All Activity

- Today

-

Tehran says Donald The President ‘raised seven claims in one hour and all seven were false’View the full article

-

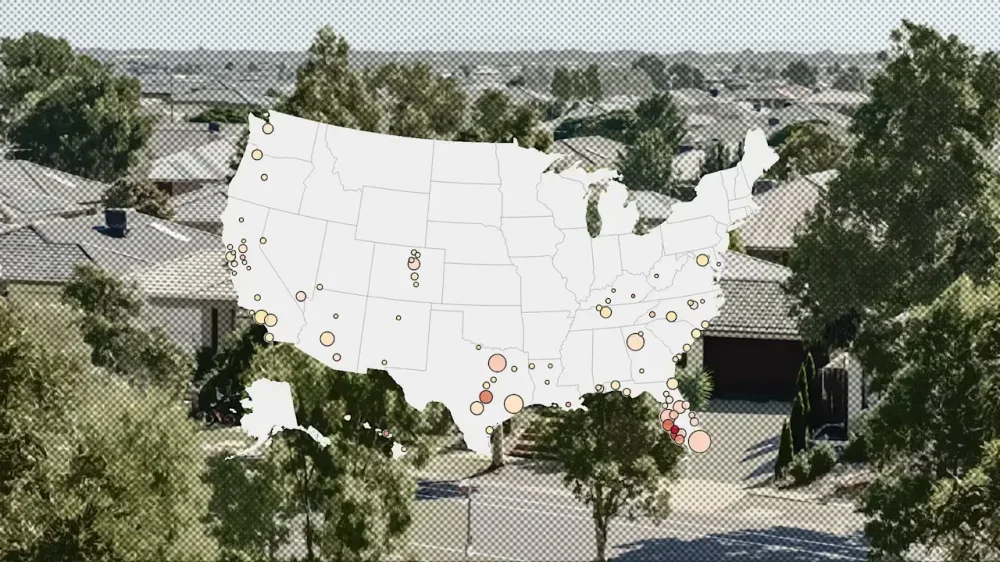

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. Based on our analysis of the Zillow Home Value Index, U.S. home prices are up just +0.8% year-over-year between March 2025 and March 2026. That marks a deceleration from the +1.2% growth rate a year earlier—though national year-over-year home price growth has recently stabilized, ticking a tad higher from a low of -0.01% in August 2025. In the first half of 2025, the number of major metro area housing markets seeing year-over-year declines climbed. That count has since stopped ticking up. 31 of the nation’s 300 largest housing markets (i.e., 10% of markets) had a falling year-over-year reading in the Jan. 2024 to Jan. 2025 window. 42 of the nation’s 300 largest housing markets (i.e., 14% of markets) had a falling year-over-year reading in the Feb. 2024 to Feb. 2025 window. 60 of the nation’s 300 largest housing markets (i.e., 20% of markets) had a falling year-over-year reading in the March 2024 to March 2025 window. 80 of the nation’s 300 largest housing markets (i.e., 27% of markets) had a falling year-over-year reading in the April 2024 to April 2025 window. 96 of the nation’s 300 largest housing markets (i.e., 32% of markets) had a falling year-over-year reading in the May 2024 to May 2025 window. 110 of the nation’s 300 largest housing markets (i.e., 36% of markets) had a falling year-over-year reading in the June 2024 to June 2025 window. 105 of the nation’s 300 largest housing markets (i.e., 36% of markets) had a falling year-over-year reading in the July 2024 to July 2025 window. 109 of the nation’s 300 largest housing markets (i.e., 35% of markets) had a falling year-over-year reading in the Aug. 2024 to Aug. 2025 window. 105 of the nation’s 300 largest housing markets (i.e., 35% of markets) had a falling year-over-year reading in the Sept. 2024 to Sept. 2025 window. 105 of the nation’s 300 largest housing markets (i.e., 35% of markets) had a falling year-over-year reading in the Oct. 2024 to Oct. 2025 window. 98 of the nation’s 300 largest housing markets (i.e., 33% of markets) had a falling year-over-year reading in the Nov. 2024 to Nov. 2025 window. 106 of the nation’s 300 largest housing markets (i.e., 35% of markets) had a falling year-over-year reading in the Dec. 2024 to Dec. 2025 window. 100 of the nation’s 300 largest housing markets (i.e., 33% of markets) had a falling year-over-year reading in the Jan. 2025 to Jan. 2026 window. 99 of the nation’s 300 largest housing markets (i.e., 33% of markets) had a falling year-over-year reading in the Feb. 2025 to Feb. 2026 window. 89 of the nation’s 300 largest housing markets (i.e., 30% of markets) had a falling year-over-year reading in the March 2025 to March 2026 window. As you can see above, in the first half of 2025, there was a notable increase in the number of housing markets slipping into year-over-year price declines as the supply–demand equilibrium (as measured by inventory) shifted more quickly toward homebuyers. Over the past eight months, however, the list of declining markets has begun to stabilize and inventory growth has also decelerated. Based on seasonally adjusted month-over-month prints, ResiClub expects the number of markets with year-over-year price declines to decrease more in the coming months. Home prices are still climbing a little year-over-year in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest. In contrast, some pockets in states like Texas, Florida, and Colorado—where active inventory exceeds pre-pandemic 2019 levels by a solid clip—are seeing modest home price pullbacks or flat pricing. Many of the housing markets seeing the most softness, where homebuyers have gained the most leverage, are primarily located in Sun Belt regions, particularly the Gulf Coast and Mountain West. Many of these areas saw even greater price surges during the Pandemic Housing Boom, with home price growth outpacing local income levels. As pandemic-driven domestic migration slowed and mortgage rates rose in 2022, markets like Tampa and Austin faced challenges, relying on local income levels to support frothy home prices. That Sun Belt softening was further compounded by an abundance of new home supply in the Sun Belt. Builders are often willing to lower prices or offer affordability incentives to maintain sales, which also has a cooling effect on the resale market. As a result, some buyers who might have previously opted for existing homes are instead choosing new construction with more attractive deals—which added further upward pressure to resale inventory growth over the past few years. Of course, while 89 of the nation’s 300 largest metro area housing markets are seeing year-over-year home price declines, another 211 are seeing year-over-year home price increases. Where are home prices still up on a year-over-year basis? See the map below. Below is a historical chart showing the year-over-year change in home prices across the 50 largest metro housing markets, with the yellow line representing the national aggregate, dating back to 2000. While the “range” [see chart above] between the strongest and weakest metro area housing markets right now is fairly normal historically speaking, the “bifurcation” (i.e., direction) itself—the share of markets with rising home prices versus those with falling prices—is wider than normal, given that national appreciation has stabilized into a softer market with growth barely above +0.0%. And the longer some markets remain in the “rising” camp while others stay in the “falling” camp, the wider the gulf can become between the relatively more resilient markets and the weaker ones. For example, home prices in the Hartford, CT metro area are now +22.5% above their 2022 peak, while home prices in the Austin, TX metro area sit -27.8% below their 2022 peak. Some of that “bifurcation” boils down to mean reversion, with many of the outright home price declines occurring in markets that overheated further during the Pandemic Housing Boom. Note: For the historical chart above, we analyzed the 200 largest markets rather than the 300 used above, as some markets ranked 201 to 300 lack complete data going back to 2000. When weighted by population (not visualized), the housing market appears slightly weaker than the chart below suggests—which aligns with the fact that, among just the 50 largest housing markets, 24 (48%) are currently posting negative year-over-year price growth, and nationally aggregated home prices are up just +0.8% year-over-year using the Zillow Home Value Index. View the full article

