization efficiently. Furthermore, this integration enables companies to maintain a high level of data governance and security while enjoying increased flexibility and power from their data sources. AI Shift, a subsidiary of CyberAgent, serves as a case study in how enterprises can harness these capabilities. CEO Yuto Yoneyama emphasized, “With Gemini Enterprise, our users can move from writing SQL to asking questions in natural language,” demonstrating the broader implications of this technology for developing efficient AI solutions across various industries. Moreover, the expansion of Oracle AI Database@Google Cloud to 15 regions worldwide offers small businesses a robust infrastructure to support their operations. Key locations—including Tokyo, Sydney, and São Paulo—help bring services closer to customers, thus providing options tailored to local business needs. This geographical flexibility enables small business owners to operate on a global scale while ensuring that they meet regional compliance and performance requirements. However, with these advancements, small business owners should also be mindful of potential challenges. Implementing new technologies often requires an investment in training and change management. Transitioning to an AI-driven system can necessitate adjustments in organizational culture and employee workflows. Business owners need to evaluate whether their current infrastructure and team capabilities can adapt to these changes effectively and how they can navigate any learning curves. The new Oracle AI Database capabilities also include features like real-time database migration and seamless integration with Google BigQuery, which can help businesses implement high-availability solutions without incurring excessive data movement costs. Such advancements allow small companies to operate more dynamically, taking advantage of insights from live data rather than relying on outdated reports. As more organizations adopt Oracle AI Database@Google Cloud, including major players like Worldline, the trend signals a significant shift toward data-driven decision-making powered by AI. Arni Smit from Worldline noted, “Oracle AI Database@Google Cloud gives us the scalability, resilience, and security capabilities we require.” This sentiment resonates with the small business community, pushing entrepreneurs to anticipate changes in technology and adapt accordingly. In summary, Oracle’s latest enhancements to its AI Database services represent a noteworthy evolution in how small businesses can engage with their data. The integration of natural language processing into database queries stands to simplify operations, and with the added support of the Google Cloud infrastructure, small business owners now have greater tools at their disposal. Adapting to these technologies could enable small businesses not just to keep pace but to innovate and thrive in an increasingly data-dependent landscape. For further details, you can visit the full press release here. Image via Google Gemini This article, "Oracle and Google Cloud Unveil AI Database Agent for Enhanced Data Insights" was first published on Small Business Trends View the full article

