All Activity

- Past hour

-

A reader writes: As part of a leadership development opportunity offered by my organization, I’ve been given the chance to participate in a 360 review process. For context, I report to a member of the C-suite and have been angling for a promotion (which would entail a new role basically being created for me), and the 360 was brought up by my supervisor and our CEO as a growth investment. I consider myself to be very self aware, so most of the things that came up in the process are not surprising to me, but I’m also very sensitive to criticism, especially from higher-ups. I am very professional and am able to calmly hear the feedback when it’s given, but with this 360, I’m finding myself spiraling. I received the written summary and skimmed the positive, but have read and reread the criticisms. I’m devastated to see the critical feedback from C-suite members in particular, and now have a twofold challenge: one, how do I become better at hearing critical feedback without taking it so personally? And two, how do I get the most out of what is being billed as a leadership/growth opportunity and transform the critical elements of the 360 into something constructive? Years ago, I was coaching a manager with a similar sensitivity to criticism, who was similarly upset about the feedback in a 360. Interestingly, when I read it through, the majority of what was in there was positive, but she couldn’t stop focusing on the (relatively small amount of) things people thought she could do to improve, and she felt like a failure. I asked her to take a yellow highlighter and highlight everything positive — which left her with a document that was about 90% yellow, which made it visually impossible for her to ignore the actual balance of the input her colleagues had offered, despite what her brain had been trying to do. She has told me in recent years that she still keeps that highlighted document as a reminder for herself. Can you try something similar and see if that changes the way it’s landing with you? I’m sure you don’t think that you’re flawless or have no areas where you can grow, and if you can correctly place those areas within the broader context of all the things people say you do well, it generally gets a lot easier to feel comfortable with this type of document as a whole, and to see it realistically. The other thing is: we all have areas where we can do better, and it’s actually a favor for people to be willing to tell you what those are! I know the whole “feedback is a gift” framing feels cheesy … but feedback really is a gift if you’re someone who wants to get better and better at what you do. I was going to add “as long as they offer it reasonably politely,” but I actually think even feedback that’s not diplomatically stated can be a gift, if you choose to see the value in hearing unvarnished input. That’s true even when you disagree with the feedback — because, if nothing else, it gives you useful info about how you’re coming across to someone else. You might ultimately consider that info and decide it doesn’t matter, but it’s still valuable to have it. The post I’m terrible at receiving negative feedback — and am spiraling from my 360 review appeared first on Ask a Manager. View the full article

-

Forget AI replacing human artists—The Devil Wears Prada 2 just proved that human artists can replace AI. The new movie, a long-awaited sequel to 2006’s The Devil Wears Prada, sees the return of star Meryl Streep as iconic fashion editor Miranda Priestly. It begins with Priestly in a PR crisis, sparking a slew of online hate. That includes memes like an image of Priestly dressed as a fast food worker captioned, “Would you like lies with that?” The image is only briefly on screen, and at first glance, many moviegoers assumed it was AI-generated. After all, on the internet of 2026, it most likely would be—an internet troll likely isn’t going out of their way to craft the image by hand. But after The Devil Wears Prada 2 hit theaters on May 1, digital artist Alexis Franklin took to social media to set the record straight: She’s the one who created the artwork, not AI, at the request of director David Frankel. On Instagram, Franklin posted the artwork along with a timelapse of her digital painting process. “Absolutely no disrespect to Queen Meryl, but this is something I would’ve painted in my free time, so when they asked me to do this it was nothing but fun,” she wrote in the caption. Franklin also shared her art on X, writing that her Instagram post had been “flooded with comments of relief that this gag in The Devil Wears Prada 2 was created by an actual human (me), so I figured I’d also post it here because I think these companies should get their flowers when they hire an artist.” ‘People do crave real art’: Social media celebrates human artists The story behind Franklin’s artwork quickly went viral, with her X post amassing 3.7 million views. Many users praised the Devil Wears Prada 2 team for staying true to the pro-artistry message of their film and hiring a human artist, even when using an AI-generated image would have made sense for the plot. “This is genuinely one of the coolest things I’ve seen a movie do,” reads one viral response. “Would’ve been so easy to AI generate something for the movie but they held themselves to a higher standard which I really really respect.” “People do crave real art and not AI slop and this is a proof,” wrote another user. A third user said they hope other films will follow in The Devil Wears Prada 2’s footsteps when it comes to telling stories about AI. “There’s a reason that it always disappoints me to no end when people assume that the only way to portray AI in a movie is by actually using AI,” they wrote. “Clearly alternatives always exist.” An accidental statement against AI Though social media largely assumed Franklin’s art was intentionally replicating AI’s signature art style, she’s since clarified that any similarities to AI were totally coincidental. In a series of follow-up posts on X, Franklin emphasized that she “was not told to mimic AI” and the aspects of her drawing people assumed were nods to AI, including the blurred lettering and font inconsistencies in the background, were just meant to be impressionistic. “I was just hired to create a cheap meme and the context of the movie has everyone, understandably, thinking I was emulating AI,” Franklin wrote. In an email to NBC News, Franklin said she understands where people’s suspicions come from, but that assuming human-made art is AI can have real, negative consequences for artists. “This mass hypervigilance prevails because people don’t want to be fooled, leading them to see signs on the walls that aren’t really there or that have very simple, reasonable explanations,” she wrote. “And it’s hard to know what the solution is.” “AI is so prevalent now, it feels like people have forgotten how it got that good—it studied us,” Franklin added. “The techniques it uses are ours!” View the full article

