ResidentialBusiness

Administrators

-

Joined

-

Last visited

Everything posted by ResidentialBusiness

-

Key components and how to optimize them. By Jackie Meyer Go PRO for members-only access to more Jackie Meyer. View the full article

Key components and how to optimize them. By Jackie Meyer Go PRO for members-only access to more Jackie Meyer. View the full article -

Key components and how to optimize them. By Jackie Meyer Go PRO for members-only access to more Jackie Meyer. View the full article

-

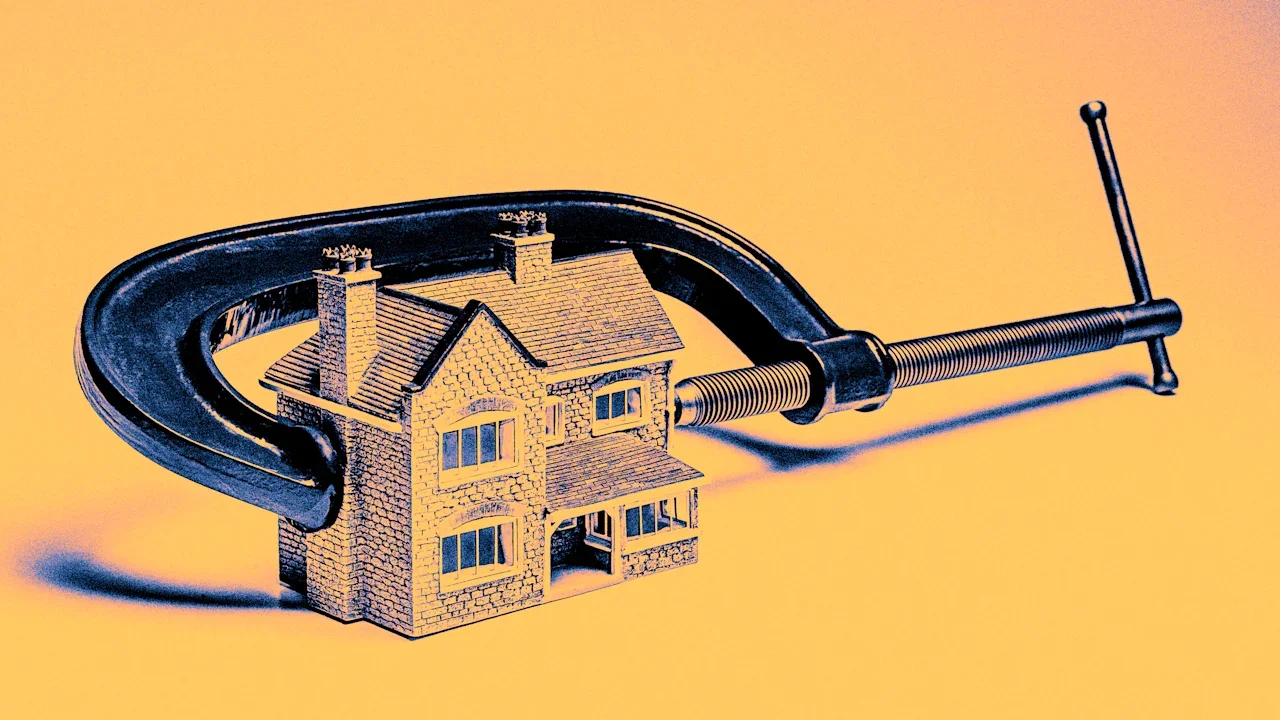

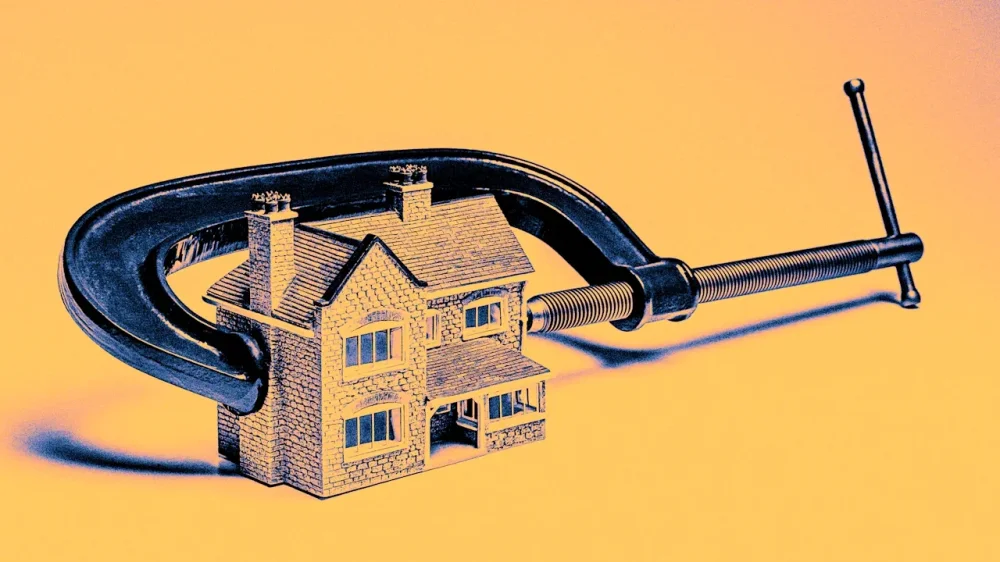

Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter. On Thursday, President Donald The President announced that government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac will buy an additional $200 billion in mortgage bonds. The President wrote: “Because I chose not to sell Fannie Mae and Freddie Mac in my first term, a truly great decision and against the advice of the “experts,” it is now worth many times that amount—an absolute fortune—and has $200 billion in cash. Because of this, I am instructing my representatives to buy $200 billion in mortgage bonds. This will drive mortgage rates down, monthly payments down, and make the cost of owning a home more affordable.” Long-term yields—like the 10-year Treasury yield and the average 30-year fixed mortgage rate—are set by demand / lack of demand for the underlying bond. Yields move inversely to bond prices. If demand for long-term bonds rises, prices go up and yields/mortgage rates fall. If bond demand falls, bond prices drop and yields/mortgage rates rise. For example, when the Federal Reserve engages in quantitative easing, as it did during the pandemic, it buys long-term assets like Treasuries and mortgage-backed securities (MBS), increasing bond demand and pushing bond prices up and long-term yields down, including mortgage rates. The Fed’s MBS purchases put additional downward pressure on mortgage rates in 2020 and 2021. Conversely, during quantitative tightening since 2022, the Fed has been letting MBS assets roll off its balance sheet without replacing them—effectively removing a major MBS buyer from the market—which can put additional upward pressure on 30-year fixed mortgage rates. Effectively, The President is proposing to use Fannie Mae and Freddie Mac—both in government conservatorship—to absorb a larger share of mortgage bonds, increasing relative market demand for MBS. That could put some short-term upward pressure on MBS prices and downward pressure on mortgage rates, further reducing the “mortgage spread.” Around the same time the Federal Reserve began raising short-term rates and stopped buying long-term bonds in the spring of 2022, financial markets started pulling back from bonds, causing long-term yields—including mortgage rates—to surge. Only, without the Fed buying MBS, the 30-year fixed average mortgage rates saw a bigger jump than the 10-year Treasury yield. At its peak in June 2023, the “mortgage spread”—the difference between the 10-year Treasury yield and the average 30-year fixed mortgage rate—hit 2.96 percentage points (296 bps). That was far above the 1.76 percentage point (176 bps) historical average since 1972. Over the past 2 years, the “mortgage spread” has slowly compressed—hitting 2.05 percentage points (205 bps) in December 2025. The goal of The President’s announcement on Thursday (i.e., Fannie Mae and Freddie Mac buying an additional $200 billion in mortgage bonds) is to accelerate that “mortgage spread” compression. As reported by Bloomberg in December, Fannie Mae and Freddie Mac have already started to accelerate their retained mortgage holdings—with them climbing around $69 billion in the second half of 2025. According to John Burns Research and Consulting, if Fannie Mae and Freddie Mac were to add another $200 billion in mortgage bond holdings in 2026, it would put the GSEs pretty close to their $450 billion legal limit ($225 billion each). On Thursday, Alex Thomas, research