- Today

-

Regarding paying taxes, grasping the deadlines is vital. You’ll find that the primary deadline for federal income tax returns is April 15, but don’t forget about quarterly estimated payments due on April 15, June 15, September 15, and January 15. Furthermore, contributions to IRA and HSA accounts must likewise be made by April 15. Missing these deadlines can lead to penalties, so it’s important to stay informed. What happens if you need more time? Key Takeaways Federal income tax returns are due by April 15, 2026, for the 2025 tax year. W-2 forms from employers must be received by February 2, 2026. Estimated tax payments are due quarterly on April 15, June 15, September 15, and January 15. Extensions can be requested by April 15, extending the filing deadline to October 15, but taxes owed must still be paid by April 15. State tax deadlines may vary, so check specific state requirements for filing and payment. Understanding Tax Deadlines Comprehending tax deadlines is critical for avoiding penalties and guaranteeing compliance with the IRS. For individuals, the primary Tax Day for federal income tax returns is April 15, 2026. Nonetheless, if this date lands on a weekend or holiday, it shifts to the next business day. Regarding tax quarterly payments, you need to make your first estimated payment on April 15, followed by payments due on June 15, September 15, and the final payment on January 15 of the following year. Employers are required to provide W-2 forms by February 2, 2026, helping you report your income accurately. If you can’t meet the April deadline, you can request a six-month extension using IRS Form 4868, pushing your filing date to October 15. Finally, keep in mind that state tax deadlines may differ, so check your state’s requirements to guarantee full compliance. Key Dates for Individual Filers As an individual filer, it’s essential to stay on top of key tax dates to avoid penalties and guarantee you’re filing accurately. Mark April 15, 2026, as your primary deadline for income tax returns, in addition to noting that estimated tax payments are due on January 15, 2026. Familiarizing yourself with these dates, along with options for filing extensions, can help you manage your tax responsibilities effectively. Tax Day Deadline When is the deadline for filing your individual income tax return? Tax Day for individual filers is April 15, 2026, except it lands on a weekend or holiday, in which case it shifts to the next business day. Knowing when you pay taxes is essential to avoid penalties. Here are some key dates to remember: W-2 forms from employers are due by February 2, 2026. The fourth quarter estimated tax payment for 2025 is due on January 15, 2026. Contributions to IRA and HSA accounts for the 2025 tax year must be made by April 15, 2026. Missing the April 15 deadline may result in penalties and interest until your taxes are paid in full. Estimated Payment Schedule Comprehending your estimated payment schedule is vital for staying on top of your tax obligations. Individual filers must make estimated payments quarterly to avoid penalties and interest for underpayment. The first payment is typically due on April 15, covering income earned from January 1 to March 31. Your second estimated payment is due on June 15 for income earned from April 1 to May 31. Then, mark your calendar for September 15, when the third payment is due, covering income from June 1 to August 31. Finally, the last estimated payment for the year is due on January 15 of the following year, addressing income earned from September 1 to December 31. Staying punctual with these dates is critical for compliance. Extension Filing Options If you find yourself needing more time to file your tax return, you can request an automatic six-month extension by submitting IRS Form 4868 by the original due date of April 15. With this extension, your new filing deadline becomes October 15. Nevertheless, keep in mind that although you have more time to file, you still need to pay any taxes owed by April 15. Not paying on time can lead to penalties and interest. Here are some key points to remember: Extension doesn’t delay payment deadlines. Capital gains taxes are due by April 15. File Form 4868 for an extension. Check for additional relief if in a disaster area. Stay informed to avoid unnecessary penalties. Important Deadlines for Businesses When it relates to tax deadlines, businesses need to stay on top of key filing dates to avoid penalties. For Partnerships and S-Corporations, the deadline is March 15, but you can extend it to September 15 if needed. C Corporations have the same initial deadline, and comprehending your quarterly payment schedule is crucial to keep your finances in check. Key Filing Dates Managing tax deadlines can feel overwhelming, but knowing key filing dates is crucial for your business’s compliance and financial health. Mark your calendar for these important dates: March 15, 2026: Deadline for Partnerships, S-Corporations, and C Corporations to file. September 15, 2026: Extension deadline for Partnerships and S-Corporations using Form 7004. October 15, 2026: Extension deadline for C Corporations filing Form 1120. April 15, 2026: First estimated tax payment required for the 2025 tax year. If you’re wondering when do you pay taxes on stocks, be aware that capital gains taxes are required when you sell the stocks, impacting your overall tax obligations. Always check if deadlines shift because of weekends or federal holidays. Quarterly Payment Schedule Comprehension of the quarterly payment schedule is essential for businesses to stay compliant with tax obligations. You’ll need to make quarterly pay estimated tax payments on specific dates: April 15, June 15, September 15, and January 15 of the following year. For 2025, your first payment is due on April 15, covering income earned from January 1 to March 31. The second payment is due on June 15, for income from April 1 to May 31. The third payment on September 15 will cover income from June 1 to August 31. Finally, the last quarterly payment for the year is due on January 15, 2026, which includes income earned from September 1 to December 31, 2025. Consequences of Missing Tax Deadlines Missing tax deadlines can lead to significant financial repercussions that accumulate over time. When you fail to meet these deadlines, especially for tax quarters, you may face various penalties and interest that increase your overall tax liability. Here are some consequences you might encounter: A penalty of 5% of unpaid taxes for each month your return is late, capping at 25%. Additional failure-to-pay penalties of 0.5% of unpaid taxes each month until resolved. Delayed refunds, as the IRS processes returns in the order received. Accumulating interest charges on unpaid balances, which can further inflate what you owe. To mitigate penalties, it’s essential to file your return as soon as possible. If you’re due a refund, filing late typically incurs no penalties, and you can claim your refund within three years. Extensions and Special Circumstances Taxpayers often find themselves in situations where they may need extra time to file their returns or may face unexpected circumstances that affect their tax obligations. If you need more time, you can apply for an automatic six-month extension by submitting IRS Form 4868, which must be postmarked by the original due date of April 15. In federally declared disaster areas, the IRS may grant additional time for filing and payment, automatically extending deadlines for affected taxpayers. It’s crucial to check your eligibility for any extensions or relief measures to guarantee compliance with IRS regulations. If you make mistakes during filing, you can correct them by re-filing your taxes; acting quickly minimizes potential penalties. Comprehending when you pay tax in these situations can help you manage your obligations effectively and avoid unnecessary stress. Always stay informed about your rights and options regarding extensions and special circumstances. Estimated Tax Payments Explained Have you ever wondered how estimated tax payments work? If you expect to owe $1,000 or more in taxes when filing your return, you’ll need to make estimated tax payments. These are typically paid quarterly, with due dates on April 15, June 15, September 15, and January 15 of the following year. The payment periods align with specific dates: January 1–March 31 for the April payment April 1–May 31 for the June payment June 1–August 31 for the September payment September 1–December 31 for the January payment To avoid penalties for underpayment, make certain you pay at least 90% of your current year’s tax liability or 100% of your previous year’s tax liability. You can conveniently make your estimated tax payment online, by phone, or through the IRS2Go app, which offers flexibility to fit your schedule. Payment Options for Tax Obligations With regard to fulfilling your tax obligations, you have several payment options available that can simplify the process. You can make tax payments online through various methods, including direct debit from your bank account or credit card payments. These options are available anytime before the due date. If you’re wondering when do you pay capital gains tax, keep in mind that estimated tax payments are due quarterly—specifically on April 15, June 15, September 15, and January 15 of the following year for those not subject to withholding. If you can’t pay the full amount by the deadline, you can request a payment plan from the IRS to manage your obligations over time. For electronic payments via Webfile, make sure they’re submitted by 11:59 p.m. CT on the due date. If you opt for paper checks, they must be postmarked by the tax deadline to avoid penalties. Filing and Payment Deadlines In terms of filing your taxes, knowing the key deadlines is crucial. Individual income tax returns are due on April 15, 2026, but you can file for an extension until October 15 if needed. Furthermore, keep in mind the quarterly estimated tax payment schedule, with payments due on April 15, June 15, September 15, and January 15 of the following year. Key Tax Payment Dates Comprehending key tax payment dates is crucial for managing your financial responsibilities effectively. Knowing when to pay tax helps you avoid penalties and guarantees compliance. Here are some important deadlines to keep in mind: Individual federal income tax returns are due on April 15, 2026. Quarterly estimated tax payments for 2025 are due on April 15, June 15, September 15, and January 15, 2027. W-2 forms must be issued by February 2, 2026. You can request an extension until October 15, 2026, but remember, this doesn’t extend your payment deadline. Stay organized and mark these dates on your calendar to make sure you’re prepared to meet your tax obligations when do you pay tax. Estimated Tax Payment Schedule Comprehending the estimated tax payment schedule is essential for managing your tax responsibilities throughout the year. Estimated tax payments are due quarterly: the first payment for income earned from January 1 to March 31 is due by April 15, the second for April 1 to May 31 by June 15, the third for June 1 to August 31 by September 15, and the final payment for September 1 to December 31 by January 15 of the following year. To avoid penalties, you must make your estimated tax payments on time, as underpayment can lead to interest and charges. Use IRS Form 1040-ES to help determine your quarterly payment amounts, and keep in mind that electronic payments are due by 11:59 p.m. CT. State vs. Federal Tax Deadlines How do state tax deadlines compare to federal ones? When you’re figuring out when do I pay tax, it’s vital to comprehend that federal tax returns are usually due on April 15, but this can shift to the next business day if that date falls on a weekend or holiday. Nevertheless, state deadlines can vary considerably: Maine and Massachusetts have deadlines around April 18 because of state holidays. Some states don’t impose personal income taxes at all. Specific state tax deadlines may not align with federal ones. Different penalties for late filing might apply based on state laws. It’s important to check your state’s regulations to avoid any surprises. Grasping these differences will help guarantee you meet both state and federal obligations without incurring unnecessary penalties. Resources for Tax Payment Assistance Meeting your tax obligations can sometimes feel intimidating, especially regarding making payments. Fortunately, there are plenty of resources to assist you with the tax payable process. You can make tax payments online anytime, using methods like bank account transfers or credit cards, giving you flexibility. If you can’t pay your tax debts, the IRS allows you to request a payment plan, helping you manage your obligations over time without incurring penalties and interest. Additionally, the IRS provides assistance for those facing payment difficulties, ensuring you have access to support. When you file electronically, tax software typically includes payment options, streamlining the process and confirming receipt by the IRS. For further guidance, numerous video resources are available online, offering visual aids that simplify comprehending various payment methods and deadlines. These tools can make steering through your tax responsibilities much easier, allowing you to fulfill your obligations confidently. Frequently Asked Questions At What Amount Do You Have to Start Paying Taxes? You start paying federal income taxes when your gross income exceeds specific amounts. For single filers, this threshold is $13,850, whereas married couples filing jointly must exceed $27,700. If you’re a dependent, you’ll owe taxes on earned income over $13,850 or unearned income over $1,250. Self-employed individuals must pay taxes if their net earnings hit $400 or more. Always consider age and filing status, as these can affect your thresholds. How Do I Know When I Need to Pay Taxes? To know when you need to pay taxes, keep track of your income throughout the year. If you’re an employee, your employer usually withholds taxes, but if you’re self-employed or have other income, you may need to make estimated payments. Pay attention to deadlines: April 15, June 15, September 15, and January 15. Use the IRS Tax Withholding Estimator to determine your obligations and avoid penalties for late payments. How Do I Know When I Have to Pay My Taxes? You’ll know when to pay your taxes by keeping track of your income and any tax withholdings. If you’re an employee, your employer withholds taxes from your paycheck. If self-employed, you should make estimated payments quarterly. Pay attention to deadlines: April 15, June 15, September 15, and January 15. Use tools like the IRS Tax Withholding Estimator to determine your payment amounts, ensuring you comply with tax regulations throughout the year. At What Point Do You Need to Pay Taxes? You need to pay taxes as you earn income throughout the year. Employers usually withhold taxes from your paycheck, but if you’re self-employed, you must make estimated quarterly payments if you expect to owe $1,000 or more at tax time. These payments are due on specific dates: April 15, June 15, September 15, and January 15. Conclusion In conclusion, grasping tax deadlines is essential for both individuals and businesses to avoid penalties. Remember key dates like April 15 for federal income tax returns and estimated payments. If you miss a deadline, consider filing for an extension, but be aware that it doesn’t extend your payment due date. Explore various payment options to manage your tax obligations effectively. Staying informed about both state and federal deadlines will help guarantee compliance and prevent unnecessary financial complications. Image via Google Gemini and ArtSmart This article, "When Do I Pay Tax?" was first published on Small Business Trends View the full article