-

Spring is in the air! The tulips are blooming, college acceptance letters are zooming into email inboxes, and the majority of parents with college-bound students are panicking about paying for their kid’s schooling. Ain’t this time of year grand? There’s a lot that families can do to tame the cost of higher education, starting with filing the Free Application for Federal Student Aid (FAFSA) which determines a student’s eligibility for federal aid, applying for scholarships and grants which don’t need to be repaid, and considering the cost of attendance when comparing college acceptance offers. But for some college students, there is a funding gap between their federal student aid–which includes federal student loans–and their total cost of attendance. If students or their parents can’t afford to pay the difference out of pocket, just over 9% turn to private student loans. And among undergraduate students, 92.45% of those private student loans are cosigned–often by Mom or Dad. Unfortunately, cosigning your kid’s private student loan can put your credit score, your retirement, and even your relationship with your child at risk. Here’s what you need to know about the unexamined dangers of cosigning your child’s private student loan. Student loan debt by the numbers There are 42.8 million federal student loan borrowers who owe a total loan balance of $1.693 trillion, which represents 90.9% of all student loan debt. Private student loans make up only 9.13% of all student loan debt, for a total loan balance of $133.4 billion. There’s an excellent reason why most student loan debt is federal: borrowers do not need to meet credit or income requirements to qualify for federal student loans. Additionally, interest rates on federal loans are set by Congress and are the same for every cohort of borrowers. The government also offers guaranteed benefits, such as income-driven repayment plans, potential loan forgiveness, and forbearance options. Unfortunately, 10.3% of student borrowers default on their loans within the first three years of repayment, and an average of 6.24% of student loan debt is in default at any given time. While the professional number crunchers haven’t teased out precisely how many of these defaulted loans are federal and how many are private, it’s safe to assume that there are a non-zero number of private, cosigned student loans going into default every year. Parent PLUS vs private student loan If you and your student have exhausted your federal student aid options, including scholarships, grants, federal student loans, and work-study programs, and you still have a funding gap, there are generally two loan options left. Parent PLUS loan A federal Parent PLUS loan allows the parent of a dependent undergraduate student to borrow up to the cost of attendance, minus any other federal student aid your student has received, on the student’s behalf. Like your student’s federal loans, PLUS loans offer multiple repayment options and allow for deferment and forbearance, although there is no path to loan forgiveness. You also cannot transfer your PLUS loan to the student you took it out for. You must not have an adverse credit history to qualify for a PLUS loan, even though this loan doesn’t require the same kind of credit check a traditional private loan uses to determine your interest rate. So it’s possible to be denied a PLUS loan, although there are workarounds–you may be able to explain the extenuating circumstances or get an “endorser,” i.e., a cosigner. Like your student’s federal loans, PLUS loans have interest rates and fees set by the federal government, and they aren’t cheap. Currently, PLUS loans have a fixed interest rate of 8.94% and an origination fee of 4.228% which is deducted from the amount disbursed. Additionally, while you can choose to defer PLUS loan payments until six months after your student leaves school, interest will accrue while they are in school, unless you make payments. Private student loans There are myriad private lenders with student loan products that can help dependent undergraduates bridge the funding gap. The problem is that the vast majority of undergraduate students don’t have the minimum credit score or income requirements to qualify for a private student loan on their own. Typically, private lenders require an established credit history, a credit score in the mid 600s, and a minimum income of $24,000–which is a tall order for an 18-year-old. But these requirements aren’t such difficult hurdles for the average parent of a college student. In fact, if you have a decent credit score and a good income, you may help your student qualify for a favorable interest rate. But private loans are more likely to require immediate repayment, rather than allowing for a deferment until your student is done with school. In addition, private loans have no path to forgiveness, few repayment plan options, and zero federal protections. What it means to cosign A recent survey of parents who cosigned private student loans for their students found that one-third of respondents did not fully understand the risks of cosigning. Specifically, if you cosign a loan with your kid, this is what you’re signing up for: You are legally responsible for the loan. If your child doesn’t make payments, creditors will come knocking on your door. If your child makes a late payment, it will affect your credit score. It doesn’t require a missed payment or a default for the cosigned loan to hurt your credit. According to the survey, 56.80% of cosigners believe that their credit scores were negatively impacted by cosigning the loan. The loan may affect your ability to get credit. If you want to apply for a mortgage or car loan, having the cosigned student loan on your credit report may make it difficult to qualify. That’s because the total amount owed will be included in your outstanding debt and the monthly payment is calculated as part of your debt-to-income ratio (how much of your income is earmarked for debt obligations), even if your child is entirely handling the payment on their own. You may be on the hook for up to 10 years. Depending on the loan, you may be stuck as a cosigner for the entire life of the loan–although some private lenders offer cosigner release after a set number of on-time payments. The loan may hurt your retirement. According to the survey, over half of cosigners feel that their child’s student debt is putting their retirement at risk. This may be related to the fact that nearly two-thirds of respondents have helped their kids with monthly payments. The loan may sour family relationships. Money has a way of magnifying old hurts and resentments. Cosigning a loan not only leaves you vulnerable to financial and psychological disappointment if your child falls behind on payments, but it can also open up the whole family to emotional distress if the student has siblings who you help in different ways. Cosigning can be a risky business The pressure you’re feeling to bridge the funding gap at Big Bucks University is real, especially if your kid has dreamed of attending BBU for years. But there’s a real cost to cosigning a private student loan to help your child pay for their education, and it’s important to slow down and consider the risks before you sign. To start, remember the massive size of the national student loan debt. Your child is about to become one of the 42.8 million federal student loan borrowers who owe a total loan balance of $1.693 trillion. Unfortunately, more than one out of every 10 borrowers defaults on their student loans within the first three years of repayment. Minimizing the amount your student borrows can help protect them from becoming part of this statistic. If you are facing a funding gap, you generally have two options: a federal Parent PLUS loan that you take out, or a private student loan you cosign with your student. The Parent PLUS loan has an 8.94% fixed interest rate and an origination fee of 4.228%, and borrowers must not have adverse credit history. The PLUS loan offers some federal protections, but fewer than the loans your student is taking out on their own behalf. Cosigning a student loan with your child may offer a lower rate, depending on your qualifications, but it puts you at risk of taking over the loan if your child defaults, hurting your credit if your child makes a late payment, affecting your credit, hurting your retirement, and potentially souring family relationships. If you and your kid go into cosigning a loan with your eyes wide open, your expectations explicitly spelled out, and an iron-clad agreement about how many times you’re each allowed to roll your eyes, it can be a viable method of filling a funding gap. But without clear expectations in place, a cosigned loan can become the beginning of the kind of tragic family story Aunt Gertrude tells when she’s feeling maudlin. View the full article

-

After going to war twice, the US president is again trying to strike a deal on the regime’s uranium enrichment programmeView the full article