-

On a March afternoon, artificial intelligence detected something resembling smoke on a camera feed from Arizona’s Coconino National Forest. Human analysts verified it wasn’t a cloud or dust, then alerted the state’s forest service and largest electric utility. One of dozens of AI cameras installed for the utility Arizona Public Service had spotted early signs of what came to be known as the Diamond Fire. Firefighters raced to the scene and contained the blaze before it grew past 7 acres (2.8 hectares). As record-breaking heat and an abysmal snowpack raise concerns about severe wildfires, states across the fire-prone West are adding AI to their wildfire detection toolbox, banking on the technology to help save lives and property. Arizona Public Service has nearly 40 active AI smoke-detection cameras and plans to have 71 by summer’s end, and the state’s fire agency has deployed seven of its own. Another utility, Xcel Energy in Colorado, has installed 126 and aims to have cameras in seven of the eight states it serves by year’s end. “Earlier detection means we can launch aircraft and personnel to it and keep those fires as small as we can,” said John Truett, fire management officer for the Arizona Department of Forestry and Fire Management. Where there are fewer eyes, AI looks for fires ALERTCalifornia is a network of some 1,240 AI-enabled cameras across the Golden State that work similar to the system in Arizona. Human intervention keeps the risk of false positives low and trains the technology to become more accurate, said Neal Driscoll, geology and geophysics professor at the University of California, San Diego, and founder of ALERTCalifornia. “The AI that’s being run on the cameras is actually beating 911 calls,” he said. In Arizona, California, and beyond, the technology is mostly used in high-risk areas that are sparsely populated, rural or remote, where a blaze might not be quickly spotted by human eyes. “It’s just the ones where we won’t get a 911 call for a long time, it is extremely helpful to have that AI always monitoring that camera,” said Brent Pascua, battalion chief for the California Department of Forestry and Fire Protection, or Cal Fire. “In many cases, we’ve started a response before 911 was even called, and in a few cases, we’ve actually started a response, went there, put the fire out, and never received a 911 call.” A technology driven by worsening blazes Pano AI, whose technology combines high-definition camera feeds, satellite data, and AI monitoring, has seen a growing interest in its cameras since launching in 2020. They’ve been deployed in Australia, Canada and 17 U.S. states, including Oregon, Washington and Texas. Its customers include forestry operations, government agencies and utilities, including Arizona Public Service. Last year, its technology detected 725 wildfires in the U.S., the company said. “In many of these situations, we hear from stakeholders that the visual intelligence, the time, really, really gives them a head start and some of these could have taken off into hundreds if not thousands of acres,” said Arvind Satyam, the company’s co-founder and chief commercial officer. Cindy Kobold, an Arizona Public Service meteorologist, said the technology notifies them about 45 minutes faster on average than the first 911 call. Satyam said development of the technology was driven by the lack of hardened solutions to combat worsening wildfires. Climate change — caused by burning oil, gas, and coal — is warming the planet and fueling dry conditions that supercharge infernos, making them burn hotter, faster, and more frequently. The technology helps firefighters to safely and effectively respond while protecting communities and infrastructure, he said. Challenges and limitations One of the biggest obstacles to implementation is the price tag; Pano AI, for instance, charges around $50,000 annually per camera. The cost also includes fire risk analysis and 24/7 intelligence center. False alarms present a challenge, which can be costly in terms of time and attention, said Patrick Roberts, a senior researcher with the nonprofit research group RAND who recently finished a project on accelerating innovation in wildfire management. And when the AI accurately detects a fire, it doesn’t tell stakeholders the best course of action. “Do you send help right away? Do you monitor? Should you worry about it? Where do you send help? Do you think about evacuation? All this still requires people and decision support systems,” said Roberts. In highly populated areas, people tend to spot and call in fires pretty quickly, and the tech is not so useful when extreme weather events, such as hurricane-force winds, intensify and rapidly shift the flames, as happened in Los Angeles last year. Pascua says the technology complements Cal Fire’s work. “As the fire moves and shifts around, that’s where the human factor comes in and decides which tactics are best in fighting the fire. AI can only do so much,” he said. “It just provides that real time information where we can make better decisions on the fire ground.” AI firefighting assistance is not limited to detection AI can also be employed to identify the best places to thin vegetation and burn cool fires, and even to monitor air quality for signs of smoke, just like your home’s carbon monoxide sensor, said Roberts, but “1,000 times more sensitive.” At George Mason University in Virginia, professor Chaowei “Phil” Yang is working with researchers from California State University of Los Angeles, the city of LA and NASA Jet Propulsion Laboratory to create a system that forecasts where a fire will burn and which communities will be hardest hit by smoke pollution. The idea is to give agencies real-time maps so they can make quick, life-saving decisions about evacuations, school and road closures, and send out early air quality warnings. Yang said they hope the technology will be operational in three years. “AI in wildfires, it’s no longer just speculative. It’s really being used,” said Roberts, and it’s use will only continue to grow. “The future is AI everywhere,” he said, “and the lines will blur between AI wildfire detection and just wildfire detection as the lines will blur in other areas of our life.” ___ The Associated Press receives support from the Walton Family Foundation for coverage of water and environmental policy. The AP is solely responsible for all content. For all of AP’s environmental coverage, visit https://apnews.com/hub/climate-and-environment —Dorany Pineda and Brittany Peterson, Associated Press View the full article