-

Improving your customer service skills is crucial for creating better client interactions and increasing satisfaction. By focusing on empathy, effective communication, and problem-solving, you can address customer needs more efficiently. Time management and a positive attitude likewise play critical roles in your approach. Furthermore, enhancing your product knowledge and practicing active listening will further raise your service quality. Let’s explore these seven strategies in detail to help you excel in customer service. Key Takeaways Embrace empathy by acknowledging customer frustrations and personalizing interactions to build rapport and trust. Sharpen communication skills by using clear, jargon-free language and practicing active listening for better understanding. Develop problem-solving abilities by identifying root causes and crafting customized solutions through critical thinking and active listening. Manage time wisely by setting personal goals for call duration and prioritizing urgent tasks to enhance workflow efficiency. Stay positive and resilient to improve customer satisfaction and maintain composure during difficult interactions, fostering a loyal customer base. Embrace Empathy Empathy plays a crucial role in improving customer service skills. When you embrace empathy, you enhance your client service skills, transforming interactions into meaningful connections. Studies reveal that 70% of consumers are more willing to spend with companies that show comprehension and care for their needs. By actively acknowledging and validating customer frustrations, you can turn negative experiences into positive ones, nurturing loyalty. Using empathetic phrases, like “I can see why that would be frustrating,” builds rapport and trust, leading to higher satisfaction ratings. In fact, emotionally intelligent interactions can boost customer satisfaction by 50%. Personalizing interactions by relating to customers’ emotions shifts conversations from transactional to relational, which in the end improves retention rates. Sharpen Communication Skills Effective communication is a cornerstone of exceptional customer service. To sharpen your communication skills, focus on these key areas: Use simple, jargon-free language to improve clarity and comprehension. Practice active listening to fully engage with customer concerns and reflect their issues. Maintain a calm and friendly tone to ease customer anxiety. These customer service soft skills highlight the importance of good customer service. When you communicate effectively, you prevent confusion and nurture a positive relationship with your customers. Remember, 70% of consumers are willing to spend more for great service, so it’s essential to prioritize clarity. By encouraging follow-up questions at the end of conversations, you can clarify any remaining doubts, ensuring their needs are met. Implementing these ways to improve customer satisfaction will lead to better interactions and a more loyal customer base. Develop Problem-Solving Abilities Even though sharpening your communication skills lays a solid foundation for customer interactions, developing strong problem-solving abilities is just as important in delivering exceptional service. Effective problem-solving relies on critical thinking to quickly identify the root causes of customer complaints, enhancing resolution efficiency and customer satisfaction. Familiarity with common customer issues enables you to offer effective solutions swiftly, reducing wait times and improving overall service quality. Actively listening to customer needs is essential for determining the source of problems, allowing you to craft customized solutions that meet their expectations. Role-playing various scenarios during training builds confidence and hones your customer care skills, preparing you for challenging interactions. Manage Time Wisely Managing time wisely is vital in customer service, as it directly impacts both response times and service quality. By mastering effective time management techniques, you can greatly improve your customer service skills. Here are some strategies to contemplate: Set personal goals for call duration to streamline workflow and reduce wait times. Prioritize urgent tasks to address important customer issues quickly, boosting overall service efficiency. Use techniques like the Pomodoro Technique to maintain focus during busy periods, allowing for efficient inquiry handling. Listening fully to customers before responding additionally plays an important role in managing interaction times. By doing so, you not only improve comprehension but also create a better experience for both yourself and the customer. Implementing these methods can lead to quicker responses and improved service quality, eventually helping you to refine your customer service skills effectively. Stay Positive and Resilient Staying positive and resilient during customer interactions is crucial for improving customer satisfaction and loyalty. A positive attitude not just creates a welcoming atmosphere but also encourages customers to return. When faced with frustrated customers, resilience helps you manage stress and maintain composure, turning challenges into opportunities for positive outcomes. Benefits of Positivity How Resilience Helps Increases customer satisfaction Manages stress effectively Cultivates customer loyalty Maintains composure during conflict Improves team morale and performance Builds trust with customers Studies show that employees with a positive mindset are more productive, which translates into better service delivery. By nurturing a culture of positivity within your team, you can improve overall performance, leading to better customer service experiences and higher retention rates. Embrace positivity and resilience to enhance your customer interactions. Enhance Product Knowledge Having a strong comprehension of your products is essential for delivering excellent customer service. When you improve your product knowledge, you’re not just advancing your customer service abilities; you’re likewise boosting customer satisfaction. Here are some effective ways to build your knowledge as a customer service employee: Engage in continuous training to stay updated on product features and benefits. Review customer feedback regularly to understand common issues and improve solutions. Collaborate with experienced product specialists during onboarding for deeper insights. Practice Active Listening Building a solid foundation of product knowledge can greatly improve your ability to connect with customers, but it doesn’t stop there. Practicing active listening is vital for enhancing your customer service skills. This means fully engaging with customers, allowing them to express their concerns without interruption. By reflecting back what customers say, you show that you understand their issues, which can greatly boost customer satisfaction. Summarizing their concerns after they’ve explained them guarantees clarity and may reveal underlying problems. Studies suggest that employees who actively listen can improve customer satisfaction scores by up to 20%. Incorporating these skills into your interactions leads to more effective problem-solving and quicker resolutions. In the end, this promotes a respectful environment that can increase customer loyalty and create a positive impression of your service. Frequently Asked Questions What Can I Do to Improve My Customer Service Skills? To improve your customer service skills, start by practicing empathy; acknowledging customer feelings can greatly improve satisfaction. Focus on clear communication, simplifying complex ideas without jargon, since most customers appreciate clarity. Engage in role-playing to boost your problem-solving abilities, as this builds confidence in handling issues. Prioritize tasks effectively to manage time, reducing customer wait times. Finally, commit to continuous product training, enabling you to provide informed and quicker support. What Are the 7 R’s of Customer Service? The 7 R’s of customer service are crucial for creating a positive experience. They include Responsiveness, which focuses on timely replies; Reliability, ensuring consistent service; Relationship, building connections with customers; Respect, treating customers with dignity; Resolution, effectively addressing issues; Recognition, acknowledging loyal customers; and Reinforcement, nurturing ongoing loyalty. What Is the 10 to 10 Rule in Customer Service? The 10 to 10 Rule in customer service states that you should respond to customer inquiries within 10 minutes and aim to resolve their issues in the same timeframe. This approach is vital since 90% of customers prefer instant replies, which boosts their loyalty and satisfaction. What Are the 4 P’s That Improve Customer Service? The four P’s that improve customer service are personalization, proactivity, patience, and positive language. Personalization tailors your approach to meet individual customer needs, enhancing satisfaction. Proactivity involves anticipating customer issues, addressing them before they escalate. Patience is essential, especially with frustrated customers, as it nurtures trust. Finally, using positive language encourages a solution-focused dialogue, improving customer perceptions and experiences. Together, these elements create a more effective and enjoyable customer service environment. Conclusion Improving your customer service skills is crucial for enhancing client interactions and overall satisfaction. By embracing empathy, sharpening communication skills, and developing problem-solving abilities, you can address customer needs more effectively. Managing your time wisely and maintaining a positive attitude further contribute to a better service experience. Furthermore, enhancing your product knowledge and practicing active listening will guarantee you meet client expectations. Implement these strategies to cultivate a more productive and satisfying customer service environment. Image via Google Gemini and ArtSmart This article, "7 Proven Ways to Improve Customer Service Skills" was first published on Small Business Trends View the full article