-

Like many, I’ve never met a chatbot I trust completely. Not only do they have a propensity to hallucinate by making up facts, but you can never be sure what their parent companies do with the information you provide. Most AI companies say they use your data to further train their models, but anonymize it first. However, you just have to take them at their word on this. Still, chatbots can be useful for summarizing and explaining complicated information, such as the kind contained in many bank statements, medical reports, and mortgage contracts. So if you do choose to upload sensitive documents like this, you should take steps to redact as much personal information as possible, not only to protect your privacy from the AI company but also to hedge against future data breaches that could cause your financial and medical records to be spilled across the dark web. Here’s how. The wrong way to redact your sensitive data First things first: There’s a right and a wrong way to redact sensitive information, particularly from PDFs, which are the format most of our bank statements, medical records, and contracts come in. As some attorneys general and lawyers have learned the hard way, redacting PDFs the wrong way essentially provides no protection at all. The “wrong” way is to use a PDF reader’s markup tools, like the pen or highlighter, to scribble out or draw black bars across text. While these methods may hide text to the naked eye, a simple mouse move across the obscured line of text to select it, followed by a copy-and-paste, can often recover it. More advanced PDF tools can also easily remove any digital pen scratches and black highlights entirely, revealing the original text underneath. In short, the “wrong” way is akin to placing a piece of electrical tape over the lines of a document: it obscures the lines from view, but it can easily be peeled off. So, if you are using this redaction method before uploading your sensitive documents to ChatGPT, your instinct is in the right place, but your execution is off—and that leaves your sensitive personally identifiable information highly vulnerable. The right way to redact your sensitive information before uploading documents to AI chatbots The correct way to digitally redact documents is to use a tool specifically designed to destroy underlying data within the PDF’s internal code. These redaction tools literally get rid of the underlying text, making it nearly impossible to recover. The easiest redaction tool I’ve discovered is built into Apple’s Preview app. Preview is macOS’s default PDF reader (it’s also available on iPhone, but the iOS version lacks a redaction tool). If you’re a Windows user, note that that platform’s native PDF viewer, Microsoft Edge, doesn’t offer such a feature, though there are a number of third-party apps, like Adobe Acrobat Pro (subscription required) and PDFgear (free), that offer redaction tools. I’ll describe here how to use Apple’s Preview redaction tool, but most other apps’ redaction tools work in similar ways. How to redact your sensitive information before uploading documents to AI chatbots The important thing to note about redaction tools is that they are designed to destroy the text you want redacted, making it unreadable. So always be sure to first make a copy of the document you plan to upload to a chatbot, and redact information in the copy. Always keep the original undredacted document on your computer, so you can access its full contents. If you do not do this, you will lose the ability to read the original document in full, because you will not be able to unredact the text once it is redacted. Once you’ve made a copy of the document, you are ready to redact. Here’s how: Open the copy of the PDF document in the Preview app on your Mac. From the menu bar, select Tools>Redact. A warning will pop up alerting you that any “redacted content is permanently removed.” Click OK to dismiss the warning. Now, move the text selection cursor over any text you want redacted. This may include your name, address, email, phone number, Social Security number, or any other sensitive information. As you drag the text selection tool over your selection, black bars with grey X’s will be laid down across the text. This tells you the text is marked for redaction. Continue redacting any text you want across the entire document. Once you’ve marked all the text you’ve redacted, you can move your mouse over the black bars to see the text to be redacted beneath it, if you wish. You can also drag your text cursor back over the text to deselect it for redaction. If you are happy with your redaction selection, save the document. But note that even with the save, the selected text still has not been redacted. Now that the document has been saved, to complete the redaction, close the PDF(keyboard shortcut: Command-W). Once you do this, the text underneath the redaction markings will be destroyed. When you open the document again, you’ll see permanent black lines with grey X’s on them where the former text was. But the text beneath those lines has been destroyed and should now be unrecoverable. A few things to keep in mind While the above method should ensure that your selected text has been redacted correctly, so that it should not be recoverable by an AI chatbot or anyone who accesses the redacted document in the future, redacting personally identifiable information in a document doesn’t necessarily keep your identity anonymous from ChatGPT and other AI chatbots. This is because, even if you redact all your personally identifiable information in the document, if you are logged into ChatGPT, OpenAI will, of course, know that your account is the one that uploaded that March bank statement or that medical report. This means that if you want as much anonymity as possible, you should not only securely redact sensitive information in your documents before uploading them to AI chatbots, but also not upload them to any AI chatbot that you are logged into. As an added measure, it’s also a good idea to strip a PDF’s metadata before you upload it, as this metadata may include your name or other information. View the full article