manager at JBREC, tweeted: “Fannie [Mae] and Freddie [Mac] have already added ~$70B to their retained mortgage portfolios since May of last year. Adding another $200B would basically put the GSEs at their legal cap ($225B each).” Following The President’s Thursday post, there was some immediate MBS pricing movement. That said, it’s unclear exactly just how much impact an additional $200 billion in GSE retained mortgage bonds would have on the “mortgage spread” and the average 30-year fixed mortgage rate. Through the end of June 2025, there is $9.26 trillion in agency mortgage-backed securities (MBS), according to data the Urban Institute recently provided to ResiClub. Below is the breakdown: —> $3.00 trillion held by depositories (banks) —> $2.74 trillion held everyone else —> $2.14 trillion held by the Federal Reserve —> $1.33 trillion held by foreign buyers —> $0.06 trillion held by GSEs (Fannie Mae and Freddie Mac) The chart below is the same as the one above, but it shows MBS holders by distribution. Prior to the Great Financial Crisis, the GSEs (Fannie Mae and Freddie Mac) used to be much bigger buyers of mortgage-backed securities. In an Urban Institute report published in January 2026, Laurie Goodman and Jim Parrott explain what happened: “For years, Fannie Mae and Freddie Mac were the buyers of last resort in the market, stepping in to profit from widening spreads and, in doing so, putting a comforting outer bound on MBS volatility. Once they went into conservatorship, the government-sponsored enterprises (GSEs) were replaced in that role by the Federal Reserve, which stepped into the agency MBS market to calm much larger swings in the economy. All of this went unnoticed outside of the MBS market until recently, when the Federal Reserve finally ended its time in the stabilizing role, leaving the MBS market without a buyer of last resort for the first time in decades.” “The GSEs gave up their role as market stabilizer when they went into conservatorship and began reducing their portfolio under the terms of their bailout by the Treasury. The Federal Reserve then promptly stepped into the role. As part of its broader effort to shore up the market in the wake of the financial crisis, the Federal Reserve bought $1.25 trillion in agency MBS between January 2009 and March 2010 and bought another $823 billion between 2012 and 2014. Largely because of that aggressive posture, along with the bailout of the GSEs, the MBS market and mortgage liquidity generally remained stable through the depths of the crisis, a remarkable feat given the level of dislocation in the rest of the economy.” “The Federal Reserve was then well positioned to handle the next major disruption in the MBS market, when financial markets seized up in the early days of the COVID-19 pandemic. In February and early March 2020, the financial markets froze, and investors were forced to sell their agency MBS to build cash reserves, pushing mortgage spreads wider by 75 basis points. The Federal Reserve stepped in in March, committing to buying agency MBS and Treasury securities “in the amounts needed to support smooth market functioning and effective transmission of monetary policy to broader financial markets and the economy.” 1 True to its word, the Federal Reserve, over the next month, bought more MBS than the entire gross production of the securities, stabilizing spreads and, with them, mortgages rates. Spreads ultimately settled a bit higher than they had been before the pandemic, but that was attributable to volatility in fixed income and a refinance wave triggered by the drop in Treasury rates.” “The Federal Reserve relinquished its role as the stabilizer of the agency MBS market when it pivoted to quantitative tightening in March 2022, ending its purchases of MBS and committing to running off its MBS portfolio. With the GSEs still operating under the portfolio constraints imposed in conservatorship, that left the market without a stabilizer for the first time in recent history.” View the full article