-

Greg Abel to address shareholders at first gathering since he succeeded Warren BuffettView the full article

-

Alphabet and Microsoft earnings show search ad revenue growing while Google Network revenue fell to $6.97B, continuing a multi-quarter decline. The post What Google & Microsoft Earnings Say About Search appeared first on Search Engine Journal. View the full article

-

In relation to small business accounting, choosing the right format is vital for your financial health. A simplified chart of accounts can help you categorize your transactions effectively, covering fundamental areas like assets, liabilities, and expenses. This streamlined approach not only improves your reporting efficiency but additionally supports better cash management. Comprehending how to structure your accounting can lead to more informed decision-making, and there are several strategies you can adopt to refine your processes. Key Takeaways Utilize a simplified chart of accounts with around 20 accounts to enhance reporting efficiency and simplify financial tracking. Implement a double-entry bookkeeping system to ensure accuracy by recording each transaction in at least two accounts. Regularly update financial statements to provide clear snapshots of your business’s financial health over specific periods. Use cloud-based accounting software and customizable templates for real-time data access and improved organization of financial records. Monitor income and expenses with cash flow templates to identify spending patterns and make informed budget adjustments. Understanding the Basics of Small Business Accounting When you plunge into small business accounting, it’s essential to grasp the foundational concepts that govern financial tracking and reporting. Start by comprehending the chart of accounts, which categorizes transactions into assets, liabilities, equity, income, and expenses. Familiarize yourself with basic accounting principles like the double-entry system, ensuring every transaction is recorded in at least two accounts to maintain balance. Regularly updated financial statements, such as balance sheets and income statements, provide a snapshot of your financial health over specific periods. To streamline your bookkeeping process, consider using accounting spreadsheet templates or small business accounting templates. Tools like a monthly cash flow template, cash flow statement template, or even a simple cash flow template in Excel can help you track income and expenses efficiently. Moreover, utilizing a financial forecast template and a balance sheet template in Excel can assist in keeping your records compliant with accounting standards and tax regulations. The Importance of a Simplified Chart of Accounts A simplified chart of accounts is essential for small businesses as it organizes financial transactions into five key categories: assets, liabilities, equity, income, and expenses. This streamlined approach not only improves reporting accuracy but likewise makes tracking your financial performance much easier. Streamlined Financial Tracking Establishing a streamlined Chart of Accounts (CoA) is vital for small businesses aiming to improve their financial tracking. A simplified CoA typically includes around 20 accounts, categorizing financial transactions into assets, liabilities, equity, income, and expenses. This organization improves reporting efficiency and helps you generate important documents like the cash flow statement template excel or balance sheet format in excel. Account Type Description Example Assets Resources owned Inventory Liabilities Obligations owed Accounts Payable Equity Owner’s investment Retained Earnings Income Earnings from operations Sales Revenue Expenses Costs incurred Rent Expense Enhanced Reporting Accuracy To achieve improved reporting accuracy, small businesses must prioritize a simplified Chart of Accounts (CoA) that categorizes financial transactions effectively. By structuring your CoA into five main categories—assets, liabilities, equity, income, and expenses—you’ll improve clarity and ease of reporting. This streamlined approach allows you to better track revenue trends and expenses, leading to more accurate financial insights. Implementing a standardized numbering system simplifies organization, making it easier to generate comparative analyses. With a limited CoA of around 20 accounts, you can avoid overwhelming complexity. Utilizing tools like a cash flow report template, general ledger template excel, or business budget template excel will further aid in efficient report generation, ultimately ensuring your financial statements reflect your company’s true performance. Key Components of an Effective Accounting Format An effective accounting format serves as the backbone of financial management for small businesses, enabling clear tracking and analysis of financial activities. A systematic Chart of Accounts categorizes transactions into assets, liabilities, equity, income, and expenses, which simplifies financial tracking. Utilizing standard templates like a balance sheet example excel and cash flow statement format xls can maintain organized records. Incorporating automatic calculations in your accounting spreadsheet reduces manual errors and improves the accuracy of your financial data. Regularly updated records, such as a daily cash flow template excel or bookkeeping spreadsheet, provide essential insights into cash flow and trends. Moreover, using a general ledger template can facilitate compliance with tax regulations and support easier audit preparation. For convenience, you might consider cash flow excel template free download and free accounting spreadsheet templates for small business to streamline your financial management processes effectively. Categorizing Financial Transactions Categorizing financial transactions is an essential step in maintaining organized and accurate financial records for small businesses. By placing transactions into specific accounts within your chart of accounts, you can streamline your financial management. Typically, this includes assets, liabilities, equity, income, and expenses. Using an accounting sheet template or a bookkeeping journal template can help simplify this process. A simple bookkeeping template can likewise aid in organizing data effectively. Implementing a standard numbering system improves efficiency and helps in generating reports like a cash flow statement example excel or balance sheet example xls. This categorization allows you to track financial performance, identify trends, and make informed decisions. For instance, an accounts receivable report template excel free Microsoft can provide insights into cash flow management. Tracking Assets, Liabilities, and Equity Comprehending how to track assets, liabilities, and equity is vital for any small business owner. A balance sheet template is important as it categorizes assets into current and non-current, giving you a clear picture of what your business owns. By using a small business bookkeeping template excel free, you can regularly update your balance sheet, which helps you monitor changes effectively. Liabilities are likewise divided into current and long-term, showing what you owe and aiding in evaluating financial obligations. Furthermore, equity reflects your investment in the business and retained earnings, indicating overall financial health. Consider utilizing an accounting general ledger template and a cash flow statement sheet to maintain accurate records. You might as well find a free balance sheet template or a sample balance sheet format excel useful to streamline your tracking process. In the end, keeping these records helps you make informed financial decisions for your business. Monitoring Income and Expenses Monitoring income and expenses is essential for the financial health of your small business. You can use a cash flow spreadsheet or a cash flow template Excel to streamline your tracking of cash transactions. These tools offer automatic calculations for subtotals and total cash balances, making it easier to manage your finances. Regularly categorizing expenses helps you identify spending patterns, guiding informed decisions about budget adjustments. Implementing an accounts receivable template allows you to track outstanding invoices, reducing the risk of overdue accounts and improving your cash flow management. Aim to reconcile your income and expenses at least quarterly to guarantee accurate transaction records. This practice is important for financial reporting and tax preparation. Utilizing a monthly income sheet, along with accounting sheets for small business and free bookkeeping templates, can boost your monitoring process considerably, leading to a clearer financial projection template for your future planning. Creating Essential Financial Statements To effectively manage your small business’s financial health, creating and regularly updating financial statements is vital. You should focus on three key documents: the balance sheet, income statement, and cash flow statement. The balance sheet template summarizes your assets, liabilities, and equity at a specific point, giving you a snapshot of financial stability. Meanwhile, the income statement in a monthly format details revenues and expenses, helping you evaluate profitability. Finally, the cash flow statement tracks cash inflows and outflows, ensuring you understand how well you’re managing cash to fund operations. Utilize tools like the cash flow spreadsheet in Excel or a simple balance sheet format to streamline the process. An accounting journal template can additionally aid in organizing your financial data. Regularly updating these statements allows for informed decision-making and effective financial planning, making a small business cash flow template invaluable for tracking performance and preparing financial projections. Utilizing Bookkeeping Templates for Efficiency During managing a small business, utilizing bookkeeping templates can greatly improve your efficiency and organization. These templates streamline financial management by providing pre-designed structures for tracking income, expenses, and cash flow. For instance, a cash flow template xls helps you visualize your cash flow spreadsheet, making it easier to assess your financial health. You can find free excel bookkeeping templates that include sample balance sheet template excel and simple accounting spreadsheets, which simplify data entry and calculation. By using excel templates for business, you can customize the tools to meet your specific needs as well as ensuring compatibility across platforms. Many business bookkeeping templates come with built-in formulas and charts, allowing you to