-

Comprehending the definition of a Limited Liability Company, or LLC, is essential for anyone pondering starting a business. An LLC offers personal liability protection for its members, meaning your personal assets are typically safe from business debts. It additionally allows profits to pass through to your personal tax return, avoiding double taxation. Nevertheless, there are benefits and drawbacks to evaluate. To make an informed decision, it’s important to explore how an LLC compares to other business structures. Key Takeaways An LLC, or Limited Liability Company, combines features of corporations and partnerships for operational flexibility and liability protection. Owners, known as members, enjoy personal liability protection against business debts, safeguarding their personal assets. LLCs benefit from pass-through taxation, meaning profits are taxed only on members’ personal tax returns, avoiding double taxation. Management can be either member-managed or manager-managed, offering flexibility in operational structure. Establishing an LLC requires filing Articles of Organization and creating an Operating Agreement to define roles and profit distribution. What Is a Limited Liability Company (LLC)? A Limited Liability Company (LLC) is a unique business structure that merges features of both corporations and partnerships, providing a blend of operational flexibility and personal liability protection for its owners, who are referred to as members. So, what’s meant by LLC? It’s a hybrid entity that allows profits to pass through to members’ personal tax returns, effectively avoiding the double taxation that corporations often face. An LLC can be owned by individuals, corporations, or even foreign entities, with no cap on the number of members involved. You have the option to manage an LLC either through its members or by appointed managers, offering significant operational flexibility. To form an LLC, you must file articles of organization with your state and might need to obtain an Employer Identification Number (EIN) for tax purposes. This structure effectively balances liability protection with operational ease. Benefits of an LLC Numerous advantages make forming a Limited Liability Company (LLC) an appealing choice for many entrepreneurs and small business owners. First and foremost, LLCs provide personal liability protection, ensuring your personal assets aren’t at risk for any business debts or legal obligations. You as well benefit from a flexible management structure, allowing for either member-managed or manager-managed operations, depending on your preferences. In addition, LLCs enjoy pass-through taxation, meaning profits are taxed only at the individual level, which helps you avoid the double taxation often faced by corporations. With fewer formalities and reporting requirements than corporations, maintaining your LLC is simpler, making it a practical option for busy entrepreneurs. Moreover, LLCs offer customizable profit distribution arrangements, enabling you to allocate earnings flexibly among members. If you’re interested, you can start your LLC in Texas by completing the LLC in Texas application online, making the process even more convenient. Drawbacks of an LLC Though Limited Liability Companies (LLCs) offer various benefits, there are also notable drawbacks that potential owners should reflect upon. One major issue is that LLCs may dissolve upon a member’s death or bankruptcy, complicating business continuity compared to corporations, which can exist indefinitely. Furthermore, you might face self-employment taxes on your earnings, increasing your tax burden relative to corporate structures. Without a well-defined operating agreement, roles can become unclear, leading to potential disputes among members. In addition, LLCs often have state-specific regulations and compliance requirements, including annual fees and reports, which add to the ongoing costs of maintaining your business. Finally, transferring membership typically requires approval from existing members, making ownership changes less flexible than in a corporation. When weighing the ltd vs llc choice, it’s crucial to reflect upon these drawbacks to make an informed decision. How to Start an LLC Starting an LLC involves several significant steps that lay the foundation for your business. First, choose a unique name that meets your state’s regulations and includes “LLC” or “Limited Liability Company.” Next, file the Articles of Organization with your state’s Secretary of State, including crucial details like your LLC’s name, address, and registered agent. After that, draft an Operating Agreement to clarify member roles and profit distribution. Don’t forget to obtain an Employer Identification Number (EIN) from the IRS for tax purposes and to open a business bank account. Finally, guarantee compliance with state regulations by acquiring any necessary licenses or permits and maintaining ongoing obligations. Here’s a quick overview of the steps: Step Description Choose a Business Name Verify it complies with state naming rules. File Articles of Organization Submit necessary documents to your state. Create an Operating Agreement Outline management and profit distribution. Obtain an EIN Required for taxes and banking. Guarantee Compliance Acquire licenses and maintain obligations. LLC vs. Corporation: Key Differences When comparing LLCs and corporations, grasping their key differences is vital for making informed business decisions. Here are some fundamental distinctions to reflect on: Ownership Structure: LLCs have members, whereas corporations have shareholders, affecting management and profit distribution. Management Flexibility: LLCs allow for member-managed or manager-managed options, whereas corporations require a board of directors and a structured hierarchy. Taxation: LLCs typically benefit from pass-through taxation, meaning profits are taxed only at the individual level, whereas corporations may face double taxation on profits. Ownership Transfer: LLCs offer more flexible ownership transfer governed by the operating agreement, whereas corporations have stricter regulations for transferring shares. Both LLCs and corporations provide limited liability protection, but corporations usually have more established legal precedents supporting this. Recognizing these differences can help you choose the right structure for your business. Frequently Asked Questions What Is an LLC Explained for Dummies? An LLC, or Limited Liability Company, combines benefits from corporations and partnerships. It protects your personal assets from business debts, meaning you’re not personally liable for losses. You can choose how it’s taxed, often avoiding double taxation. Forming an LLC involves selecting a unique name, filing Articles of Organization, and possibly creating an operating agreement. They’re flexible and require fewer formalities, making them ideal for small businesses and entrepreneurs. What Is a Simple Definition of LLC? An LLC, or Limited Liability Company, is a flexible business structure that combines personal liability protection with tax benefits. As a member, you enjoy limited liability, meaning your personal assets are typically safe from business debts. LLCs can be formed by one or more individuals or entities, and profits pass through to your personal tax return, avoiding double taxation. To establish an LLC, you file articles of organization and designate a registered agent for legal matters. What Is the Biggest Disadvantage of an LLC? The biggest disadvantage of an LLC is often the self-employment tax liability. If you actively participate in the business, your profits are subject to this tax, which can be significant. Moreover, LLCs can incur higher startup and maintenance costs compared to other business structures. Limited ownership transferability complicates succession planning, and raising capital may prove challenging since investors frequently prefer more established entities like corporations. Proper maintenance is vital to protect personal assets from business liabilities. What Are Three Things That LLCS Are Not Required to Do? LLCs aren’t required to hold annual meetings, which simplifies their management. You likewise don’t need to maintain extensive corporate records, unlike corporations. Furthermore, LLCs don’t have to file separate federal tax returns; profits are typically reported on your personal tax return, allowing for pass-through taxation. Although it’s advisable to have an operating agreement for clarity, it’s not mandatory, providing you with flexibility in managing your business structure. Conclusion In conclusion, a Limited Liability Company (LLC) offers a blend of liability protection and tax advantages, making it an attractive option for many business owners. As it provides benefits like flexible management and pass-through taxation, it is crucial to evaluate potential drawbacks, such as varying regulations and self-employment taxes. Starting an LLC involves specific steps, and grasping the differences between an LLC and a corporation can further guide your decision. With the right information, you can make an informed choice for your business structure. Image via Google Gemini This article, "Understanding the Company LLC Definition: A Simple Guide" was first published on Small Business Trends View the full article