-

Barely 10 days into the new year, it already feels like you can’t look away from the news. In the last week alone, the U.S. military captured Venezuelan president Nicolás Maduro and took over operations of the country; President The President withdrew the U.S. from dozens of international organizations, including a major climate treaty; and an ICE agent fatally shot a Minneapolis resident, sparking outrage and widespread protests. If it seems impossible to focus on work—or anything else, for that matter—amid all this troubling news, you’re not alone. Plenty of research in recent years has shown that Americans are overwhelmed by the state of politics and feel a heightened sense of anxiety over the news cycle. There’s also clear evidence that doomscrolling and constantly absorbing negative media can interfere with our physical and mental health. It might feel like there’s no reprieve from the endless onslaught of news, and the idea of staying productive seems almost quaint when each day has something new in store. But there are, in fact, some things you can do to help ground yourself—and get through the workday without being consumed by the news cycle. Create some guardrails Our media consumption habits are unhealthy, and not only because of the obvious effects on our productivity. Engaging with the news cycle takes a toll on our well-being—and from an evolutionary perspective, our brains are wired to pay closer attention to negative news. “When we see something in the news that triggers our perception of danger, we have a physiological response in our bodies,” says Emma McAdam, a marriage and family therapist who also shares mental health resources on YouTube. “So in order to not be reactive, we have to be really intentional consumers of the news. And we have to ask ourselves: ‘Am I consuming news for entertainment, or am I consuming news to inform action?’” If the news you’re taking in is not actionable, McAdam says, it can just increase your stress levels or serve as a distraction. “It’s easy to pretend that we’re doing some important job by reading the news—that we’re being informed,” she says. “But realistically, we’re probably more emotionally driven to read the news.” At the same time, it’s also not realistic for many people to entirely block out the news—especially when it directly impacts their lives. McAdam argues you can, however, be more intentional about how you consume news to avoid simply consuming information that is not actually actionable. This can be as simple as turning off push notifications and carving out specific times of day to catch up on the news. Or you might remove certain apps from your phone so you’re less inclined to check the news unless you’re on your laptop. “Our bodies respond very differently to acute stress than chronic stress,” McAdam says. “We’re actually very good at managing little bits of stress. A big stressor in a short dose gives your nervous system a chance to get activated and then to relax and restore your internal sense of safety. But when we consume the news throughout our entire day, then we have this low level of chronic stress.” Step away from the devices There are, of course, jobs where you simply can’t avoid the news, or maybe a push notification pops up when you pick up your phone for something work-related. In those moments, you may have an emotional response that makes it difficult to stay on task. “We’re not able to focus and concentrate as well because our nervous system is activated,” says psychologist Maggie Stoutenburg, who works with the telehealth provider NY Mental Health Center. “We feel this distress, but then we also feel hopeless—and people can feel kind of paralyzed by that.” If you find yourself in that situation, it can be helpful to just step away from your desk. When you’re activated and on edge, doing something that lights up your parasympathetic nervous system can help calm you down, Stoutenburg says. Deep breathing can be “quite powerful,” she says, or you might try going on a brief walk or listening to soothing music. Even a funny video can do the trick. When you need to get back on track after a distressing news alert, Stoutenburg recommends trying to work for just 10–15 minute increments without letting your mind wander. “Give yourself some compassion,” she says. “Validate your own feelings, and try to acknowledge it and then redirect it. ‘Okay, there’s this stress here. Maybe there’s not a lot I can do about that in this moment, but what I can do is accomplish something in the next 10 or 15 minutes that will give me more of a sense of productivity and control’.” Focus on what you can control Embracing the things that are within your control can be a crucial tool for managing news-related anxiety. McAdam recommends an activity that can help you gain agency, by articulating exactly what is within your control and what is out of your hands. “You take a piece of paper, you divide it in half, and on one side, you write ‘things I can’t control,’ and on the other side you write, ‘what I can control,’” she says. “‘I can’t control what the President said today. But I can control whether I’m going to show up at a protest. I can control whether I love my kids’.” In other words, you do have a say in how you respond to depressing news—and McAdam points out that even anxiety can be a useful response at times, by nudging you to take action and relieve that feeling. “Anxiety isn’t just something bad that happens to us,” she says. “Anxiety is actually supposed to ask the question: Am I in danger? Is there something I should do about it? When we ask that question, we can get more clarity and be like, well, I can’t change this. I’ll let it go . . . And if there is something actionable, that little spurt of anxiety can help us take that action.” When there’s so much happening in the world, it can be difficult to stay motivated. You may have a harder time finding purpose or meaning in your work, especially in the face of more serious concerns. It can be helpful, then, to reframe how you think about your job or other elements of your life and understand where you can actually have an impact. “Most of the news we read is very far from us, and most of the good we can do is very close to us,” McAdam says. “Parenting matters. Being connected to our neighbors and being kind to our neighbors matters. Doing good in my sphere, doing good in my job, being kind to my coworkers, being really productive and solving [problems] at work—these are things that actually do make a difference and hopefully make the world a better, kinder, happier, safer place.” View the full article

-

We may earn a commission from links on this page. Deal pricing and availability subject to change after time of publication. The ANC headphones from Sony and Bose are great, but they look like gadgets, not music gear. Luckily, Marshall is offering these Monitor III ANC earbuds, which offer a cool retro look. And right now, they're available for the lowest price ever, at $279.99 (down from $379.99), beating the heavyweights from Sony and Bose on price. Marshall Monitor III Headphones $279.99 at Amazon $379.99 Save $100.00 Get Deal Get Deal $279.99 at Amazon $379.99 Save $100.00 These Monitor III headphones feature the iconic Marshall script logo, a retro brass control knob (instead of touch buttons), and a textured black vinyl finish that mimics Marshall guitar amps. Other than the looks, the most impressive part is the battery life. These will last you for 70 hours of ANC playback (and 100 hours without ANC). That is a staggering number; for comparison, the Sony XM6 gets you 30-40 hours of playback per charge. The headphones are also collapsible, folding into a small ball. They come with a hard-shell travel case and are pretty lightweight, too, at 250 grams. There is no 3.5mm headphone jack here, but the box does include a USB-C to 3.5mm cable for wired listening. They feature the signature Marshall sound, warm and punchy. They are tuned for listening to rock, heavy metal and guitar-heavy music, and offer a more fun sound profile compared to Sony or Bose, which can sound a bit more flat or balanced. In its review, PCMag gave the Monitor IIIs a 4.0 star rating, noting that they deliver a "pleasing audio signature, a comfortable fit with intuitive controls, easy portability, and excellent battery life." View the full article

-

Your team and your clients both win. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-

Your team and your clients both win. By Jody Grunden Building the Virtual CFO Firm in the Cloud Go PRO for members-only access to more Jody Grunden. View the full article