automate calculations and visually represent financial trends. This organization not just facilitates tax preparation but additionally improves your ability to monitor cash flow effectively, in the end aiding in better decision-making for your business’s future. Cash Management and Its Role in Accounting Cash management plays a crucial role in the accounting practices of small businesses, directly influencing their financial stability and operational efficiency. By tracking and optimizing cash flow, you guarantee that your business has enough liquidity to meet obligations. Using cash management templates like a cash flow spreadsheet or a cash projection template in Excel simplifies monitoring. Regularly analyzing a cash statement format in Excel helps identify cash trends, which aids in financial planning and decision-making. You might also find a cash flow chart Excel beneficial for visualizing your cash movements. Utilizing free accounting software in Excel can streamline your bookkeeping processes. Furthermore, having a solid basic bookkeeping template can automate calculations, providing a clearer financial picture. Strong cash management practices improve your ability to secure financing, as lenders often evaluate your cash flow stability before approving loans. By implementing these tools and strategies, you can strengthen your financial foundation. Expense Tracking and Budgeting Best Practices Effective expense tracking and budgeting are essential for maintaining financial health in any small business, as they provide the framework for comprehending where your money goes and how to plan for future expenses. Here are some best practices to follow: Use a small business excel template for organizing expenses. Implement a cash flow template excel to monitor cash movements. Regularly compare planned versus actual expenses for improved financial decision-making. Establish a template for ledger sheet customized to your business’s needs. Utilize a company budget template excel for automatic calculations and forecasts. The Benefits of Regular Financial Reporting Regular financial reporting is crucial for small businesses, as it provides timely insights into your financial health and helps you make informed decisions. By utilizing tools like a cash flow spreadsheet or an account balance spreadsheet, you can track your financial status effectively. A monthly cash flow template allows you to manage cash flow and forecast future performance. Regular reporting, using a financial ledger template or a template income and expenditure statement, helps identify budget variances, enabling you to allocate resources more efficiently. Furthermore, accessing sample income and expense statements can guide you in comprehending your profits and losses. Employing a free accounting program in Excel simplifies this process further. Overall, regular financial reporting promotes transparency and accountability, enhancing trust with stakeholders and ensuring compliance with tax regulations. Aim for at least quarterly reports to maintain accurate financial records and make timely adjustments to your business strategies. Leveraging Technology in Small Business Accounting In today’s fast-paced business environment, leveraging technology in accounting can greatly streamline your financial management. By adopting cloud-based accounting software, you gain access to real-time data and the ability to collaborate with your accountant from anywhere. Furthermore, automated reporting solutions can save you time and reduce errors, allowing you to focus on growing your business instead of getting bogged down in manual processes. Streamlined Financial Management Tools Streamlined financial management tools are essential for small businesses looking to improve their accounting practices. By leveraging technology, you can boost accuracy and efficiency in your financial processes. Consider using: Free Excel bookkeeping software to manage your finances easily. Customizable templates and dashboards for quick insights into your financial health. An excel template for accounting to maintain organized records. A business ledger template to track income and expenses effectively. Automated financial management tools, like a statement of account template, to simplify invoicing and expense tracking. These solutions not only reduce manual entry errors but also allow for real-time access to financial data, facilitating informed decision-making and strategic planning in your small business. Automated Reporting Solutions Automated reporting solutions play a crucial role in transforming how small businesses manage their financial data, especially as they seek to improve accuracy and efficiency. By utilizing these tools, you can streamline financial data collection and generate real-time reports with minimal manual input. This not only improves accuracy but also greatly reduces time on financial reporting by up to 75%. With cloud-based accounting software, you gain access to cash flow insights, expenses, and profitability metrics through customizable dashboards. Many automated reporting solutions integrate seamlessly with existing systems like QuickBooks or Xero, helping you monitor key performance indicators (KPIs) effortlessly. Cloud-Based Accounting Software As small businesses increasingly embrace technology, cloud-based accounting software has emerged as a crucial tool for managing financial operations more effectively. This software enables you to access your financial data from anywhere, enhancing real-time collaboration with remote teams. Here are some key benefits: Automatic updates and backups to prevent data loss Integration with other business tools, like CRM and invoicing software Cost-effective subscription models, eliminating hefty upfront costs Improved cash flow management with real-time expense tracking Access to various templates, including balance sheet and bank statement template excel Utilizing cloud accounting can simplify your bookkeeping forms and streamline processes, making it easier to manage your finances efficiently. Consider exploring options like full accounting in Excel format free download to complement your cloud solutions. Tips for Streamlining Your Accounting Processes Effective accounting processes are essential for small businesses seeking to improve financial management and reduce errors. Start by using standardized excel sheet templates, like a balance worksheet template or a free balance sheet sample, to keep records organized. Implement a company budget format in Excel for better financial planning. Regularly generate a sales report template in Excel to track revenue effectively. Consider utilizing a printable bookkeeping template and a ledger template to streamline daily transactions. Adopting a statement of account format in Excel helps clarify outstanding payments. Automating invoicing and expense tracking through integrated solutions minimizes manual entry, saving time, and reducing errors. Finally, verify you reconcile accounts regularly, which aids in identifying discrepancies early, guaranteeing compliance and accuracy in your financial reporting. Frequently Asked Questions What Accounting Software Is Best for Small Businesses? When choosing accounting software for your small business, consider options like QuickBooks, Xero, and FreshBooks. Each offers features like expense tracking, invoicing, and tax preparation. QuickBooks is user-friendly and widely used, whereas Xero provides strong online collaboration tools. FreshBooks, in contrast, thrives in invoicing and time tracking. Evaluate your specific needs, budget, and the software’s scalability to guarantee it meets your business’s growth and operational requirements effectively. How Often Should I Review My Financial Statements? You should review your financial statements at least monthly. This regular check helps you identify trends, expenses, and areas for improvement. By staying on top of your finances, you can make informed decisions about budgeting and investments. Moreover, quarterly reviews are crucial for evaluating your financial health over a longer period. If your business experiences significant changes, consider reviewing your statements more frequently to adapt to new circumstances effectively. Do I Need a Professional Accountant for My Small Business? You don’t necessarily need a professional accountant for your small business, but having one can be advantageous. If your financial situation is complex or you’re unfamiliar with tax laws, an accountant can help you navigate these challenges. They can likewise save you time and guarantee compliance. Nonetheless, if your finances are straightforward, you might manage with accounting software or basic financial knowledge. Evaluate your needs to determine the best approach for your situation. How Can I Reduce Accounting Costs for My Business? To reduce accounting costs for your business, consider using accounting software to automate tasks like invoicing and expense tracking. You can likewise streamline your processes by organizing receipts and financial documents digitally, which saves time and reduces errors. Furthermore, training your staff to handle basic accounting tasks can cut down on professional fees. Regularly reviewing your financial reports helps identify potential savings and guarantees you’re not overspending on unnecessary services. What Are Common Accounting Mistakes Small Businesses Make? Common accounting mistakes small businesses make include failing to keep accurate records, which can lead to financial discrepancies. Not reconciling bank statements regularly creates confusion about cash flow. Additionally, neglecting to track expenses can result in lost deductions. Many entrepreneurs underestimate the importance of separating personal and business finances, causing complications during tax season. Finally, not utilizing accounting software can hinder efficiency and accuracy in financial reporting, affecting decision-making and growth potential. Conclusion In conclusion, adopting a simplified chart of accounts is crucial for small businesses to maintain financial clarity and efficiency. By categorizing transactions into key areas and utilizing technology, you can streamline your accounting processes and improve decision-making. Regular financial reporting and reconciliations guarantee compliance as well as providing valuable insights into your business’s performance. Implementing these best practices will not just help you manage your finances effectively but will additionally support your overall business growth. Image via Google Gemini This article, "Best Accounting Format for Small Businesses?" was first published on Small Business Trends View the full article