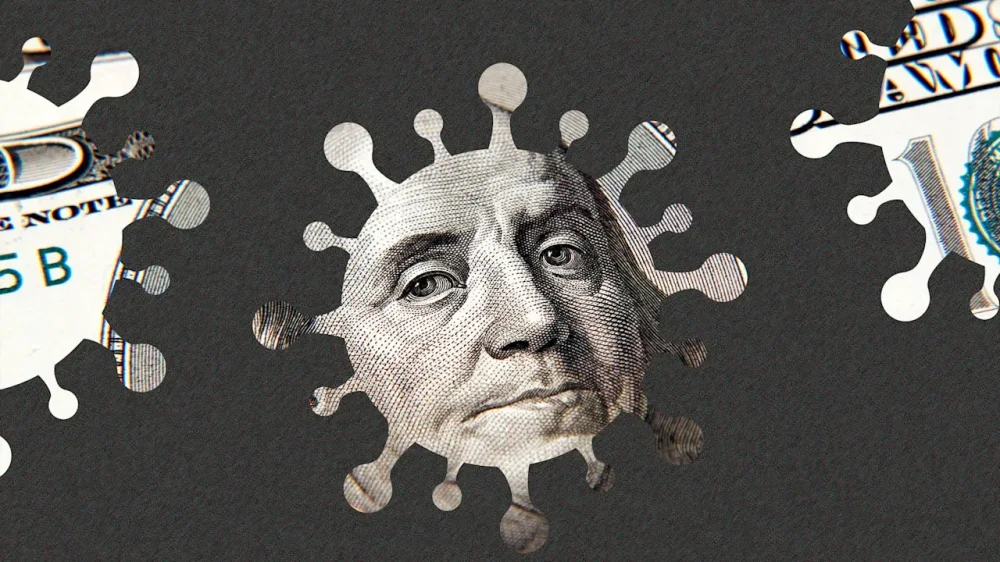

-

In a stark reminder of the vigilance required in managing federal relief programs, Marcus Eichelberger, a former pastor from Jacksonville, Florida, faces serious legal consequences for alleged wire fraud tied to the Paycheck Protection Program (PPP). The case highlights ongoing challenges for small business owners navigating relief programs designed to support them amid financial uncertainty. Eichelberger was indicted on four counts of wire fraud, which carries a potential sentence of up to 20 years in federal prison for each count. The indictment alleges that between March 2021 and February 2022, he and an associate submitted false applications for PPP loans. They purportedly claimed the funds would be used to maintain payroll and operational expenses for an unqualified business. Instead, the funds were allegedly diverted for personal use. U.S. Attorney Gregory W. Kehoe commented on the case, emphasizing the government’s commitment to safeguarding taxpayer-funded programs. “The U.S. Attorney’s Office is committed to prosecuting those who use fraud and deception to exploit our nation’s federal benefits programs,” he said. Such statements reinforce the growing scrutiny on loan applications, especially in the wake of widespread fraud in relief programs during the pandemic. The alleged activities surrounding Eichelberger’s case serve as a crucial alert for small business owners. The PPP was designed to offer financial relief during the COVID-19 pandemic, but the influx of funds also opened avenues for fraudulent claims. For entrepreneurs, this means that they must be particularly diligent in documenting and using funds according to the requirements set by the SBA. Moreover, the case is part of a larger investigative effort spearheaded by the Department of Justice’s National Fraud Enforcement Division, which aims to combat misuse of taxpayer dollars. “This case demonstrates the VA OIG’s unwavering commitment to detecting and preventing fraud,” remarked Special Agent in Charge David Spilker of the VA Office of Inspector General’s Southeast Field Office. This pronouncement not only underlines the seriousness of the allegations but also highlights the collaborative approach government agencies are taking to address fraud. While the PPP provided financial lifelines to many businesses, small business owners must consider the implications of this surveillance. Compliance with federal guidelines is paramount; failing to do so can lead to severe penalties, including prosecution. Misunderstanding the eligibility criteria or misusing the funds can result in not just repayment demands but significant criminal charges. Further complicating matters for small businesses, the landscape of federal aid continues to evolve. With new rounds of funding being introduced, being informed about the rules is essential. Keeping abreast of updates from the SBA and other relevant agencies can provide clarity, though navigating the details remains an ongoing challenge. Additionally, courts have reaffirmed the presumption of innocence until proven guilty, which is vital in cases like that of Eichelberger. Nevertheless, this underscores the fact that the burden of proof lies with individuals seeking federal funds. Detailed documentation and transparency are non-negotiable. For small business owners looking to secure funds through federal programs, diligence is key. It is not just essential to fill out the application properly; careful attention must be paid to how those funds are spent. Failure to comply could open a floodgate of issues, potentially endangering the very existence of a business that relies on such financial assistance. As the Department of Justice continues its crackdown on fraud, the consequences will likely resonate beyond those accused. Small business owners must remain aware of their responsibilities, the evolving regulatory environment, and the importance of ethical practices in securing federal funding. For more information on this case and ongoing fraud prevention efforts, you can visit the original U.S. Department of Justice press release here. Additionally, updates on SBA guidelines and related news can be found by signing up for the SBA OIG email updates here. Image via Google Gemini This article, "Former Jacksonville Pastor Indicted for Fraud in PPP Loan Scheme" was first published on Small Business Trends View the full article

- Today

-

Google Ads CTR is rising, but conversions remain flat. New Optmyzr data explains why performance is shifting and what it means for advertisers. The post Optmyzr Report Finds Google Ads Engagement Rising While Efficiency Holds appeared first on Search Engine Journal. View the full article