-

Two years ago, countries around the world set a goal of “transitioning away from fossil fuels in energy systems in a just, orderly and equitable manner.” The plan included tripling renewable energy capacity and doubling energy efficiency gains by 2030—important steps for slowing climate change since the energy sector makes up about 75% of the global carbon dioxide emissions that are heating up the planet. The world is making progress: More than 90% of new power capacity added in 2024 came from renewable energy sources, and 2025 saw similar growth. However, fossil fuel production is also still expanding. And the United States, the world’s leading producer of both oil and natural gas, is now aggressively pressuring countries to keep buying and burning fossil fuels. The energy transition was not meant to be a main topic when world leaders and negotiators met at the 2025 United Nations climate summit, COP30, in November in Belém, Brazil. But it took center stage from the start to the very end, bringing attention to the real-world geopolitical energy debate underway and the stakes at hand. Brazilian President Luiz Inácio Lula da Silva began the conference by calling for the creation of a formal road map, essentially a strategic process in which countries could participate to “overcome dependence on fossil fuels.” It would take the global decision to transition away from fossil fuels from words to action. More than 80 countries said they supported the idea, ranging from vulnerable small island nations like Vanuatu that are losing land and lives from sea level rise and more intense storms, to countries like Kenya that see business opportunities in clean energy, to Australia, a large fossil-fuel-producing country. Opposition, led by the Arab Group’s oil- and gas-producing countries, kept any mention of a “road map” energy transition plan out of the final agreement from the climate conference, but supporters are pushing ahead. I was in Belém for COP30, and I follow developments closely as a former special climate envoy and head of delegation for Germany and senior fellow at the Fletcher School at Tufts University. The fight over whether there should even be a road map shows how much countries that depend on fossil fuels are working to slow down the transition, and how others are positioning themselves to benefit from the growth of renewables. And it is a key area to watch in 2026. The battle between electro-states and petro-states Brazilian diplomat and COP30 President André Aranha Corrêa do Lago has committed to lead an effort in 2026 to create two road maps: one on halting and reversing deforestation and another on transitioning away from fossil fuels in energy systems in a just, orderly, and equitable manner. What those road maps will look like is still unclear. They are likely to be centered on a process for countries to discuss and debate how to reverse deforestation and phase out fossil fuels. Over the coming months, Corrêa plans to convene high-level meetings among global leaders, including fossil fuel producers and consumers, international organizations, industries, workers, scholars and advocacy groups. For the road map to both be accepted and be useful, the process will need to address the global market issues of supply and demand, as well as equity. For example, in some fossil fuel-producing countries, oil, gas or coal revenues are the main source of income. What can the road ahead look like for those countries that will need to diversify their economies? Nigeria is an interesting case study for weighing that question. Oil exports consistently provide the bulk of Nigeria’s revenue, accounting for around 80% to over 90% of total government revenue and foreign exchange earnings. At the same time, roughly 39% of Nigeria’s population has no access to electricity, which is the highest proportion of people without electricity of any nation. And Nigeria possesses abundant renewable energy resources across the country, which are largely untapped: solar, hydro, geothermal and wind, providing new opportunities. What a road map might look like In Belém, representatives talked about creating a road map that would be science-based and aligned with the Paris climate agreement, and would include various pathways to achieve a just transition for fossil-fuel-dependent regions. Some inspiration for helping fossil-fuel-producing countries transition to cleaner energy could come from Brazil and Norway. In Brazil, Lula asked his ministries to prepare guidelines for developing a road map for gradually reducing Brazil’s dependency on fossil fuels and find a way to financially support the changes. His decree specifically mentions creating an energy transition fund, which could be supported by government revenues from oil and gas exploration. While Brazil supports moving away from fossil fuels, it is also still a large oil producer and recently approved new exploratory drilling near the mouth of the Amazon River. https://datawrapper.dwcdn.net/ctvhR/1 Norway, a major oil and gas producer, is establishing a formal transition commission to study and plan its economy’s shift away from fossil fuels, particularly focusing on how the workforce and the natural resources of Norway can be used more effectively to create new and different jobs. Both countries are just getting started, but their work could help point the way for other countries and inform a global road map process. The European Union has implemented a series of policies and laws aimed at reducing fossil fuel demand. It has a target for 42.5% of its energy to come from renewable sources by 2030. And its EU Emissions Trading System, which steadily reduces the emissions that companies can emit, will soon be expanded to cover housing and transportation. The Emissions Trading System already includes power generation, energy-intensive industry, and civil aviation. https://datawrapper.dwcdn.net/PeAlZ/1 Fossil fuel and renewable energy growth ahead In the U.S., the The President administration has made clear through its policymaking and diplomacy that it is pursuing the opposite approach: to keep fossil fuels as the main energy source for decades to come. The International Energy Agency still expects to see renewable energy grow faster than any other major energy source in all scenarios going forward, as renewable energy’s lower costs make it an attractive option in many countries. Globally, the agency expects investment in renewable energy in 2025 to be twice that of fossil fuels. At the same time, however, fossil fuel investments are also rising with fast-growing energy demand. The IEA’s World Energy Outlook described a surge in new funding for liquefied natural gas, or LNG, projects in 2025. It now expects a 50% increase in global LNG supply by 2030, about half of that from the U.S. However, the World Energy Outlook notes that “questions still linger about where all the new LNG will go” once it’s produced. What to watch for The Belém road map dialogue and how it balances countries’ needs will reflect on the world’s ability to handle climate change. Corrêa plans to report on its progress at the next annual U.N. climate conference, COP31, in late 2026. The conference will be hosted by Turkey, but Australia, which supported the call for a road map, will be leading the negotiations. With more time to discuss and prepare, COP31 may just bring a transition away from fossil fuels back into the global negotiations. Jennifer Morgan is a senior fellow at the Center for International Environment and Resource Policy and Climate Policy Lab at Tufts University. This article is republished from The Conversation under a Creative Commons license. Read the original article. View the full article

-

Bolívar has fallen nearly 20% on black market, after US capture of President MaduroView the full article