-

Calculating corporate income tax can seem intimidating, but it doesn’t have to be. By following a structured approach, you can guarantee accuracy and compliance. Start by gathering all your financial statements, then work through the steps from calculating gross income to identifying tax credits. Each detail matters, as it can greatly affect your final tax liability. Ready to explore the crucial steps that lead to precise tax calculations? Let’s get into it. Key Takeaways Gather all financial statements, including the Income Statement, Balance Sheet, and Cash Flow Statement, to assess overall company performance. Calculate gross income by adding total revenues from all sources, ensuring accurate reporting for tax purposes. Deduct non-capital business expenses from gross income to determine preliminary taxable income, considering depreciation for capital expenses. Identify and apply relevant tax credits and deductions, including state-specific modifications, to minimize tax liability. Verify taxable income against financial statements and ensure timely estimated tax payments to avoid penalties. Understand the Basics of Corporate Income Tax Corporate income tax is a fundamental aspect of the financial environment for businesses, as it directly impacts the profits of C corporations. Comprehending how to calculate corporate income tax involves knowing that a fixed federal tax rate of 21% is applied to taxable income. To accurately report this, you’ll need to follow the form 1120 instructions, which guide you through reporting income, deductions, and credits. Most states adopt federal definitions of corporate income to determine taxable income, meaning you must apportion your income if operating in multiple states. Although some states impose their own rates, like Minnesota’s 9.8%, others like North Carolina have much lower rates at 2.5%. Be aware that certain states, such as Ohio and Washington, tax gross receipts instead of income, which adds another layer to reflect upon when calculating your tax obligations. Comprehending these basics is vital for compliance and financial planning. Gather Financial Statements and Data Before plunging into the nuances of calculating corporate income tax, it’s essential to gather all relevant financial statements and data that reflect your company’s financial performance. This foundational step sets the stage for an accurate tax calculation. Here’s what you need to collect: Income Statement: This shows your revenue and expenses, providing insight into your profitability. Balance Sheet: It outlines your company’s assets, liabilities, and equity, giving a snapshot of financial position. Cash Flow Statement: This document details cash inflows and outflows, vital for grasping liquidity. Expense Documentation: Differentiate between non-capital and capital expenses, and track any tax credits or deductions. Organizing these documents helps guarantee you capture all revenue sources and business expenses accurately, laying the groundwork for evaluating taxable income effectively and preparing for any challenges in tax compliance. Calculate Gross Income Calculating gross income is a fundamental step in determining your business’s overall tax liability, as it lays the groundwork for taxable income. For corporate tax purposes, gross income includes total revenues from various sources, such as sales, investments, franchise fees, and any compensation received for infringements. It’s important to account for all these income sources to guarantee a thorough assessment of your revenue. The IRS mandates that you accurately report gross income on your tax returns, as it serves as the foundation for calculating taxable income. Following federal tax regulations, you must include all forms of revenue in your gross income calculations. This accuracy is critical, as it directly impacts your corporate tax liability, which is assessed at a fixed corporate tax rate of 21%. Identify Allowable Business Expenses Identifying allowable business expenses is crucial for accurately determining your taxable income, as these costs can greatly reduce your overall tax liability. Comprehending which expenses qualify will help you maximize your deductions. Here are some key allowable business expenses to reflect on: Raw Materials: Costs directly associated with the production of goods or services your business offers. Salaries and Wages: Employee compensation, including bonuses and commissions, can be deducted. Rent: The cost of leasing office space or equipment is likewise deductible. Fringe Benefits: Expenses like health insurance premiums and retirement contributions for employees are allowable. Determine Taxable Income Determining taxable income is an essential step for any C corporation, as it directly influences the amount of corporate income tax you’ll owe. Start with your total revenues, which include sales, investments, and other income sources. Be certain you account for every type of revenue accurately. Next, subtract your non-capital business expenses, such as raw materials and selling costs, to arrive at a preliminary figure. Remember that capital business expenses aren’t deducted immediately; instead, focus on depreciation for assets with useful lives beyond one year, as required by tax regulations. After identifying these costs, calculate your taxable income by deducting total business expenses from your total revenues. Make certain you apply all necessary adjustments for permanent and temporary differences to arrive at the correct figure. Apply the Appropriate Corporate Tax Rate Once you’ve calculated your taxable income, applying the appropriate corporate tax rate is the next crucial step in comprehending your tax obligations. For C corporations, this rate is fixed at 21%, which applies to your taxable income after deductions and credits. Nevertheless, state-specific tax rates can vary greatly, so you must account for these as well. Here are some key considerations: Determine Federal Rate: Start with the 21% federal rate for C corporations. Identify State Rates: Research the corporate tax rate in each state where you operate, as these can differ widely. Apportion Income: Allocate your taxable income to each state according to its rules. Calculate Total Liability: Multiply your apportioned taxable income by the corresponding state tax rates, then add the federal tax to determine your total tax liability. Account for Tax Credits and Deductions When calculating corporate income tax, it’s essential to identify available tax credits and analyze applicable deductions. Tax credits can greatly reduce your tax liability, whereas deductions lower your taxable income, both of which can lead to substantial savings. Keeping accurate records and comprehending the specific credits and deductions relevant to your business will guarantee you maximize your benefits and comply with tax regulations. Identify Available Tax Credits Identifying available tax credits is vital for corporations seeking to minimize their tax liability. Tax credits can considerably reduce the amount owed, so it’s important to know what’s out there. Here are some key credits to reflect on: Research and Development (R&D) Tax Credit: For businesses engaged in qualifying activities, this can lead to substantial savings. Renewable Energy Investments: You might earn credits up to 30% of your investment cost in sustainable projects. State-Specific Credits: Many states offer unique tax credits that can positively impact your overall tax situation. Consulting with Tax Professionals: They can help identify and maximize all applicable credits, ensuring you don’t miss out on potential savings. Stay informed and proactive to optimize your corporate tax strategy. Analyze Applicable Deductions To effectively reduce your corporate tax liability, analyzing applicable deductions is crucial, as these deductions can markedly lower your taxable income. Start by identifying allowable deductions like business expenses, salaries, and benefits, which directly cut your overall tax liability. Don’t forget about tax credits, such as those for research and development or renewable energy investments, which offer dollar-for-dollar reductions in taxes owed. It’s important to distinguish between permanent and temporary differences, as permanent differences won’t reverse and can impact your financial statements differently. Keep accurate records and documentation of all expenses and credits, since the IRS requires proof to validate your claims during audits. Consider using tax software or professional services to maximize your savings and guarantee compliance with current tax laws. Consider State-Specific Regulations and Apportionment When you’re calculating corporate income tax, comprehension of state-specific apportionment methods is essential. Different states use various approaches, like three-factor or single sales factor, which can impact how you allocate income. Furthermore, be aware of state modifications, such as disallowing federal bonus depreciation, since they can greatly alter your taxable income calculations. Understand Apportionment Methods Grasping apportionment methods is fundamental for corporations operating across state lines, as these methods determine how much of their income is taxable in each state. You’ll need to take into account various factors and state-specific regulations when determining your apportionment approach. Here are some common methods: Three-Factor: This method considers property, payroll, and sales, allowing a balanced assessment across factors. Single Sales Factor: Focusing solely on in-state sales, this method simplifies calculations, benefiting companies with significant out-of-state assets. Hybrid Approach: Combining different factors customized to specific business needs or state requirements. State-Specific Rules: Each state has unique regulations, so staying updated is vital for accurate tax calculations and compliance. Adjust for State Modifications Adjusting for state modifications is crucial as each state has its own set of regulations that can significantly impact your taxable income. You’ll need to carefully adjust your federal taxable income based on these state-specific modifications, which may include the disallowance of federal bonus depreciation. Different states also employ varying apportionment methods, such as three-factor or single sales factor, to determine the share of income subject to state tax. To compute state apportionment accurately, gather data on revenue, payroll, and property, ensuring consistency across states to avoid discrepancies. Utilizing technology like Bloomberg Tax Workpapers can streamline this process by automating calculations and ensuring compliance with state regulations, making your adjustments more efficient and precise. Review and Finalize Tax Calculations To guarantee the accuracy of your corporate income tax calculations, it’s essential to carefully review the calculated taxable income, aligning it with your financial statements. This verifies that all revenues and expenses match and that deductions have been properly applied. Here are some key steps to follow: Double-check state-specific tax modifications, confirming compliance with local laws and limitations on federal deductions. Utilize error-checking functions in tax software, like Bloomberg Tax Workpapers, to identify any discrepancies and minimize human error. Consolidate data across multiple entities and states, verifying that apportionment formulas reflect current regulations. Finalize your calculations by consulting tax provision checklists, verifying all credits and deductions are accounted for, which can greatly reduce your tax liability. Ensure Timely Tax Payments and Compliance To guarantee compliance with tax regulations, you need to make your estimated tax payments on time, as required by the IRS. Missing deadlines can lead to penalties and interest, putting your corporation’s financial standing at risk. Importance of Timely Payments Even though it may seem manageable to delay tax payments, timely payments are vital for ensuring compliance with IRS regulations. When you meet your payment deadlines, you help maintain good standing with tax authorities, which is fundamental for smooth business operations. Here are some key reasons to prioritize timely payments: Regulatory Compliance: Corporations must make estimated payments if they expect to owe $500 or more. Avoiding Surprises: Accurate calculations of your tax liability assist in proper budgeting and prevent unexpected costs. Positive Compliance History: Consistent and timely payments contribute to a strong relationship with tax authorities. Reduced Financial Burden: Timely payments minimize the risk of penalties and interest, keeping your overall tax burden manageable. Avoiding Penalties and Interest Failing to make timely tax payments can lead to unnecessary penalties and interest that accumulate quickly, impacting your corporation’s bottom line. If you expect to owe $500 or more in taxes, you must make estimated tax payments due on the 15th of the 4th, 6th, 9th, and 12th months. To avoid penalties, calculate your estimated tax liability accurately using Form 1120-W, which helps determine your installment amounts. You can choose between the Current Year Method and the Previous Year Method, both requiring precise financial records. Furthermore, consider using the IRS electronic federal tax payment system (EFTPS) for quick and documented transactions, ensuring you meet deadlines and minimize the risk of underpayment penalties. Maintaining Tax Compliance Standards Maintaining tax compliance standards is vital for C corporations, as it safeguards against potential legal issues and financial penalties. To guarantee timely tax payments and compliance, follow these important steps: Make four installment payments throughout the year, due on the 15th of the 4th, 6th, 9th, and 12th months to avoid penalties. If you expect to owe $500 or more, prepare to make estimated tax payments as per IRS guidelines. Use the Current Year Method to determine each installment as 25% of expected income tax based on net profit before taxes. On the other hand, apply the Previous Year Method to base estimated payments on 25% of last year’s tax return, provided you’d a positive tax liability. Accurate calculations and timely payments are important for compliance. Frequently Asked Questions How Do You Calculate Corporate Income Tax? To calculate corporate income tax, you start with your total revenues, which include sales and other income streams. Next, subtract allowable business expenses to find your taxable income. Apply the federal corporate tax rate of 21% to this amount. Don’t forget to take into account state-specific tax rates, which can vary, and any adjustments for non-deductible expenses or available tax credits, as these can affect your overall tax liability considerably. How to Calculate C Corp Taxes for Dummies? To calculate C Corp taxes, you start with total revenues from sales and investments. Next, subtract allowable business expenses to find your taxable income. Apply the corporate tax rate of 21% to this income to determine your tax liability. Don’t forget to take into account any tax credits or deductions that might lower your total. Finally, keep in mind the double taxation on dividends paid to shareholders, affecting your overall tax responsibility. How to Calculate Corporation Tax? To calculate corporation tax, start by determining your total revenues, which include sales and other income sources. Next, deduct your non-capital business expenses, like costs of materials and administrative fees, to find your taxable income. Once you have that figure, apply the corporate tax rate, typically 21%. Finally, consider any applicable tax credits or deductions that could lower your overall tax liability before ensuring compliance with any state-specific regulations. How Do You Ensure Accuracy in Tax Calculations and Analysis? To guarantee accuracy in tax calculations and analysis, you should utilize automation tools that streamline data processing and reduce manual errors. Start by gathering accurate federal taxable income, making necessary adjustments for state-specific regulations. Implement a consistent review process to consolidate data across departments, confirming compliance. Using tax provision software can help capture real-time updates, as thorough documentation of all calculations supports compliance and facilitates audits or inquiries effectively. Conclusion In summary, accurately calculating corporate income tax involves several critical steps, from gathering financial statements to guaranteeing timely payments. By comprehending gross income, allowable expenses, and applicable tax credits, you can determine your taxable income with precision. Furthermore, staying compliant with state regulations is vital to avoid penalties. Following these steps not merely simplifies the tax process but likewise helps your business manage its financial obligations effectively. Staying informed will make certain you meet all requirements efficiently. Image via Google Gemini This article, "10 Steps to Calculate Corporate Income Tax Accurately" was first published on Small Business Trends View the full article