-

What Is Job Scheduling? Job scheduling is the process of planning, assigning and timing tasks so they are completed using available resources. It is commonly used in construction, manufacturing, maintenance and IT operations to organize work, coordinate labor and meet deadlines. Clear sequencing and resource allocation allow teams to execute work without delays or conflicts. What Is a Job Schedule? A job schedule is a structured plan that shows tasks, timelines and assigned resources for completing work. It is used to track when each task should start and finish, who is responsible and how activities are sequenced. By laying out dependencies and deadlines, it helps teams across industries coordinate execution and keep work moving without conflicts or delays. ProjectManager is an award-winning project management software that helps teams across industries plan, schedule and track work from start to finish. Create detailed job schedules, manage resources, monitor costs and compare planned versus actual performance with a full suite of powerful tools including Gantt charts, kanban boards, real-time dashboards and much more. Get started for free today. /wp-content/uploads/2024/03/Manufacturing-gantt-chart-light-mode-costs-exposed-cta-e1712005286389-1600x659.jpgLearn more What Industries Use Job Scheduling? Job scheduling is used anywhere work needs to be planned, sequenced and executed using limited resources. While the core principles remain the same, how schedules are built and managed varies depending on the type of work, the level of complexity and how resources are deployed. Construction On construction projects, job scheduling coordinates crews, equipment and subcontractors across multiple phases of work. Tasks must follow a strict sequence, as many activities depend on others being completed first. Delays in one area can impact the entire project, so schedules are continuously updated to reflect progress and keep work aligned with deadlines. Manufacturing Within manufacturing operations management, job scheduling organizes production tasks across machines, workstations and operators. Each job may follow a different process, requiring careful sequencing to avoid bottlenecks. Schedules must account for setup times, material availability and production capacity to ensure consistent output and prevent disruptions on the production line. IT and Software Development In IT projects, job scheduling is used to manage automated tasks, system processes and development workflows. Tasks such as data processing, system updates and deployments must run in a specific order to avoid conflicts. Schedules help teams coordinate dependencies, manage system loads and ensure that critical operations run at the right time. Maintenance and Field Service Maintenance planning teams rely on job scheduling to plan inspections, repairs and preventive work across multiple assets and locations. Schedules must balance urgent requests with routine service tasks while ensuring technicians and equipment are available. Effective scheduling reduces downtime, improves response times and helps maintain consistent asset performance. /wp-content/uploads/2026/01/Printable-Gantt-chart-template.jpg Get your free Gantt Chart Template Use this free Gantt Chart Template for Excel to manage your projects better. Download Excel File Why Job Scheduling Matters Across construction sites, production floors and service operations, job scheduling determines how work actually gets done day to day. Poor coordination leads to idle crews, missed deadlines and wasted materials, while structured scheduling aligns resources with demand. Teams that actively manage schedules can respond faster to changes and maintain steady progress without constant disruption. Efficient job scheduling ensures that labor, equipment and materials are allocated at the right time, preventing costly downtime and improving overall productivity across projects. Clear scheduling structures help teams avoid task conflicts and overlapping responsibilities, reducing confusion and ensuring that work progresses in a logical and controlled sequence. Accurate job schedules make it easier to meet deadlines by aligning task durations with realistic timelines, helping teams avoid delays that can impact project budgets and client expectations. Well-managed schedules improve resource utilization by balancing workloads across teams, preventing overloading some workers while others remain underutilized or idle. Structured job scheduling provides better visibility into ongoing work, allowing managers to track progress, identify bottlenecks early and make adjustments before issues escalate. Consistent scheduling practices support better cost control by reducing inefficiencies, minimizing rework and ensuring that resources are used effectively throughout the project lifecycle. Reliable job schedules create a foundation for better decision-making by providing real-time insight into project status, enabling teams to adapt quickly to changes in scope or priorities. What Should Be Included in a Job Schedule? Before work begins, a job schedule needs to clearly show what will be done, when it will happen and who is responsible. A complete structure removes guesswork during execution and gives teams a reliable reference point to track progress, adjust priorities and keep work aligned with deadlines. Job or Task Name: Each activity must be clearly labeled so teams can quickly identify what work needs to be performed without confusion. Task Description: A short explanation provides context on what the task involves, helping ensure consistency in how the work is executed. Start Date and Time: Defines exactly when a task is scheduled to begin, allowing teams to plan resource availability and sequencing. End Date and Time: Establishes when the task should be completed, creating clear expectations for delivery and progress tracking. Task Duration: The estimated time required to complete the task, which supports realistic scheduling and workload balancing. Assigned Resources: Identifies the workers, teams or equipment responsible for completing the task, ensuring accountability and coordination. Task Dependencies: Shows relationships between tasks, indicating which activities must be completed before others can start. Priority Level: Highlights the importance or urgency of each task so teams can focus on critical work first when conflicts arise. Status: Tracks whether tasks are not started, in progress or completed, giving real-time visibility into execution. Work Hours or Effort: Captures the amount of labor required, helping managers distribute workloads and avoid overallocating resources. Location or Work Area: Specifies where the task takes place, which is essential for coordinating teams across multiple sites or departments. Materials and Equipment Needed: Lists required inputs so teams can prepare in advance and avoid delays caused by missing resources. Constraints or Restrictions: Identifies limitations such as deadlines, regulations or resource availability that may impact how the task is performed. Notes or Instructions: Provides additional guidance or special considerations that help teams execute the work correctly and consistently. Job Schedule Example Consider a small construction project involving site preparation, foundation work and structural framing. The team needs to coordinate labor, materials and equipment across sequential tasks. A clear job schedule ensures each activity is properly timed, resources are available when needed and work progresses without delays or conflicts. Job or Task Name Task Description Start Date and Time End Date and Time Task Duration Assigned Resources Task Dependencies Priority Level Work Hours or Effort Materials and Equipment Needed Site Clearing Remove debris and prepare the site for construction activities 06/01/26 07:00 06/01/26 12:00 5 hours Ground crew, bulldozer None High 10 labor hours Bulldozer, safety gear Excavation Dig foundation trenches according to site plans 06/01/26 13:00 06/02/26 12:00 1 day Excavation crew, excavator Site Clearing High 16 labor hours Excavator, measuring tools Foundation Pouring Pour concrete into prepared trenches 06/02/26 13:00 06/02/26 18:00 5 hours Concrete crew, mixer Excavation High 12 labor hours Concrete, mixer, rebar Curing Time Allow concrete to set and reach required strength 06/02/26 18:00 06/05/26 18:00 3 days No active crew Foundation Pouring Medium 0 labor hours Curing blankets Framing Build structural framework of the building 06/06/26 07:00 06/10/26 17:00 5 days Carpenters, tools Curing Time High 80 labor hours Lumber, nails, power tools Job Scheduling Process Getting from a vague scope of work to a clear, executable plan requires a structured approach. A well-defined job scheduling process helps teams organize tasks, sequence activities and align resources so work progresses in a controlled and predictable way. 1. Define the Job to Be Performed Before anything is scheduled, the team must fully understand the job that will be performed. That means clarifying what work will be done, what goals and objectives need to be achieved and who the stakeholders are. Without this clarity, schedules become disconnected from reality and fail to support execution effectively. 