-

In terms of securing financing for your S Corporation, comprehending the best loan options available is vital. SBA loans offer significant amounts and favorable terms, whereas nonbank lenders can provide quick access to funds. Knowing how to evaluate loan terms and prepare your business can make a difference in approval chances. To navigate these choices effectively, it’s important to grasp key documentation requirements and strategies that can improve your application’s strength. Key Takeaways SBA loans offer significant funding up to $5 million with lower interest rates starting at 6.5% for S corporations. Nonbank lenders, like Fundbox, provide quick approvals and flexible credit lines suitable for S Corps with lower credit scores. Eligibility for SBA loans includes at least one year of operational history and a minimum credit score of 580 for owners. Preparing accurate financial statements and legal documentation enhances loan approval chances for S Corporations. Maintaining strong financial health, including a Debt Service Coverage Ratio above 1.25, is crucial for securing favorable loan terms. Top Lenders for S Corporations When you’re looking for financing options as an S corporation, it’s essential to know the top lenders that cater particularly to your needs. Popular choices include Newtek, which specializes in SBA loans, and Fundbox, known for quick approvals and flexible credit lines. These lenders understand the unique structure and tax implications of S corporations, so they can offer customized solutions. You’ll likely need to provide documentation, such as an Operating Agreement and Articles of Incorporation, to establish your eligibility for a business loan for S corp. Furthermore, maintaining a strong Debt Service Coverage Ratio (DSCR) above 1.25 can greatly improve your chances of securing favorable loan terms. You should also be aware that substantial owners may need to provide personal guarantees, which could impact their credit scores. If you’re considering an LLC loan agreement or a shareholder loan, make sure you compare these options carefully to find the best fit for your business. Understanding SBA Loans for S Corps When considering SBA loans for your S Corporation, it’s essential to understand the eligibility criteria and the loan application process. You’ll need to prepare a detailed business plan and financial statements to showcase your business’s viability. Eligibility Criteria Overview To qualify for SBA loans, S Corporations must meet specific eligibility criteria that guarantee financial stability and operational viability. You’ll need at least one year of operational history and demonstrate stable cash flow. A minimum credit score of 580 is typically required, and significant owners must provide a personal guarantee, including their credit history and personal assets. Detailed financial statements, such as three years of business tax returns and a current balance sheet, are necessary as well. Requirement Details Operational History At least 1 year Minimum Credit Score 580 Maximum Loan Amount (7(a)) Up to $5 million Understanding these criteria can help you secure the right sh loan for your S Corp. Loan Application Process Maneuvering the loan application process for SBA loans can be complex, but comprehending the necessary steps will help streamline your efforts. First, gather detailed documentation, such as business and personal tax returns, financial statements, and a solid business plan to demonstrate viability. Significant owners must be prepared to provide personal guarantees and align on financial goals. Personal credit scores are vital, with a minimum score of 580 typically required. Moreover, verify your Debt Service Coverage Ratio (DSCR) exceeds 1.25, reflecting healthy cash flow. Finally, be aware that the application process can take several weeks, so prompt submission of all required documents is important to avoid delays and improve your chances of approval. Benefits of SBA Loans SBA loans offer several key advantages for S corporations seeking funding. These loans provide long-term financing options, with amounts typically ranging from $50,000 to $5 million, allowing you to access crucial capital for growth and operational needs. One of the most attractive features is the lower interest rates, often starting as low as 6.5%, which helps minimize your borrowing costs. Furthermore, SBA loans come with flexible repayment terms, extending up to 25 years for real estate purchases, easing your monthly payment burden. The SBA 7(a) loan program is particularly beneficial because of its versatility, enabling you to use funds for working capital, equipment purchases, or refinancing existing debt, provided you meet the eligibility criteria. Benefits of Nonbank Lending Options Even though traditional banks often impose strict requirements for loans, nonbank lending options provide a valuable alternative for S corporations looking to secure funding. These lenders, like Fundbox and Fora Financial, often feature faster approval times, with some offering funding within 24 hours. Many nonbank lenders have more flexible eligibility requirements, accepting credit scores as low as 475, which can be beneficial for S corps with less established credit histories. In addition, nonbank lenders typically don’t charge prepayment penalties, allowing you to pay off your loans early without incurring extra costs. Options like Accion focus on microlending, providing customizable funding terms customized to your specific financial needs. Moreover, many nonbank lenders offer additional resources, such as coaching and support networks, to help you effectively manage your business finances alongside your loan. This extensive support can be invaluable as you navigate the challenges of running your S corporation. Evaluating Loan Terms and Interest Rates When evaluating loan terms and interest rates for your S corporation, it’s essential to compare the interest rates offered by different lenders. You’ll want to take into account the flexibility of loan terms, as some options may better suit your business’s cash flow needs. Furthermore, analyzing the repayment structure can help you avoid potential financial strain as you ensure you meet your obligations effectively. Interest Rate Comparison Interest rates for business loans can vary widely, and grasping these differences is vital for making informed financial decisions. For well-established businesses, rates can be as low as 6.5% for a $100,000 loan over 24 months. Conversely, startups often face markedly higher rates, with loans available at 35% for the same amount over just 6 months because of increased risk. Women- and minority-owned businesses benefit from competitive rates, such as 9.99% for loans up to $250,000 over 12 months. Low-revenue businesses may encounter much higher interest rates, reaching 36% for a $250,000 loan over 3 months. Moreover, fast funding options can provide quick access to $250,000 for 12 months at a rate of 14%. Grasping these variations is vital for your decision-making. Loan Term Flexibility Grasping loan term flexibility is vital for S Corporations as it directly impacts your repayment strategy and overall financial health. Different types of loans come with varying terms and interest rates, so comprehending these can help you make informed decisions. Established businesses can secure loans for up to 24 months, with interest rates as low as 6.5%. Startups may only access funding for 6 months, but often at high rates of 35%, which demands careful planning. Women- and minority-owned businesses typically enjoy 12-month loans at competitive rates of 9.99%. Selecting the right loan term can greatly affect your cash flow, so it’s important to evaluate your options based on your business needs and financial situation. Repayment Structure Analysis Grasping the repayment structure of loans is critical for S corporations, as it directly affects your financial planning and stability. You’ll encounter various repayment terms depending on your business profile. For instance, well-established S Corps might secure $100,000 over 24 months at a low rate of 6.5%. Conversely, startups may face higher risks with $100,000 for 6 months at an alarming 35%. Women- and minority-owned businesses can access $250,000 for 12 months at a favorable 9.99%. Nevertheless, low-revenue firms might see $250,000 with a short repayment of 3 months at 36%. Comprehending these terms helps you evaluate options that align with your cash flow and repayment capacity, ensuring you make informed financial decisions. Preparing Your S Corp for Loan Applications Preparing your S Corp for loan applications requires a strategic approach to guarantee your business presents itself as a reliable candidate to lenders. Start by ensuring all shareholders review and correct their personal credit scores, since one partner’s bad credit can impact the entire application. It’s likewise crucial to prepare key legal documents, such as the Operating Agreement and Articles of Incorporation, to verify your business structure. Here are some important steps to reflect on: Gather financial statements, including income statements and balance sheets, to showcase your corporation’s financial health. Confirm all co-owners consent to the loan application and align on financial goals to present a unified front. Maintain accurate and current tax filings to avoid red flags during the loan approval process. Key Documentation Required for S Corps When you’re applying for a loan as an S corporation, having the right documentation is vital to your success. First, you’ll need to provide legal documents like the Operating or Partnership Agreement, which outlines roles and profit-sharing among co-owners. Next, submit your Articles of Organization or Incorporation to verify your business structure. An Employer Identification Number (EIN) is also important for tax purposes and must be included in your loan documentation. Furthermore, prepare business and personal tax returns for all shareholders, as these demonstrate your financial health and ownership stakes. Finally, ownership documentation showing ownership percentages and decision-making authority among co-owners is critical for evaluating your loan eligibility. By gathering these documents, you’ll improve your chances of securing the financing your S corporation needs. Tips for Improving Loan Approval Chances To improve your chances of loan approval for your S corporation, it’s crucial to focus on both your personal and business financial health. Start by ensuring that all co-owners have strong personal credit scores, as one partner’s bad credit can undermine the entire application. Furthermore, maintain transparent and organized business records to build lender confidence. Here are some key strategies to improve your loan approval chances: Regularly review your Debt Service Coverage Ratio (DSCR) to keep it above 1.25, indicating healthy cash flow. Prepare thorough legal documentation, like an Operating Agreement, to clarify roles among co-owners. Align on a cohesive business plan that outlines financial goals and projections. Frequently Asked Questions What Is the Monthly Payment on a $50,000 Business Loan? The monthly payment on a $50,000 business loan varies based on the interest rate and loan term. For example, at an 8.75% rate over six months, you’d pay about $1,594.88 monthly. If the rate rises to 14% for 12 months, expect around $5,039.28 monthly. On the other hand, a lower 6.5% over 24 months results in payments of about $2,221.03. Always factor in fees and total costs when calculating your monthly obligations. How to Qualify for a $200,000 Business Loan? To qualify for a $200,000 business loan, you need to demonstrate a solid cash flow, ideally with a Debt Service Coverage Ratio (DSCR) above 1.25. Gather necessary documentation, including personal tax returns, financial statements, and legal agreements. Maintain a strong credit profile, aiming for a FICO score of at least 600. Align financial goals with co-owners and present a cohesive business plan detailing how the loan will generate revenue and guarantee repayment. What Is the 20% Rule for SBA? The 20% rule for SBA loans requires that you, as a business owner, must hold at least 20% of your company’s equity to qualify for certain SBA programs. This rule guarantees you’re financially invested in your business, promoting responsible management. For S Corporations, the shareholders must collectively meet this 20% threshold. If you don’t meet this requirement, you could face ineligibility for valuable SBA loan options, limiting your financing possibilities. Can I Take Out a Loan From My S Corp? Yes, you can take out a loan from your S corporation, but it must be a genuine loan with proper documentation. The terms should be similar to what you’d find in a typical loan with unrelated parties, including interest rates and repayment schedules. This guarantees the loan is recognized for tax purposes, and it can additionally increase your shareholder basis, allowing for greater loss deductions against your income. Avoid circular loans to prevent IRS scrutiny. Conclusion To sum up, S Corporations have several viable financing options, including SBA loans and nonbank lending solutions. By comprehending these choices and preparing properly, you can notably improve your chances of securing funding. Focus on maintaining strong financial health and organizing fundamental documentation, as these factors play a vital role in the application process. With the right approach, you can find the best loan option to support your business growth and operational needs effectively. Image via Google Gemini This article, "Best Business Loan Options for S Corps" was first published on Small Business Trends View the full article