-

Calculating corporate income tax can seem intimidating, but it doesn’t have to be. By following a structured approach, you can guarantee accuracy and compliance. Start by gathering all your financial statements, then work through the steps from calculating gross income to identifying tax credits. Each detail matters, as it can greatly affect your final tax liability. Ready to explore the crucial steps that lead to precise tax calculations? Let’s get into it. Key Takeaways Gather all financial statements, including the Income Statement, Balance Sheet, and Cash Flow Statement, to assess overall company performance. Calculate gross income by adding total revenues from all sources, ensuring accurate reporting for tax purposes. Deduct non-capital business expenses from gross income to determine preliminary taxable income, considering depreciation for capital expenses. Identify and apply relevant tax credits and deductions, including state-specific modifications, to minimize tax liability. Verify taxable income against financial statements and ensure timely estimated tax payments to avoid penalties. Understand the Basics of Corporate Income Tax Corporate income tax is a fundamental aspect of the financial environment for businesses, as it directly impacts the profits of C corporations. Comprehending how to calculate corporate income tax involves knowing that a fixed federal tax rate of 21% is applied to taxable income. To accurately report this, you’ll need to follow the form 1120 instructions, which guide you through reporting income, deductions, and credits. Most states adopt federal definitions of corporate income to determine taxable income, meaning you must apportion your income if operating in multiple states. Although some states impose their own rates, like Minnesota’s 9.8%, others like North Carolina have much lower rates at 2.5%. Be aware that certain states, such as Ohio and Washington, tax gross receipts instead of income, which adds another layer to reflect upon when calculating your tax obligations. Comprehending these basics is vital for compliance and financial planning. Gather Financial Statements and Data Before plunging into the nuances of calculating corporate income tax, it’s essential to gather all relevant financial statements and data that reflect your company’s financial performance. This foundational step sets the stage for an accurate tax calculation. Here’s what you need to collect: Income Statement: This shows your revenue and expenses, providing insight into your profitability. Balance Sheet: It outlines your company’s assets, liabilities, and equity, giving a snapshot of financial position. Cash Flow Statement: This document details cash inflows and outflows, vital for grasping liquidity. Expense Documentation: Differentiate between non-capital and capital expenses, and track any tax credits or deductions. Organizing these documents helps guarantee you capture all revenue sources and business expenses accurately, laying the groundwork for evaluating taxable income effectively and preparing for any challenges in tax compliance. Calculate Gross Income Calculating gross income is a fundamental step in determining your business’s overall tax liability, as it lays the groundwork for taxable income. For corporate tax purposes, gross income includes total revenues from various sources, such as sales, investments, franchise fees, and any compensation received for infringements. It’s important to account for all these income sources to guarantee a thorough assessment of your revenue. The IRS mandates that you accurately report gross income on your tax returns, as it serves as the foundation for calculating taxable income. Following federal tax regulations, you must include all forms of revenue in your gross income calculations. This accuracy is critical, as it directly impacts your corporate tax liability, which is assessed at a fixed corporate tax rate of 21%. Identify Allowable Business Expenses Identifying allowable business expenses is crucial for accurately determining your taxable income, as these costs can greatly reduce your overall tax liability. Comprehending which expenses qualify will help you maximize your deductions. Here are some key allowable business expenses to reflect on: Raw Materials: Costs directly associated with the production of goods or services your business offers. Salaries and Wages: Employee compensation, including bonuses and commissions, can be deducted. Rent: The cost of leasing office space or equipment is likewise deductible. Fringe Benefits: Expenses like health insurance premiums and retirement contributions for employees are allowable. Determine Taxable Income Determining taxable income is an essential step for any C corporation, as it directly influences the amount of corporate income tax you’ll owe. Start with your total revenues, which include sales, investments, and other income sources. Be certain you account for every type of revenue accurately. Next, subtract your non-capital business expenses, such as raw materials and selling costs, to arrive at a preliminary figure. Remember that capital business expenses aren’t deducted immediately; instead, focus on depreciation for assets with useful lives beyond one year, as required by tax regulations. After identifying these costs, calculate your taxable income by deducting total business expenses from your total revenues. Make certain you apply all necessary adjustments for permanent and temporary differences to arrive at the correct figure. Apply the Appropriate Corporate Tax Rate Once you’ve calculated your taxable income, applying the appropriate corporate tax rate is the next crucial step in comprehending your tax obligations. For C corporations, this rate is fixed at 21%, which applies to your taxable income after deductions and credits. Nevertheless, state-specific tax rates can vary greatly, so you must account for these as well. Here are some key considerations: Determine Federal Rate: Start with the 21% federal rate for C corporations. Identify State Rates: Research the corporate tax rate in each state where you operate, as these can differ widely. Apportion Income: Allocate your taxable income to each state according to its rules. Calculate Total Liability: Multiply your apportioned taxable income by the corresponding state tax rates, then add the federal tax to determine your total tax liability. Account for Tax Credits and Deductions When calculating corporate income tax, it’s essential to identify available tax credits and analyze applicable deductions. Tax credits can greatly reduce your tax liability, whereas deductions lower your taxable income, both of which can lead to substantial savings. Keeping accurate records and comprehending the specific credits and deductions relevant to your business will guarantee you maximize your benefits and comply with tax regulations. Identify Available Tax Credits Identifying available tax credits is vital for corporations seeking to minimize their tax liability. Tax credits can considerably reduce the amount owed, so it’s important to know what’s out there. Here are some key credits to reflect on: Research and Development (R&D) Tax Credit: For businesses engaged in qualifying activities, this can lead to substantial savings. Renewable Energy Investments: You might earn credits up to 30% of your investment cost in sustainable projects. State-Specific Credits: Many states offer unique tax credits that can positively impact your overall tax situation. Consulting with Tax Professionals: They can help identify and maximize all applicable credits, ensuring you don’t miss out on potential savings. Stay informed and proactive to optimize your corporate tax strategy. Analyze Applicable Deductions To effectively reduce your corporate tax liability, analyzing applicable deductions is crucial, as these deductions can markedly lower your taxable income. Start by identifying allowable deductions like business expenses, salaries, and benefits, which directly cut your overall tax liability. Don’t forget about tax credits, such as those for research and development or renewable energy investments, which offer dollar-for-dollar reductions in taxes owed. It’s important to distinguish between permanent and temporary differences, as permanent differences won’t reverse and can impact your financial statements differently. Keep accurate records and documentation of all expenses and credits, since the IRS requires proof to validate your claims during audits. Consider using tax software or professional services to maximize your savings and guarantee compliance with current tax laws. Consider State-Specific Regulations and Apportionment When you’re calculating corporate income tax, comprehension of state-specific apportionment methods is essential. Different states use various approaches, like