2. Break Down the Job Into Individual Tasks Once the job is clearly defined and understood by both leadership and the team responsible for execution, the next step is to divide the work into manageable tasks. Breaking down the scope of work allows each activity to be assigned, tracked and completed with clarity, reducing confusion and making the schedule easier to follow. 3. Identify Task Dependencies Task dependencies determine the sequence in which work must be performed, giving the job schedule its logical structure. Some tasks cannot begin until others are completed, and recognizing these relationships is essential. There are four main types of task dependencies, and understanding them helps create a realistic and executable schedule. 4. Estimate the Duration of Tasks Estimating task durations allows schedulers to build a realistic project timeline and understand how long the job will take overall. Methods such as expert judgment, historical data, CPM and PERT can be used. Since estimates rarely match actual results, comparing planned durations against real performance is critical during execution. 5. Create a Timeline for the Execution of the Job With task durations defined, the next step is to assign start and end dates to each activity so the full timeline becomes visible. This timeline represents the job schedule that stakeholders will review and rely on. It also establishes a schedule baseline that allows teams to track progress and measure performance throughout execution. 6. Assign Resources for the Completion of Tasks After the timeline is established, resources must be assigned to ensure each task can be completed as planned. This includes human resources such as workers and supervisors, as well as non-human resources like materials, equipment and components. Aligning these inputs with the schedule ensures that work can proceed without interruptions. 7. Estimate Resource Costs Once resources are allocated, the next step is to estimate the costs associated with labor, materials and equipment. These projections provide a financial view of the job schedule and help guide decision-making. Because actual costs often vary from estimates, tracking real expenses is essential to maintain control over the budget. 8. Monitor Progress, Costs and Timelines As work moves forward, performance must be tracked against the original plan to keep the job on course. Reviewing progress, timelines and costs together allows teams to identify deviations early and take corrective action. Continuous monitoring ensures that adjustments are based on real data rather than assumptions, keeping execution aligned with expectations. What Tools Can Be Used for Making a Job Schedule? Different tools can be used to build and manage a job schedule depending on the complexity of the work and the level of control required. The right tool helps teams visualize tasks, organize timelines and coordinate resources without losing track of dependencies or deadlines. Gantt Charts Gantt charts are one of the most effective tools for building a job schedule because they visually map tasks across a timeline. Teams can see start and end dates, task durations and dependencies in one place. This makes it easier to sequence work, adjust schedules and quickly understand how delays in one task affect the overall timeline. /wp-content/uploads/2023/01/Gantt-Manufacturing-Light-2554x1372-1-1600x860.png Kanban Boards Kanban boards help teams manage a job schedule by organizing tasks into visual columns that represent different stages of work. As tasks move from one stage to another, teams can track progress in real time. This approach is especially useful for managing workflows that require flexibility and continuous updates rather than rigid timelines. /wp-content/uploads/2023/01/Kanban-Manufacturing-Light-2554x1372-1-1600x860.png Task Lists Task lists provide a simple way to create and manage a job schedule by outlining tasks, deadlines and assigned resources in a structured format. They are easy to update and ideal for smaller jobs or teams that do not need complex scheduling tools. With clear priorities and deadlines, task lists help keep work organized and on track. /wp-content/uploads/2024/05/Sheet-light-mode-punch-list-construction-custom-columns-costs-hours--1600x875.png Types of Job Scheduling Different scheduling approaches are used depending on deadlines, resource availability and how work flows through an operation. Choosing the right method helps teams structure timelines, prioritize tasks and adapt to constraints without disrupting execution. Forward Job Scheduling Forward job scheduling is a scheduling method used to plan tasks from the present time into the future based on available resources. It is commonly used when work can begin immediately and the goal is to complete jobs as early as possible. Tasks are scheduled in sequence as resources become available, often resulting in earlier completion but potential idle time between activities. Backward Job Scheduling Backward job scheduling is a scheduling method used to plan tasks by starting from a fixed deadline and working backward. It is commonly used when delivery dates are predetermined and meeting them is the priority. Tasks are scheduled as late as possible without delaying completion, reducing idle time but requiring accurate duration estimates. Job Shop Scheduling Job shop scheduling is a scheduling method used to organize tasks across multiple jobs that follow different workflows and sequences. It is commonly used in environments where each job has unique requirements and must pass through shared resources. This approach requires careful coordination to manage resource conflicts and maintain efficient task sequencing. Batch Job Scheduling Batch job scheduling is a scheduling method used to group similar tasks and process them together within a defined time period. It is commonly used when tasks share the same requirements or resources and can be executed in cycles. Grouping work into batches improves efficiency by reducing setup time and optimizing resource usage. Free Job Scheduling Templates We’ve created over 100 free project management templates for Excel, Word and Google Sheets. Here are some that can help with job scheduling. Gantt Chart Template This Gantt chart template helps plan and visualize job schedules by mapping tasks, timelines and dependencies, making it easier to track progress, coordinate resources and keep work aligned with deadlines. Critical Path Template This critical path template identifies the sequence of tasks that directly impact completion time, helping teams prioritize critical activities, reduce delays and maintain control over project timelines and execution. PERT Chart Template This PERT chart template helps estimate task durations and visualize dependencies, allowing teams to analyze uncertainty, plan realistic schedules and improve decision-making when managing complex job scheduling scenarios. ProjectManager Is a Robust Job Scheduling Software ProjectManager is an online project management solution that provides a complete set of work planning, scheduling and tracking tools, including Gantt charts, kanban boards, task lists and real-time dashboards and reports. With these features, teams across industries can build detailed job schedules, assign resources and monitor progress, costs and timelines. ProjectManager also delivers AI-powered project insights to support better decision-making and connects with over 100 tools like Microsoft Project, Acumatica and Power BI. With its open API and wide range of integrations, organizations can seamlessly link ProjectManager to their existing systems. Watch the video below to learn more! Related Job Management Content How to Make a Job Cost Report for Construction Job Card Template What Is Job Costing? How to Make a Job Cost Sheet (Example Included) 10 Best Job Tracking Software of 2026 (Free & Paid) If you need a tool to help you manage projects, then signup for our software now at ProjectManager. Our online software helps teams across industries plan, track and oversee projects as they unfold. Sign up for a free 30-day trial today! The post Job Scheduling 101: Making a Job Schedule appeared first on ProjectManager. View the full article