-

The veteran senator is one of the most hawkish Republicans with influence over the US presidentView the full article

-

Heidi O’Neill is having a tough week. In late April, the Lululemon board announced it had ended its monthslong search to replace CEO Calvin McDonald, who left the company abruptly in 2025 after six years at the helm. As soon as the company announced that O’Neill, a 26-year Nike veteran, would be taking on the position, things got messy. Lululemon’s stock took a plunge, suggesting that investors didn’t think O’Neill was the right pick. And many analysts—including myself—argued that following the Nike playbook would not lead Lululemon out of its financial doldrums. Then, Lululemon founder Chip Wilson weighed in. Wilson launched the company in 1998 as a yoga brand and left in 2005, but he has never stopped trying to stay involved, and he still wields considerable power at the company as its largest shareholder. He had made it clear that he didn’t approve of McDonald’s leadership, and in a LinkedIn post, he went after the board for choosing O’Neill, arguing they should be looking for “passionate, creative renegades who have a vision that will shake up the status quo.” Wilson’s judgment is not always right. This is someone who once had to apologize for saying that women’s thighs rubbing together was responsible for the pilling on Lululemon leggings—a comment widely perceived to be body shaming. And last year he criticized Lululemon’s diversity, equity, and inclusion policies for welcoming customers “you don’t want . . . coming in.” But that doesn’t mean his instincts are always wrong. What Lululemon needs right now is the kind of revitalization we’re seeing at Gap—and it’s worth paying attention to how that brand pulled it off. The legacy apparel brand, founded in 1969, had gone through several years of declining sales. But these days it’s having a moment. Over the past two years, it has had hit marketing campaigns every season, tapping stars like Young Miko, Troye Sivan, and, most notably, Katseye. Zac Posen has created a high-fashion version of the Gap label called GapStudio, which has put red-carpet garments on the backs of celebrities like Timothée Chalamet and Anne Hathaway. The brand has also launched collaborations with Béis, Dôen, and, most recently, Victoria Beckham, all huge hits. While this kind of turnaround is the stuff brands dream of, Mark Breitbard, president and CEO of the global Gap Brand, has made it clear that it’s the result of a lot of hard work. It has also required a deep knowledge of the brand. Breitbard is not a Gap outsider. Early in his career, from 2009 to 2013, he worked as the chief merchant at Old Navy and then Gap, and later came back in 2017 to run Banana Republic. When he took on his current role in 2020, he inherited a mess. The brand had too many stores, many of them unprofitable. It also had too much inventory, which resulted in heavy discounting. The quality of clothing had declined. “The business was broken,” Breitbard told me recently. “We had to address each of these issues with discipline. It wasn’t fun, but it laid the foundation for us to bring the brand back into the center of culture.” Product, he points out, is crucial. Despite its long history as a beloved maker of basics, Gap’s clothes had lost their luster. Breitbard, who is steeped in supply chains and merchandising, worked to improve the quality of the materials and fit. And consumers are responding. After the Katseye video, which featured retro denim styles, people rushed to Gap to buy ’90s-style jeans—and they weren’t disappointed. During Coachella, Gap created an activation focused on sweats, and people loved how cozy they were. This is an important lesson for Lululemon. The brand has always been known for its unique fabrics, developed out of its internal design philosophy, which it calls “the science of feel.” It has had many blockbusters, including its proprietary buttery-soft Nulu fabric, which is in its famous Align pants, which have generated more than $1 billion for the company. Lululemon customers come to the brand for its high quality and reputation for innovation, and its new leader must be laser-focused on product. Once this pillar is in place, it’s possible to bring the brand back into the cultural conversation. It’s notable that Breitbard didn’t start pushing out these creative campaigns for Gap five years ago; he waited until he believed the foundations of the business were in order. Only then did he turn his attention to launching some of the most exciting marketing campaigns we’ve seen recently. When I interviewed him for Fast Company’s Most Innovative Companies podcast, Breitbard said he empowers his creative team to do what they do best. This includes Fabiola Torres, the CMO he brought on in May 2024. “If we have amazing creatives, and we put them in a position where we can trust the creatives to keep pushing and driving, and not overburden them with bureaucracy, we will stay in this moment of heat,” he says. This is exactly the kind of creativity Wilson is hoping for. And it’s unclear whether O’Neill is the right person for the task. In recent years, she has been focused on more technical parts of the business, which is not a bad thing, except she was responsible for helping Nike pivot toward a direct-to-consumer approach that has proved lacking for the company. And when it comes to creative, Nike’s heyday as an engine for brilliant advertising and marketing is long gone. Gap proved that legacy brands can come roaring back—but only with the right leader at the helm. Whether O’Neill is that person for Lululemon remains to be seen. She’ll have plenty to prove, assuming the board doesn’t have second thoughts. View the full article