three-factor or single sales factor, which can impact how you allocate income. Furthermore, be aware of state modifications, such as disallowing federal bonus depreciation, since they can greatly alter your taxable income calculations. Understand Apportionment Methods Grasping apportionment methods is fundamental for corporations operating across state lines, as these methods determine how much of their income is taxable in each state. You’ll need to take into account various factors and state-specific regulations when determining your apportionment approach. Here are some common methods: Three-Factor: This method considers property, payroll, and sales, allowing a balanced assessment across factors. Single Sales Factor: Focusing solely on in-state sales, this method simplifies calculations, benefiting companies with significant out-of-state assets. Hybrid Approach: Combining different factors customized to specific business needs or state requirements. State-Specific Rules: Each state has unique regulations, so staying updated is vital for accurate tax calculations and compliance. Adjust for State Modifications Adjusting for state modifications is crucial as each state has its own set of regulations that can significantly impact your taxable income. You’ll need to carefully adjust your federal taxable income based on these state-specific modifications, which may include the disallowance of federal bonus depreciation. Different states also employ varying apportionment methods, such as three-factor or single sales factor, to determine the share of income subject to state tax. To compute state apportionment accurately, gather data on revenue, payroll, and property, ensuring consistency across states to avoid discrepancies. Utilizing technology like Bloomberg Tax Workpapers can streamline this process by automating calculations and ensuring compliance with state regulations, making your adjustments more efficient and precise. Review and Finalize Tax Calculations To guarantee the accuracy of your corporate income tax calculations, it’s essential to carefully review the calculated taxable income, aligning it with your financial statements. This verifies that all revenues and expenses match and that deductions have been properly applied. Here are some key steps to follow: Double-check state-specific tax modifications, confirming compliance with local laws and limitations on federal deductions. Utilize error-checking functions in tax software, like Bloomberg Tax Workpapers, to identify any discrepancies and minimize human error. Consolidate data across multiple entities and states, verifying that apportionment formulas reflect current regulations. Finalize your calculations by consulting tax provision checklists, verifying all credits and deductions are accounted for, which can greatly reduce your tax liability. Ensure Timely Tax Payments and Compliance To guarantee compliance with tax regulations, you need to make your estimated tax payments on time, as required by the IRS. Missing deadlines can lead to penalties and interest, putting your corporation’s financial standing at risk. Importance of Timely Payments Even though it may seem manageable to delay tax payments, timely payments are vital for ensuring compliance with IRS regulations. When you meet your payment deadlines, you help maintain good standing with tax authorities, which is fundamental for smooth business operations. Here are some key reasons to prioritize timely payments: Regulatory Compliance: Corporations must make estimated payments if they expect to owe $500 or more. Avoiding Surprises: Accurate calculations of your tax liability assist in proper budgeting and prevent unexpected costs. Positive Compliance History: Consistent and timely payments contribute to a strong relationship with tax authorities. Reduced Financial Burden: Timely payments minimize the risk of penalties and interest, keeping your overall tax burden manageable. Avoiding Penalties and Interest Failing to make timely tax payments can lead to unnecessary penalties and interest that accumulate quickly, impacting your corporation’s bottom line. If you expect to owe $500 or more in taxes, you must make estimated tax payments due on the 15th of the 4th, 6th, 9th, and 12th months. To avoid penalties, calculate your estimated tax liability accurately using Form 1120-W, which helps determine your installment amounts. You can choose between the Current Year Method and the Previous Year Method, both requiring precise financial records. Furthermore, consider using the IRS electronic federal tax payment system (EFTPS) for quick and documented transactions, ensuring you meet deadlines and minimize the risk of underpayment penalties. Maintaining Tax Compliance Standards Maintaining tax compliance standards is vital for C corporations, as it safeguards against potential legal issues and financial penalties. To guarantee timely tax payments and compliance, follow these important steps: Make four installment payments throughout the year, due on the 15th of the 4th, 6th, 9th, and 12th months to avoid penalties. If you expect to owe $500 or more, prepare to make estimated tax payments as per IRS guidelines. Use the Current Year Method to determine each installment as 25% of expected income tax based on net profit before taxes. On the other hand, apply the Previous Year Method to base estimated payments on 25% of last year’s tax return, provided you’d a positive tax liability. Accurate calculations and timely payments are important for compliance. Frequently Asked Questions How Do You Calculate Corporate Income Tax? To calculate corporate income tax, you start with your total revenues, which include sales and other income streams. Next, subtract allowable business expenses to find your taxable income. Apply the federal corporate tax rate of 21% to this amount. Don’t forget to take into account state-specific tax rates, which can vary, and any adjustments for non-deductible expenses or available tax credits, as these can affect your overall tax liability considerably. How to Calculate C Corp Taxes for Dummies? To calculate C Corp taxes, you start with total revenues from sales and investments. Next, subtract allowable business expenses to find your taxable income. Apply the corporate tax rate of 21% to this income to determine your tax liability. Don’t forget to take into account any tax credits or deductions that might lower your total. Finally, keep in mind the double taxation on dividends paid to shareholders, affecting your overall tax responsibility. How to Calculate Corporation Tax? To calculate corporation tax, start by determining your total revenues, which include sales and other income sources. Next, deduct your non-capital business expenses, like costs of materials and administrative fees, to find your taxable income. Once you have that figure, apply the corporate tax rate, typically 21%. Finally, consider any applicable tax credits or deductions that could lower your overall tax liability before ensuring compliance with any state-specific regulations. How Do You Ensure Accuracy in Tax Calculations and Analysis? To guarantee accuracy in tax calculations and analysis, you should utilize automation tools that streamline data processing and reduce manual errors. Start by gathering accurate federal taxable income, making necessary adjustments for state-specific regulations. Implement a consistent review process to consolidate data across departments, confirming compliance. Using tax provision software can help capture real-time updates, as thorough documentation of all calculations supports compliance and facilitates audits or inquiries effectively. Conclusion In summary, accurately calculating corporate income tax involves several critical steps, from gathering financial statements to guaranteeing timely payments. By comprehending gross income, allowable expenses, and applicable tax credits, you can determine your taxable income with precision. Furthermore, staying compliant with state regulations is vital to avoid penalties. Following these steps not merely simplifies the tax process but likewise helps your business manage its financial obligations effectively. Staying informed will make certain you meet all requirements efficiently. Image via Google Gemini This article, "10 Steps to Calculate Corporate Income Tax Accurately" was first published on Small Business Trends View the full article

-

Rise in domestic tourism could provide relief for rural hospitality businesses struggling with higher costsView the full article

-

The aspiration gap has turned everyone into losers, especially graduatesView the full article

-

Reflections on an ancient prejudiceView the full article

-

Company expands accommodation options alongside home rentals but analysts warn of stiff competitionView the full article