-

In terms of securing financing for your S Corporation, comprehending the best loan options available is vital. SBA loans offer significant amounts and favorable terms, whereas nonbank lenders can provide quick access to funds. Knowing how to evaluate loan terms and prepare your business can make a difference in approval chances. To navigate these choices effectively, it’s important to grasp key documentation requirements and strategies that can improve your application’s strength. Key Takeaways SBA loans offer significant funding up to $5 million with lower interest rates starting at 6.5% for S corporations. Nonbank lenders, like Fundbox, provide quick approvals and flexible credit lines suitable for S Corps with lower credit scores. Eligibility for SBA loans includes at least one year of operational history and a minimum credit score of 580 for owners. Preparing accurate financial statements and legal documentation enhances loan approval chances for S Corporations. Maintaining strong financial health, including a Debt Service Coverage Ratio above 1.25, is crucial for securing favorable loan terms. Top Lenders for S Corporations When you’re looking for financing options as an S corporation, it’s essential to know the top lenders that cater particularly to your needs. Popular choices include Newtek, which specializes in SBA loans, and Fundbox, known for quick approvals and flexible credit lines. These lenders understand the unique structure and tax implications of S corporations, so they can offer customized solutions. You’ll likely need to provide documentation, such as an Operating Agreement and Articles of Incorporation, to establish your eligibility for a business loan for S corp. Furthermore, maintaining a strong Debt Service Coverage Ratio (DSCR) above 1.25 can greatly improve your chances of securing favorable loan terms. You should also be aware that substantial owners may need to provide personal guarantees, which could impact their credit scores. If you’re considering an LLC loan agreement or a shareholder loan, make sure you compare these options carefully to find the best fit for your business. Understanding SBA Loans for S Corps When considering SBA loans for your S Corporation, it’s essential to understand the eligibility criteria and the loan application process. You’ll need to prepare a detailed business plan and financial statements to showcase your business’s viability. Eligibility Criteria Overview To qualify for SBA loans, S Corporations must meet specific eligibility criteria that guarantee financial stability and operational viability. You’ll need at least one year of operational history and demonstrate stable cash flow. A minimum credit score of 580 is typically required, and significant owners must provide a personal guarantee, including their credit history and personal assets. Detailed financial statements, such as three years of business tax returns and a current balance sheet, are necessary as well. Requirement Details Operational History At least 1 year Minimum Credit Score 580 Maximum Loan Amount (7(a)) Up to $5 million Understanding these criteria can help you secure the right sh loan for your S Corp. Loan Application Process Maneuvering the loan application process for SBA loans can be complex, but comprehending the necessary steps will help streamline your efforts. First, gather detailed documentation, such as business and personal tax returns, financial statements, and a solid business plan to demonstrate viability. Significant owners must be prepared to provide personal guarantees and align on financial goals. Personal credit scores are vital, with a minimum score of 580 typically required. Moreover, verify your Debt Service Coverage Ratio (DSCR) exceeds 1.25, reflecting healthy cash flow. Finally, be aware that the application process can take several weeks, so prompt submission of all required documents is important to avoid delays and improve your chances of approval. Benefits of SBA Loans SBA loans offer several key advantages for S corporations seeking funding. These loans provide long-term financing options, with amounts typically ranging from $50,000 to $5 million, allowing you to access crucial capital for growth and operational needs. One of the most attractive features is the lower interest rates, often starting as low as 6.5%, which helps minimize your borrowing costs. Furthermore, SBA loans come with flexible repayment terms, extending up to 25 years for real estate purchases, easing your monthly payment burden. The SBA 7(a) loan program is particularly beneficial because of its versatility, enabling you to use funds for working capital, equipment purchases, or refinancing existing debt, provided you meet the eligibility criteria. Benefits of Nonbank Lending Options Even though traditional banks often impose strict requirements for loans, nonbank lending options provide a valuable alternative for S corporations looking to secure funding. These lenders, like Fundbox and Fora Financial, often feature faster approval times, with some offering funding within 24 hours. Many nonbank lenders have more flexible eligibility requirements, accepting credit scores as low as 475, which can be beneficial for S corps with less established credit histories. In addition, nonbank lenders typically don’t charge prepayment penalties, allowing you to pay off your loans early without incurring extra costs. Options like Accion focus on microlending, providing customizable funding terms customized to your specific financial needs. Moreover, many nonbank lenders offer additional resources, such as coaching and support networks, to help you effectively manage your business finances alongside your loan. This extensive support can be invaluable as you navigate the challenges of running your S corporation. Evaluating Loan Terms and Interest Rates When evaluating loan terms and interest rates for your S corporation, it’s essential to compare the interest rates offered by different lenders. You’ll want to take into account the flexibility of loan terms, as some options may better suit your business’s cash flow needs. Furthermore, analyzing the repayment structure can help you avoid potential financial strain as you ensure you meet your obligations effectively. Interest Rate Comparison Interest rates for business loans can vary widely, and grasping these differences is vital for making informed financial decisions. For well-established businesses, rates can be as low as 6.5% for a $100,000 loan over 24 months. Conversely, startups often face markedly higher rates, with loans available at 35% for the same amount over just 6 months because of increased risk. Women- and minority-owned businesses benefit from competitive rates, such as 9.99% for loans up to $250,000 over 12 months. Low-revenue businesses may encounter much higher interest rates, reaching 36% for a $250,000 loan over 3 months. Moreover, fast