-

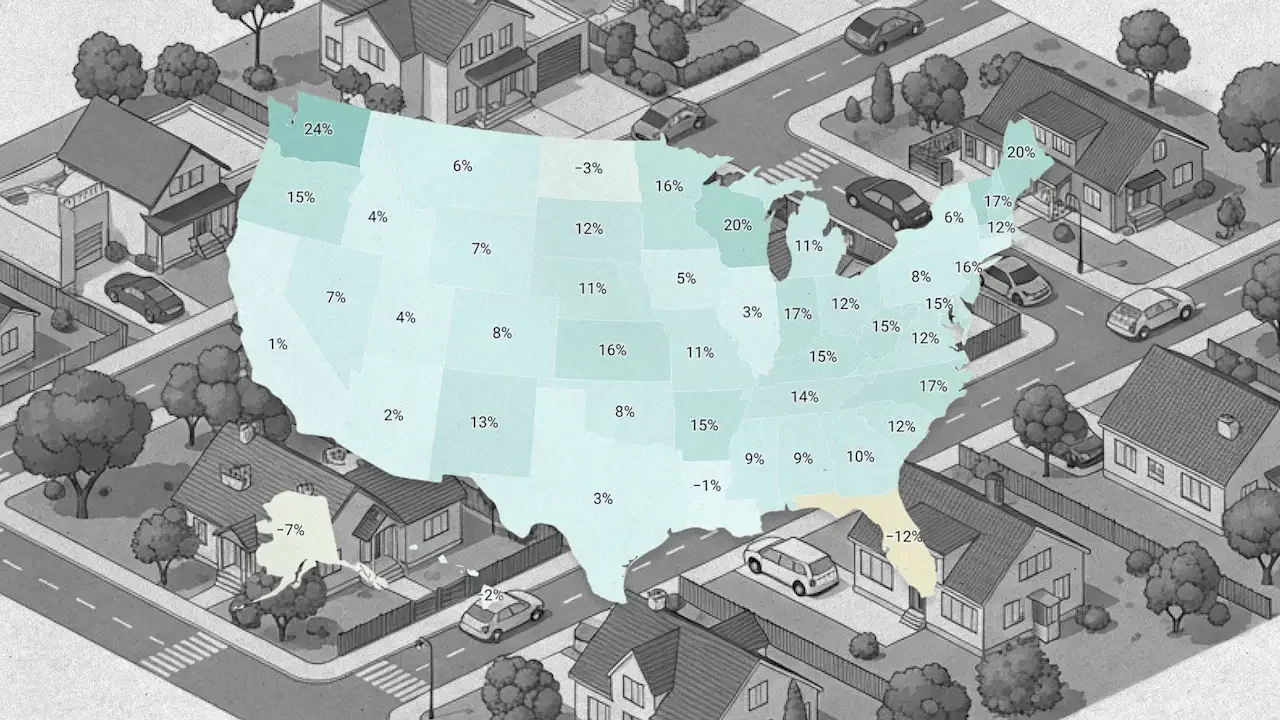

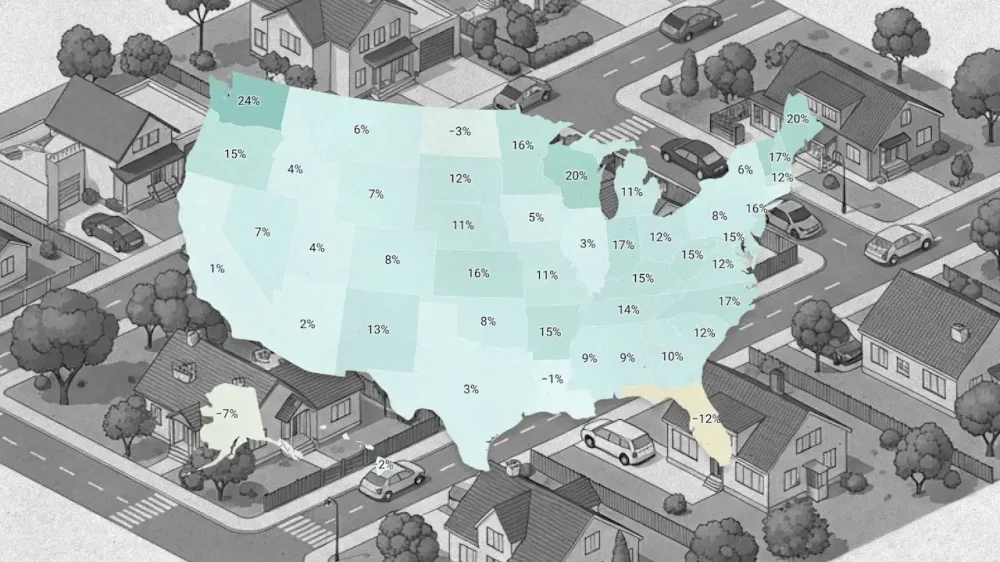

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. When assessing home price momentum, ResiClub believes it’s important to monitor active listings and months of supply. If active listings start to increase rapidly as homes remain on the market for longer periods, it may indicate pricing softness or weakness. Conversely, a rapid decline in active listings beyond seasonality could suggest a market where sellers are gaining power. Since the national pandemic housing boom fizzled out in 2022, the power dynamic has slowly been shifting directionally from sellers to buyers. Of course, that shift has varied across the country. Generally speaking, local housing markets where active inventory has jumped above pre-pandemic 2019 levels have experienced softer home price growth (or outright price declines) over the past 47 months. Conversely, local housing markets where active inventory remains far below pre-pandemic 2019 levels have, generally speaking, experienced, relatively speaking, more resilient home price growth over the past 47 months. Where is national active inventory headed now? While national active inventory is still up year over year, the pace of growth has slowed in recent months as softening has slowed. National active listings are up 4.6% on a year-over-year basis from April 30, 2025, to April 30, 2026, according to Realtor.com’s inventory data. But if you go back 12 months, that year-over-year national inventory growth rate was much higher (+30.6%). After a period in which leverage shifted more toward homebuyers, the supply-demand equilibrium in the nationally aggregated housing market has been more stable in recent months. Nationally, we’re still below pre-pandemic 2019 inventory levels (-11.8% below April 2019) and some resale markets, in particular chunks of the Midwest and Northeast, still remain tightish, relatively speaking. April inventory/active listings total, according to Realtor.com: April 2017 -> 1,198,424 April 2018 -> 1,102,064 April 2019 -> 1,137,198 April 2020 -> 941,733 April 2021 -> 435,663 (pandemic housing boom overheating) April 2022 -> 379,978 (pandemic housing boom overheating) April 2023 -> 562,966 April 2024 -> 734,318 April 2025 -> 959,251 April 2026 -> 1,002,935 If we maintain the current year-over-year pace of inventory growth (+43,684 homes for sale), we’d have 1,046,619 active inventory come April 2027. (Note: That’s not a prediction—I’m just showing what the math looks like if that pace continues.) Below is the year-over-year active inventory percentage change by state. While active housing inventory is rising in most markets on a year-over-year basis, the pace of growth continues to decelerate across much of the country (see the side-by-side maps below). In fact, Florida—home to many of the weakest regional housing markets over the past two years—is now seeing active inventory edge down a little year over year (-12%). Above, left: Year-over-year active inventory shift from April 2024 to April 2025 Above, right: Year-over-year active inventory shift from April 2025 to April 2026 And while active housing inventory is rising in most markets on a year-over-year basis, some markets still remain tightish. As ResiClub has been documenting, both active resale and new homes for sale remain the most limited across huge swaths of the Midwest and Northeast. That’s where home sellers in the spring/summer are likely, relatively speaking, to have more power than their peers in many Southern markets. Active inventory in April 2026 compared to pre-pandemic April 2019: Southwest —> +23% West —> +3% Southeast —> -2% Midwest —> -35% Northeast —> -50% In contrast, active housing inventory for sale has neared or surpassed pre-pandemic 2019 levels in many parts of the Sunbelt and Mountain West, including metro area housing markets such as Punta Gorda, Florida, and Austin. Many of these areas saw major price surges during the pandemic housing boom, with home prices getting stretched compared to local incomes. As pandemic-driven domestic migration slowed and mortgage rates rose, markets like Punta Gorda and Austin faced challenges, relying on local income levels to support frothy home prices. This softening trend was accelerated further by an abundance of new home supply in the Sunbelt. Builders are often willing to lower prices or offer affordability incentives (if they have the margins to do so) to maintain sales in a shifted market, which also has a cooling effect on the resale market, with some buyers, who would have previously considered existing homes, opting for new homes with more favorable deals over the past couple years. That then puts some additional upward pressure on resale inventory. Click here to view an interactive version of the map below. At the end of April 2026, 12 states were above pre-pandemic 2019 active inventory levels: Alabama, Arizona, Colorado, Florida, Hawaii, Idaho, Nebraska, Nevada, North Carolina, Oklahoma, Oregon, Tennessee, Texas, Utah, and Washington. (The District of Columbia—which we left out of the table below—is also back above pre-pandemic 2019 active inventory levels.) The big picture Over the past several months, the post-boom softening has lost momentum, and inventory growth has decelerated on a year-over-year basis. That said, the nationally aggregated housing market remains soft. While home prices are declining in some parts of the Sunbelt, a large share of Northeast and Midwest markets are still eking out modest year-over-year gains. At the national level, home prices are essentially flat year over year. Below is another version of the table; this one includes every month since January 2017. If you’d like to examine the monthly state inventory figures further, use the interactive chart below. Florida—which has been the epicenter of housing market weakness over the past two years, particularly in Southwest Florida—is no longer seeing the upward burst in inventory. Indeed, the intensity of Florida’s housing market correction is easing across many pockets of the state. Click here to view a sortable version of the chart below. View the full article