-

Hunger and even famine are foreseeable consequences of the war on Iran. Now the world must act to shield the poorest from effects that will continue long after the fighting stopsView the full article

-

Officials plan to reopen frontier with Armenia to unlock a The President-backed trade route between Europe and Asia View the full article

-

In relation to small business tax rates, comprehending the differences based on your business structure is essential. C corporations face a flat federal rate of 21%, whereas pass-through entities, like sole proprietorships and partnerships, are taxed according to individual income tax brackets that can range from 10% to 37%. State tax rates likewise differ greatly, further complicating your tax obligations. Knowing these details can help you navigate your tax responsibilities effectively. What strategies can you employ to minimize your burden? Key Takeaways C corporations face a flat federal tax rate of 21% on taxable income. Pass-through entities are taxed based on individual income tax brackets, ranging from 10% to 37%. State corporate tax rates vary; California is 8.84%, Georgia is 5.75%, and Florida is 5.5%. Pass-through entities may be subject to state income tax rates from 0% to 13.30%. Corporations face double taxation, while sole proprietorships and partnerships report income on personal tax returns. Understanding Small Business Tax Rates When you’re maneuvering through the domain of small business taxes, it’s crucial to comprehend that the rates you face depend largely on your business structure. For C corporations, the federal tax rate is a flat 21%, whereas pass-through entities like sole proprietorships and LLCs get taxed based on individual income tax brackets, ranging from 10% to 37%. At the state level, the California corporate tax rate is 8.84%, and Georgia‘s corporate tax rate is 5.75%. These state rates can greatly impact your overall tax burden. Furthermore, pass-through entities are typically taxed at personal income tax rates, which can range from 0% to 13.30%. Federal Income Taxes for Small Businesses Comprehending federal income taxes for small businesses is essential, as your tax obligations will vary based on your business structure. If you operate a C corporation, you’ll face a flat federal income tax rate of 21%. Conversely, pass-through entities such as sole proprietorships and LLCs are taxed based on individual income tax brackets, which range from 10% to 37% in 2025. Most small businesses must make estimated tax payments, whereas partnerships only need to file an information return. Furthermore, self-employed individuals must pay self-employment tax if their net earnings exceed $400. This tax covers Social Security and Medicare contributions. To potentially lower your taxable income, you can likewise take advantage of the Qualified Business Income deduction, which allows eligible owners of pass-through entities to deduct up to 20% of their business income, offering significant savings on federal income tax liabilities. State Income Taxes for Small Businesses When you consider state income taxes for small businesses, you’ll find that rates can vary widely, impacting your bottom line. For instance, whereas California’s tax rate may reach as high as 13.30%, states like Florida offer a more favorable 5.5% corporate tax rate. Furthermore, if you operate as a pass-through entity, your income will be taxed at your individual rate, which can fluctuate between 10% and 37%, depending on your earnings and the state you’re in. Corporate Tax Rates Grasping corporate tax rates is essential for small business owners, as these rates can greatly impact their bottom line. C corporations face a federal tax rate of 21%, but state corporate taxes vary considerably. For instance, California imposes an 8.84% corporate tax on businesses, which can add to your expenses. Conversely, Georgia offers a lower corporate tax rate, which can influence your decision if you’re considering expansion there. The state income tax rate in Georgia is relatively competitive, making it an appealing option for new ventures. Furthermore, some states provide special business tax rates or incentives, which can further affect your overall tax burden. Comprehending these rates helps you make informed financial decisions for your business. Pass-Through Entity Taxation Comprehending pass-through entity taxation is vital for small business owners, as it directly impacts how your business profits are taxed at the state level. Pass-through entities like sole proprietorships and partnerships don’t pay federal taxes at the entity level; instead, income is taxed at your individual rate, which can range from 10% to 37% in 2025. In Georgia, the state income tax rate for pass-through entities aligns with personal income tax rates, typically around 5.75%. So, if you’re wondering how much are taxes in Georgia for your business, consider this rate. Furthermore, you could benefit from the Qualified Business Income deduction, allowing for a potential 20% reduction in taxable income. Accurate record-keeping is vital for maximizing deductions and minimizing overall tax liability. Types of Business Structures and Their Tax Implications When choosing a business structure, comprehension of the tax implications is essential for your financial planning. Sole proprietorships and partnerships are taxed as pass-through entities, meaning profits or losses appear on your personal tax return. Conversely, corporations face different tax rates and structures, including potential double taxation, which can greatly impact your overall tax burden. Sole Proprietorship Taxation Overview A sole proprietorship serves as the simplest and most common business structure, particularly for individuals looking to start their own ventures. If you’re the sole owner, your business automatically falls into this category, and you’ll file taxes using your personal Social Security Number (SSN). You’ll be taxed at individual income tax rates, which for 2025 range from 10% to 37%, based on your total taxable income. Your business income is reported on Schedule C of your personal tax return, allowing you to deduct business expenses to lower your taxable income. Furthermore, if you earn more than $400, you’ll need to pay a self-employment tax of 15.3% on your net earnings, covering Social Security and Medicare. Partnership Tax Structure Partnerships represent another common business structure that offers distinct tax implications compared to sole proprietorships. Classified as pass-through entities, partnerships don’t pay income tax at the business level; instead, profits and losses flow through to your personal tax return, taxed at your individual rate, ranging from 10% to 37% for 2025. There are two main types: Limited Partnerships (LP), which feature both general and limited partners, and Limited Liability Partnerships (LLP), providing personal liability protection to all partners. Partnerships must file an annual information return (Form 1065) with the IRS, but each partner receives a Schedule K-1 detailing their share of income, deductions, and credits. Furthermore, partnerships can access various deductions, including the Qualified Business Income (QBI) deduction. Corporation Tax Implications Comprehending the tax implications of different corporation types is essential for business owners. C corporations face a flat federal tax rate of 21% on taxable income, but they’re subject to double taxation when profits are distributed as dividends. Conversely, S corporations allow profits and losses to pass through to shareholders’ personal tax returns, avoiding double taxation, though they limit shareholders to a maximum of 100. Limited Liability Companies (LLCs) provide flexibility, allowing you to choose taxation as a sole proprietorship, partnership, or corporation, all the while protecting members from personal liability. Sole proprietorships report business income on their owner’s personal tax return, facing individual tax rates between 10% and 37%. Partnerships pass income or losses to partners, who report them on their personal returns. Sales and Use Taxes Sales and use taxes are vital components of the tax obligations faced by small businesses in the United States. Sales tax is a percentage added to the sale price of taxable goods and services, which you must collect from your customers. This rate varies by state, with California at 7.25% and Texas at 6.25%. Furthermore, use taxes are applicable on out-of-state purchases made for business purposes, ensuring you pay the appropriate taxes on items not taxed in your state. Local jurisdictions may likewise impose extra sales taxes, pushing total rates over 8% in some areas. It’s important to accurately track and remit collected sales taxes to state and local authorities to stay compliant with tax regulations. Failing to do so can lead to penalties and interest charges, underscoring the significance of comprehending your obligations in your specific jurisdiction. Payroll Taxes Overview After grasping your sales and use tax obligations, it’s important to turn your attention to payroll taxes, which play a significant role in the financial responsibilities of small businesses. As an employer, you’re responsible for several payroll taxes, including federal income tax withholding, Social Security, and Medicare taxes, collectively known as FICA, along with federal unemployment tax (FUTA). FICA taxes total 15.3% of eligible gross earnings, with you and your employees each contributing 7.65%. Importantly, Social Security tax only applies to the first $168,600 of earnings in 2024, whereas Medicare has no income cap. Furthermore, you must adhere to state and local payroll tax regulations, which can