-

Term financing is a structured funding option that gives businesses a lump sum of capital to invest in growth or significant projects. You’ll repay this amount over a set period, often through fixed or variable payments that include interest. This type of financing can be advantageous for long-term financial planning, but it’s crucial to understand its various types and features. What should you consider before applying for this form of financing? Key Takeaways Term financing provides a lump sum of cash that is repaid over a set period through regular payments, often requiring collateral. It includes various loan types: short-term, medium-term, long-term, and specialized loans like balloon or step-up repayment loans. The approval process assesses creditworthiness, requiring strong financial statements and an evaluation of collateral. Repayment structures are fixed, with payments typically made monthly or quarterly, depending on the loan duration. Term financing is suitable for significant investments, predictable revenue streams, and consolidating high-interest debts. What Is Term Financing? Term financing is an essential funding option that provides businesses with a lump sum of cash, which they repay over a set period through regular payments. This financing can be categorized into different types, such as term loan A versus term loan B, depending on the structure and terms. Term loans typically require collateral, which may include business assets or personal guarantees, and the approval process is rigorous to evaluate creditworthiness. The duration of term financing varies; short-term loans last less than a year, whereas intermediate-term loans span one to three years, and long-term loans can extend from three to 25 years. Interest rates can be fixed or variable, and costs are reflected in the annual percentage rate (APR), including any fees. Businesses often use term financing for significant investments in fixed assets, like equipment purchases and operational expansions, making it a critical option for growth. Key Features of Term Financing When considering financing options, comprehension of the key features of term financing can greatly improve your decision-making process. Term financing offers distinct characteristics that can help you manage your business’s financial needs effectively: Provides a lump sum of capital upfront, which you repay over a set period, usually with fixed or variable interest rates. Features structured repayment schedules, typically with monthly or quarterly payments that include both principal and interest. Offers a range of loan durations: short-term (less than a year), intermediate-term (one to three years), and long-term (three to 25 years). Often requires collateral, like business or personal assets, which can lower interest rates and reduce lender risk. Understanding these key features allows you to make informed choices and better plan your finances, ensuring that your business remains on a stable path throughout the loan period. Types of Term Financing Several types of term financing are available, each designed to meet specific business needs and timelines. Comprehending these options can help you make informed decisions for your business. Type of Loan Duration Purpose Short-Term Loans A few months to 2 years Immediate needs like inventory purchases Medium-Term Loans 2 to 5 years Equipment purchases or modest expansions Long-Term Loans Over 5 years (up to 25) Significant investments such as real estate Balloon Loans Varies Smaller payments with a large final payment Step-Up Repayment Loans Varies Lower initial payments that increase over time Short-Term Financing Explained Short-term financing is a valuable option for businesses needing quick access to capital to address immediate financial challenges. Typically lasting less than one year, this type of financing is perfect for situations like: Seasonal inventory purchases Urgent operational expenses Managing cash flow fluctuations Covering unexpected costs While short-term loans provide rapid approval with less documentation, they often come with higher monthly payments and steeper interest rates. This makes them more suitable for businesses that can rely on consistent near-term revenue, ensuring that repayments won’t strain cash flow. Nevertheless, it’s vital to manage these loans carefully, as accumulating high-interest costs can pose risks if not handled properly. Overall, short-term financing can deliver quick relief, but comprehending its implications is key for maintaining financial health. Intermediate-Term Financing Explained Intermediate-term financing serves as a practical solution for businesses seeking to fund specific projects or acquisitions over a period of one to three years. This type of financing is commonly used for purchasing equipment or modest expansions. Repayment typically occurs through manageable monthly payments based on your business’s cash flow, making it easier to budget. Interest rates for intermediate-term loans are typically lower than those for short-term loans, providing a cost-effective financing option. Nevertheless, many lenders require collateral, which might include business assets or personal guarantees to reduce risk. The structured repayment schedule aids in effective cash flow management throughout the loan duration. Here’s a quick overview of intermediate-term financing: Feature Description Loan Duration 1 to 3 years Repayment Frequency Monthly payments Interest Rates Typically lower than short-term loans Collateral Requirements Business assets or personal guarantees Typical Uses Equipment purchase, modest expansions Long-Term Financing Explained Long-term financing is a crucial option for businesses aiming to invest considerably in their future without the immediate pressure of repayment. Typically, these loans have repayment periods ranging from three to 25 years, allowing for significant investments in fixed assets. Here are some key points to reflect on: Loans often require collateral, such as business assets or personal guarantees, to secure the lender’s investment. Interest rates can be fixed or variable, providing predictability in monthly payments. Maximum loan terms vary; real estate loans may extend up to 25 years, whereas other types may be shorter, around 10 years. Long-term financing is ideal for substantial expenditures like purchasing commercial real estate, equipping facilities, or funding major business expansions. Benefits of Term Financing Term financing offers numerous advantages that can greatly benefit businesses looking to invest in their growth. It provides access to substantial capital, enabling you to make significant investments in equipment, real estate, or expansion projects that mightn’t be feasible with smaller funding options. With predictable repayment schedules, term financing aids your budgeting and cash flow management, allowing you to plan for fixed monthly or quarterly payments. Typically, it offers lower interest rates compared to other financing methods, such as credit cards, which can help reduce your overall borrowing costs. By securing larger amounts of capital through term financing, you can facilitate growth initiatives, like entering new markets or upgrading technology, enhancing your competitiveness. Finally, successfully repaying term loans can positively impact your credit score, creating opportunities for future financing at more favorable terms. Drawbacks of Term Financing When considering term financing, you should be aware of several drawbacks that could impact your business. First, the need for collateral means you might risk valuable assets if you can’t make payments. Furthermore, rigid repayment structures and qualification challenges can add stress to your financial planning, especially during tough economic times. Collateral Risks Involved Collateral risks are a significant concern for businesses evaluating term financing, as they often require assets or personal guarantees to secure the loan. If you default, the lender can seize these assets, which might jeopardize your operations. Here are some key risks to bear in mind: You could lose vital business assets or even personal property. Your access to financing may be limited if you lack sufficient collateral. Defaulting on a loan could lead to severe personal financial repercussions. Strained cash flow from rigid repayment terms can increase the risk of default during tough times. Understanding these risks is important before committing to term financing to guarantee that you’re making informed decisions for your business’s future. Rigid Repayment Structures Despite having a structured repayment plan may seem beneficial, the rigidity of these schedules in term financing can pose significant challenges for your business. Fixed repayment schedules require consistent monthly or quarterly payments, which might strain your cash flow during slower periods. This lack of flexibility makes it tough to adjust payments based on fluctuating revenues or unexpected expenses. If you encounter financial difficulties, the obligation to make regular payments can increase stress and lead to default risks. Furthermore, prepayment penalties could limit your ability to adjust your repayment strategy. Strict repayment terms can likewise hinder your chances of securing additional financing, as lenders may view existing debt as a risk factor. Challenge Impact on Business Fixed Repayment Schedules Strained cash flow Lack of Flexibility