-

Anil Menon might have the world’s spaciest resume. After several years as a NASA flight surgeon, he became SpaceX’s medical director in 2018, where he authored research on the effects of space on the human body. In 2021, he was selected as a NASA astronaut and has spent the past several years training for his own journey to space. Along the way, he also supported his wife, Anna Menon, who traveled to space on a private mission in 2024 and was herself selected as a NASA astronaut last year. Somewhere in the margins, Menon has also served as an Air Force Reserve member and emergency room doctor. Now, he’s finally heading to space himself. This July, Menon will travel to Kazakhstan, where Russia’s space program conducts launches, and join two cosmonauts on the next mission to the International Space Station. He’ll fly aboard the storied Russian Soyuz crew vehicle, which has been used successfully for decades, and is expected to spend eight months aboard the station. For years, NASA and Roscosmos, Russia’s space agency, have maintained the practice of placing astronauts and cosmonauts on one another’s missions. One side effect of that arrangement, and of the modern space age more broadly, is that Menon brings an unusually expansive perspective on life in space, with experience spanning NASA, Russia’s space program, and SpaceX, as well as a firsthand view of NASA’s distinct institutional role. “NASA kind of bridges the gap between some of these different cultures and synthesizes it,” he says. “As we look at the moon, everyone is going to pursue that as well. I think that NASA is this great synergy for all of that.” Fast Company spoke with Menon about his upcoming mission, the future of commercial space stations, and the biggest unanswered questions surrounding microgravity’s effects on the human body. This interview has been edited for clarity and length. Can you talk a little bit about the differences between the Soyuz and the Crew Dragon? The Soyuz was developed for some of the first space flights and it’s got this long heritage tracing back to what we consider the space race. They’ve tried to keep things that work and just keep them working for high-reliability reasons. Some of the computers and screen layouts are things that are push-button… They work. The same goes for engines and some of the seats and comfort level. Most of the astronauts during the early Russian space program were shorter in stature, so someone who’s 6’1’’ like me doesn’t fit as well, but I fit… It works, and that’s the interesting thing. The spacesuit has a rubber pressure seal, and you twist it … and then you put a band around it to seal it—two bands—and that’s how you create your seal. It isn’t a zipper. It isn’t some locking mechanism, but it works. And it’s always worked. SpaceX, born in this era, is really pushing the frontiers of engineering and developing things. You’ll see more touch displays. It’s automated procedure sequences….you hit a button, and you get that procedure popping up for you with a lot of data flowing in, as you’d see in a sci-fi movie. It also works, and it’s a different way to tackle the problem, and it’s got some advantages. The suits: you zip them around and put them on… They look really cool, and they work really well. There are different sorts of engines —[where] the rocket itself lands—which adds usability. I’d say it’s pushing the frontiers of where we want to go with things, which is uniquely cultural to us in terms of the way we look at things. As a physician, what do you see as the biggest open questions about, like, the impact of space on the human body? We’ve done a lot of studies on through the International Space Station, but what open questions intrigue you as we think about going to the moon, and maybe Mars? I’ll answer that in a nebulous way and a very specific way. The more general answer is that there’s just so much new stuff. We’ve been flying healthy astronauts to space for a long time. We are going to be flying—and we are starting to fly—the whole spread of humans to space. You know, on Inspiration 4, Hayley Arceneaux had an osteosarcoma [bone cancer]. How does that change things? So there’s just a lot of unknown. At this point in time, in medicine, it’s not often you see totally new diseases, but we’re seeing new things in space. I think in the future, we’ll continue to see new things, and that’s probably like the biggest thing. If I were to just pick a specific thing for a concrete example, we’re seeing clotting happen in space in unexpected ways. You take a really healthy person, put them in space, there’s three things that increase your chance of a clot: One is injury, and that’s when your body, like closes the wound—[and] that’s normal. The other is stasis, which means if you just keep blood in a static spot, it’s going to clot. The other is like some element of hypercoagulability. If you take oral contraceptives for women, it makes you a little more prone to clotting. In space, what you’re getting is stasis on some level, so blood isn’t moving the same. You’re getting one cornerstone of that clotting triangle, and it just takes a little bit more to see something else. As you send more people up there, a lot of these diseases that are related to that [and] you’re just going to see more of them. That could be deep vein thrombosis, pulmonary embolism, strokes, things like that. We’ll have to figure out, like, what do we do about it? On the flip side, is there any promise or hope that there are health metrics that seem to improve in space compared to on Earth? You always see this in sci-fi, but if you have disabilities on Earth, maybe that goes away in space, right? You don’t need your legs in space, and so you can do a lot of things that you couldn’t do on Earth, which opens up the doors for a lot of people for whom that’s an issue. And I watch enough sci-fi movies that I’m hoping that I get a mutant gene while I’m up there and have some new superpower. I’m just kidding! We’re preparing for the next generation of commercial space stations that will eventually replace the ISS. What do you have in mind for what we could do differently or change? ISS is a great stepping stone to leverage to learn about our next step. I think the next step, a commercial space station, will also be a stepping stone to the future. So what are the things we do on ISS that we could do better on those would be really important science. Increase the throughput and make it easier for people to do science. On the ISS, that’s great, but you can always do things better. Letting people do real-time feedback on some of the science that they’re doing there. Experimenting with things that could open up the door to going to Mars and staying on the Moon. Looking at those things that kick off the orbital economy, like printing and developing those manufacturing processes. They want to make new chips up there, and that stimulates more jobs in space and doing stuff. Focusing on the high-yield things and then kicking them off are going to be transformative…Think about all the things that need to go into a data center that’s in space. Some of these future stations can lean into that and help carry out or fix that technology until it’s like something that you can just deliver and launch. View the full article

-