differ widely between jurisdictions. To avoid penalties and interest on overdue amounts, accurate payroll tax calculations and timely payments are vital. Grasping these obligations will help you maintain compliance and manage your business finances effectively. Calculating Your Small Business Taxes Calculating your small business taxes starts with determining your taxable income, which involves deducting eligible business expenses from your total revenue. It’s essential to keep accurate records, as these deductions can markedly reduce your tax liability. Comprehending the different structures of your business and the potential for deductions, like the Qualified Business Income deduction, can further impact the taxes you owe. Taxable Income Calculation Determining your small business’s taxable income is a crucial step in comprehending your tax obligations. To calculate this, start with your total revenue and subtract business expenses, tax deductions, exemptions, and credits. For C-corporations, a flat federal income tax rate of 21% applies to taxable income. Conversely, pass-through entities like sole proprietorships and LLCs are taxed based on individual income tax brackets, ranging from 10% to 37% in 2025. At the state level, C corporations face corporate tax rates between 0% and 9.80%, whereas pass-through entities typically pay state taxes according to personal income tax rates, which can reach up to 13.30%. Utilizing deductions, such as the Qualified Business Income deduction, can also greatly reduce taxable income. Deductible Business Expenses In relation to managing your small business taxes, comprehending deductible business expenses is vital for reducing your taxable income. You can offset your revenue by identifying eligible costs like operating expenses, supplies, and travel-related expenses. Common deductible items include vehicle mileage, home office costs, and health insurance premiums if you’re self-employed. Furthermore, the Qualified Business Income (QBI) deduction allows you to deduct up to 20% of your qualified business income, further lowering your taxable income. Accurate record-keeping of all expenses is imperative, as it substantiates your deductions during tax filings or audits. Finally, don’t forget to explore tax credits, which can directly reduce your tax payments and may offer greater benefits than deductions. Tax Deductions and Credits for Small Businesses Comprehending tax deductions and credits is vital for small business owners who want to minimize their tax liabilities and maximize their profitability. By utilizing these financial tools effectively, you can lower your taxable income and improve your bottom line. Here are three key deductions and credits to take into account: Qualified Business Income (QBI) Deduction: This allows eligible owners to claim up to a 20% deduction on their qualified business income, greatly reducing your tax burden. Expense Deductions: You can deduct various expenses, like home office costs, vehicle mileage, and interest on business-related debts, to lower your taxable income. Tax Credits: These directly reduce the amount of tax owed and can include credits for research and development, hiring from target groups, and energy efficiency improvements. Understanding these deductions and credits can provide substantial savings, making it important to stay informed about your options. Strategies for Minimizing Your Tax Burden During the process of maneuvering through the intricacies of taxation, small business owners can adopt several strategies to effectively minimize their tax burden. Start by keeping accurate records of all business expenses, as these deductions can greatly reduce your taxable income. Take advantage of the Qualified Business Income (QBI) deduction, allowing you to deduct up to 20% of your qualified business income, which can lower your effective tax rate. Moreover, consider the legal structure of your business; forming an LLC or S Corporation may offer tax advantages and help avoid double taxation. Engaging a tax professional can also be advantageous, as they can identify specific tax credits and deductions customized to your situation. Finally, regularly review state and local tax rates, since variations can impact your overall tax burden, especially in regions with higher sales or property taxes. Reporting Requirements for Small Businesses Comprehension of the reporting requirements for small businesses is crucial for maintaining compliance and avoiding potential penalties. Here are key aspects you should know: Most small businesses, except partnerships, must file an annual income tax return. Partnerships file an information return but don’t pay taxes at the entity level. As a pay-as-you-go tax, federal income tax requires you to withhold income taxes from employee paychecks and make quarterly estimated tax payments if your withholding isn’t sufficient. If you’re self-employed with net earnings exceeding $400, you’ll need to make estimated tax payments to avoid underpayment penalties. The Importance of Record-Keeping Effective record-keeping is crucial for small businesses, as it directly impacts your ability to determine taxable income and maximize deductions. Accurate records help you track revenue, expenses, deductions, and credits effectively, guaranteeing you’re aware of potential tax benefits like home office expenses and vehicle mileage. By identifying these deductions, you can considerably reduce your taxable income. The IRS requires you to maintain records for at least three years from the date you file a return, which helps guarantee compliance and provides necessary substantiation in case of an audit. Utilizing automated accounting and mileage tracking tools can simplify your record-keeping process, reducing errors and saving time compared to manual logging. Regularly reviewing your financial records allows you to make informed decisions, maximize tax benefits, and engage proactively with tax professionals for strategic planning. This disciplined approach to record-keeping eventually protects your business’s financial health and supports its growth. Resources for Small Business Tax Assistance Steering through the intricacies of tax obligations can be intimidating for small business owners, but a wealth of resources is available to help you manage these responsibilities effectively. Here are three key resources to evaluate: IRS Small Business/Self-Employed Tax Center: This site provides crucial guidance on tax obligations, forms, and deductions particularly designed for small businesses. Small Business Administration (SBA): The SBA offers workshops, webinars, and resources to help you understand your tax responsibilities and locate tax assistance programs in your area. Local Small Business Development Centers (SBDCs): These centers provide free consulting services, helping you grasp tax implications and ensuring your filings are accurate. Additionally, tax professionals like CPAs and online software tools such as TurboTax can offer personalized advice and simplify the filing process, making it easier for you to stay compliant and minimize your tax burden. Frequently Asked Questions How Much Is the Tax for a Small Business? The tax for a small business varies considerably based on its structure. If you operate as a C corporation, expect a flat federal tax rate of 21%. For pass-through entities like sole proprietorships or LLCs, taxes align with individual income brackets, ranging from 10% to 37%. Moreover, state tax rates differ, with some states imposing corporate taxes up to 9.80%, whereas others may have no tax at all. Don’t forget about self-employment taxes if applicable. How Much Does Your Small Business Have to Make to Pay Taxes? Your small business needs to make at least $400 in net earnings from self-employment to start paying taxes. This applies to sole proprietorships and partnerships. If you operate as a C corporation, you’re taxed at a flat 21% rate regardless of income. For pass-through entities like LLCs or S corporations, taxes depend on your individual income tax bracket, which ranges from 10% to 37% in 2025. Keep this in mind for tax planning. Is Self-Employment Tax 15% or 30%? Self-employment tax isn’t 15% or 30%; it’s actually 15.3%. This rate includes 12.4% for Social Security and 2.9% for Medicare. Nonetheless, only the first $168,600 of earnings in 2024 is subject to the Social Security portion, whereas there’s no limit for Medicare. If you earn over $200,000 as a single filer, you might face an additional 0.9% Medicare tax. How Much Should My LLC Set Aside for Taxes? You should set aside about 25% to 30% of your LLC’s net income for taxes. This estimate covers federal income taxes, self-employment taxes, and potential state taxes, which can vary considerably. If you have employees, remember to factor in payroll taxes as well. Utilizing deductions like the Qualified Business Income deduction can help reduce your taxable income, allowing you to lower the amount you need to reserve for taxes effectively. Conclusion Grasping small business tax rates is essential for effective financial planning. By recognizing the differences between federal and state taxes, along with the implications of various business structures, you can better navigate your tax obligations. Implementing strategies to minimize your tax burden and maintaining accurate records will further streamline compliance. Utilizing available resources for tax assistance can help guarantee you remain informed and prepared for any changes in tax regulations, finally supporting your business’s financial health. Image via Google Gemini and ArtSmart This article, "Small Business Tax Rate?" was first published on Small Business Trends View the full article

-