funding options can provide quick access to $250,000 for 12 months at a rate of 14%. Grasping these variations is vital for your decision-making. Loan Term Flexibility Grasping loan term flexibility is vital for S Corporations as it directly impacts your repayment strategy and overall financial health. Different types of loans come with varying terms and interest rates, so comprehending these can help you make informed decisions. Established businesses can secure loans for up to 24 months, with interest rates as low as 6.5%. Startups may only access funding for 6 months, but often at high rates of 35%, which demands careful planning. Women- and minority-owned businesses typically enjoy 12-month loans at competitive rates of 9.99%. Selecting the right loan term can greatly affect your cash flow, so it’s important to evaluate your options based on your business needs and financial situation. Repayment Structure Analysis Grasping the repayment structure of loans is critical for S corporations, as it directly affects your financial planning and stability. You’ll encounter various repayment terms depending on your business profile. For instance, well-established S Corps might secure $100,000 over 24 months at a low rate of 6.5%. Conversely, startups may face higher risks with $100,000 for 6 months at an alarming 35%. Women- and minority-owned businesses can access $250,000 for 12 months at a favorable 9.99%. Nevertheless, low-revenue firms might see $250,000 with a short repayment of 3 months at 36%. Comprehending these terms helps you evaluate options that align with your cash flow and repayment capacity, ensuring you make informed financial decisions. Preparing Your S Corp for Loan Applications Preparing your S Corp for loan applications requires a strategic approach to guarantee your business presents itself as a reliable candidate to lenders. Start by ensuring all shareholders review and correct their personal credit scores, since one partner’s bad credit can impact the entire application. It’s likewise crucial to prepare key legal documents, such as the Operating Agreement and Articles of Incorporation, to verify your business structure. Here are some important steps to reflect on: Gather financial statements, including income statements and balance sheets, to showcase your corporation’s financial health. Confirm all co-owners consent to the loan application and align on financial goals to present a unified front. Maintain accurate and current tax filings to avoid red flags during the loan approval process. Key Documentation Required for S Corps When you’re applying for a loan as an S corporation, having the right documentation is vital to your success. First, you’ll need to provide legal documents like the Operating or Partnership Agreement, which outlines roles and profit-sharing among co-owners. Next, submit your Articles of Organization or Incorporation to verify your business structure. An Employer Identification Number (EIN) is also important for tax purposes and must be included in your loan documentation. Furthermore, prepare business and personal tax returns for all shareholders, as these demonstrate your financial health and ownership stakes. Finally, ownership documentation showing ownership percentages and decision-making authority among co-owners is critical for evaluating your loan eligibility. By gathering these documents, you’ll improve your chances of securing the financing your S corporation needs. Tips for Improving Loan Approval Chances To improve your chances of loan approval for your S corporation, it’s crucial to focus on both your personal and business financial health. Start by ensuring that all co-owners have strong personal credit scores, as one partner’s bad credit can undermine the entire application. Furthermore, maintain transparent and organized business records to build lender confidence. Here are some key strategies to improve your loan approval chances: Regularly review your Debt Service Coverage Ratio (DSCR) to keep it above 1.25, indicating healthy cash flow. Prepare thorough legal documentation, like an Operating Agreement, to clarify roles among co-owners. Align on a cohesive business plan that outlines financial goals and projections. Frequently Asked Questions What Is the Monthly Payment on a $50,000 Business Loan? The monthly payment on a $50,000 business loan varies based on the interest rate and loan term. For example, at an 8.75% rate over six months, you’d pay about $1,594.88 monthly. If the rate rises to 14% for 12 months, expect around $5,039.28 monthly. On the other hand, a lower 6.5% over 24 months results in payments of about $2,221.03. Always factor in fees and total costs when calculating your monthly obligations. How to Qualify for a $200,000 Business Loan? To qualify for a $200,000 business loan, you need to demonstrate a solid cash flow, ideally with a Debt Service Coverage Ratio (DSCR) above 1.25. Gather necessary documentation, including personal tax returns, financial statements, and legal agreements. Maintain a strong credit profile, aiming for a FICO score of at least 600. Align financial goals with co-owners and present a cohesive business plan detailing how the loan will generate revenue and guarantee repayment. What Is the 20% Rule for SBA? The 20% rule for SBA loans requires that you, as a business owner, must hold at least 20% of your company’s equity to qualify for certain SBA programs. This rule guarantees you’re financially invested in your business, promoting responsible management. For S Corporations, the shareholders must collectively meet this 20% threshold. If you don’t meet this requirement, you could face ineligibility for valuable SBA loan options, limiting your financing possibilities. Can I Take Out a Loan From My S Corp? Yes, you can take out a loan from your S corporation, but it must be a genuine loan with proper documentation. The terms should be similar to what you’d find in a typical loan with unrelated parties, including interest rates and repayment schedules. This guarantees the loan is recognized for tax purposes, and it can additionally increase your shareholder basis, allowing for greater loss deductions against your income. Avoid circular loans to prevent IRS scrutiny. Conclusion To sum up, S Corporations have several viable financing options, including SBA loans and nonbank lending solutions. By comprehending these choices and preparing properly, you can notably improve your chances of securing funding. Focus on maintaining strong financial health and organizing fundamental documentation, as these factors play a vital role in the application process. With the right approach, you can find the best loan option to support your business growth and operational needs effectively. Image via Google Gemini This article, "Best Business Loan Options for S Corps" was first published on Small Business Trends View the full article