Difficulty adjusting payments Default Risks Increased financial stress Qualification Challenges for Borrowers Securing term financing often involves maneuvering through a complex terrain of qualification challenges that can be overwhelming for many borrowers. You may encounter several hurdles, including: Stringent qualification requirements, demanding a strong credit history and solid financial statements. Collateral demands, which could put your business assets or personal guarantees at risk if you default. Difficulties for startups and newer businesses, often struggling because of a lack of established creditworthiness. Lengthy approval processes that can deter you, especially if you need quick access to capital. These challenges can make obtaining term financing an intimidating experience, as you navigate strict criteria and potential risks that may affect your financial stability. How Term Financing Works When you pursue term financing, the process begins with an application and approval phase, where lenders assess your financial health and creditworthiness. Once approved, you’ll receive a lump sum that you’ll repay through a structured schedule of fixed or variable payments over a set period, which can range from a few months to several years. Moreover, comprehending interest rates and any associated fees will help you grasp the total cost of your loan, ensuring you’re fully aware of your financial obligations. Application and Approval Process To obtain term financing, you’ll need to navigate a structured application and approval process designed to assess your creditworthiness and the financial health of your business. Typically, you’ll need to gather and submit: Financial statements Business plans Personal guarantees Tax returns and cash flow projections The lender reviews your application, focusing on these documents to determine your business’s viability. If approved, they’ll present you with terms that outline the loan amount, interest rate, repayment schedule, and any associated fees. Once you accept these terms, the lender disburses the agreed lump sum into your bank account, allowing you to utilize the funds for your planned business activities. This process is essential for ensuring both parties understand their commitments. Repayment Structure Explained Comprehending the repayment structure of term financing is crucial for managing your business’s financial obligations effectively. Typically, you’ll face fixed monthly or quarterly payments that include both principal and interest over a set period. The repayment schedule is established at the loan’s inception, varying by loan type—short-term loans usually require payments in less than a year, whereas long-term loans can extend up to 25 years. Here’s a quick overview of common repayment structures: Loan Term Payment Frequency Duration Short-term Monthly Medium-term Quarterly 1-5 years Long-term Monthly 5-25 years Flexible option Varies Depends on agreement Understanding this structure helps you plan your cash flow effectively. Interest Rates Overview Interest rates play a pivotal role in how term financing works, impacting the overall cost of borrowing. When you consider a term loan, you’ll typically encounter fixed or variable interest rates, which depend on your creditworthiness and market conditions at the time of your loan agreement. Here are some key points to remember: Interest rates for term loans are typically lower than those for credit cards. Monthly or quarterly payments include both principal and interest, with interest decreasing over time. Prepayment penalties may apply if you pay off the loan early, particularly for longer maturities. The Annual Percentage Rate (APR) provides a thorough view of the loan’s overall cost, combining interest and additional fees. Understanding these factors helps you make informed borrowing decisions. When to Consider Term Financing When should you evaluate term financing for your business? If you need significant capital for long-term investments, like purchasing equipment or broadening operations, term financing may be a good fit. It allows predictable repayment over time. Furthermore, if your business has a stable revenue stream, you can support consistent monthly or quarterly payments without straining cash flow. Term financing is also helpful for consolidating high-interest debts into a single payment, potentially lowering interest rates. In addition, if you have a solid business plan and strong financial statements, term loans can provide access to larger sums of capital. Finally, businesses financing real estate purchases or major renovations should contemplate long-term term loans, which can extend repayment periods up to 25 years. When to Evaluate Term Financing Benefits Significant long-term investments Predictable repayment Stable revenue stream Support for consistent payments Debt consolidation Lower overall interest rates Real estate financing Extended repayment terms Tips for Applying for Term Financing When applying for term financing, it’s vital to prepare fundamental financial documentation, like tax returns and bank statements, to showcase your business’s creditworthiness. Furthermore, consider applying with multiple lenders so you can compare interest rates, terms, and fees, which may lead to better financing options. Prepare Financial Documentation Applying for term financing requires careful preparation of financial documentation that showcases your business’s financial health and stability. To improve your chances of approval, gather the following crucial documents: Recent tax returns, profit and loss statements, and balance sheets to demonstrate financial health. A detailed business plan outlining how you’ll use the loan, projected cash flow, and anticipated growth. Personal financial documentation, including tax returns and credit history, as many lenders require personal guarantees. Existing loan documentation to illustrate current debt obligations, helping lenders assess overall financial stability and repayment capacity. Compare Multiple Lenders Securing the right term financing requires a careful evaluation of various lenders to identify the best fit for your business. Gather quotes from at least three lenders to compare interest rates, repayment terms, and fees. Remember, it’s not just about the interest rate; consider the total loan cost, including origination fees and any prepayment penalties. Each lender has different qualification requirements, which can affect your approval chances based on your financial health. Review the fine print in loan agreements for covenants that may impact your operations. Fortifying your application with financial documents like tax returns and cash flow statements can greatly improve your credibility. Lender Interest Rate Fees Repayment Terms Lender A 5.5% $500 5 years Lender B 6.0% $300 7 years Lender C 5.8% $400 6 years Frequently Asked Questions What Is Term Financing? Term financing is a borrowing method where you receive a lump sum from a lender, which you repay over a set period. This type of financing is ideal for large purchases, like equipment or real estate. The repayment includes both principal and interest, making it easier for you to plan your finances. Typically, you’ll need to provide collateral and undergo a credit assessment to secure the loan, which helps mitigate lender risk. Is a Term Loan Good or Bad? A term loan can be both good and bad, depending on your business’s financial situation. It offers predictable monthly payments and often lower interest rates, which can be appealing for long-term investments. Nevertheless, it may require collateral, risking your assets if you fail to repay. Furthermore, the fixed repayment schedule can strain cash flow during slow periods, making it less suitable for short-term needs. Assess your stability and purpose before deciding. What Is Better, a Term Loan or a Line of Credit? Choosing between a term loan and a line of credit depends on your needs. If you’re making a large, one-time investment, a term loan may be better because of its lower interest rates and structured repayment schedule. On the other hand, if you need flexible access to funds for ongoing expenses or cash flow management, a line of credit provides that adaptability. Assess your financial goals and choose the option that aligns best with your situation. Can Term Loans Be Paid off Early? Yes, you can often pay off term loans early, but it depends on your specific loan agreement. Many loans allow for early repayment without penalties, which can help reduce overall interest costs. Nonetheless, some long-term loans may impose prepayment fees if paid off too soon, especially those with maturities of 15 years or more. Always review your loan terms carefully to understand any potential fees or restrictions regarding early payoff options. Conclusion In conclusion, term financing is a structured funding option that provides businesses with the capital needed for significant investments. By comprehending its key features, types, and potential drawbacks, you can make informed decisions about whether it’s right for your financial needs. When applying, guarantee you present a strong financial profile and a clear repayment plan. Finally, term financing can support your business growth when used strategically and responsibly. Image via Google Gemini and ArtSmart This article, "What Is Term Financing and How Does It Work?" was first published on Small Business Trends View the full article

-