-

We may earn a commission from links on this page. Prime Video's Fallout, an adaptation of the popular video game series of the same name, is set more than two centuries from now on an Earth still devastated by a long-ago nuclear war between the United States and China. The protagonist, Lucy MacLean (Ella Purnell), emerges from the underground fallout shelter where she's lived her entire life in search of her father, and a fuller understanding of the world above, a wasteland is dominated by warring factions and freakish mutants. It's a gutsy, hilarious adaptation of out-there source material, and it's wild to consider that, in the space of a couple of years, we've gone from approximately zero worthwhile video game adaptations to having two series (the other being HBO's The Last of Us) contending for Outstanding series Emmys. Strange days. Yet these two are definitely not the only post-apocalyptic narratives you'll find streaming right now. Here are 15 more to shows, from dramatic, to funny, to everything between, to fuel your end times fantasies. (It's fine, everything's fine, I'm fine lol.) Twisted Metal (2023 – ) This '90s were a great time for post-apocalyptic video games, and the 2020s would seem to be a great time to adapt them for TV. The most brutal show on the Peacock block stars Anthony Mackie as John Doe, and is based on the vehicular combat games that parents probably hated way more than they hated Fallout (it’s a lot of wild, demolition-derby style action involving smashing and/or blowing up your opponents). The show does what it says on the tin, providing plenty of frenetic car-on-car action (and car-on-semi, car-on-hearse, -ice cream truck, etc.). Mackie is an effective anchor for the chaos, and he's joined by an impressive supporting cast that includes Stephanie Beatriz, Thomas Haden Church, and Neve Campbell. Cars go boom, mostly, and sometimes that’s exactly what you want—it’s the show for the 15-year-old gamer inside all of us. A third season is coming. Stream Twisted Metal on Peacock. Twisted Metal (2023 – ) at Peacock Learn More Learn More at Peacock Silo (2023 – ) Rebecca Ferguson stars as Juliette Nichols, an engineer who gets wrapped up in an investigation involving the local sheriff (played by David Oyelowo)—usual stuff, except that the characters all inhabit a massive silo, 144-levels deep, protecting the remaining 10,000 humans from the allegedly poisoned world above. Those running the silo have managed to convince everyone left that only strict adherence to rules and procedures will keep them safe from the dangers outside. This isn't the heightened, colorful apocalypse of Fallout, but nevertheless prestige drama that incorporates elements of horror, mystery, and science fiction to tell very human stories about fear and control. Two further seasons are coming. Stream Silo on Apple TV+. Silo (2023 – ) at Apple TV+ Learn More Learn More at Apple TV+ Z Nation (2014 - 2019) Where The Walking Dead and The Last of Us made prestige television out of the specifically zombie apocalypse, this SyFy channel original is all about zombies as a campy, gory good time. Things kick off with a soldier who’s been tasked with transporting a package across country. The package in question is actually a human being, a survivor of a zombie bite who might be able to help create a vaccine (sound familiar?). The show comes from the schlock-masters at The Asylum, purveyors of infamous B-movies like Sharknado, which should tell you all you need to know about the tone. It lacks the gloss of Fallout, for sure, but it shares some of that show's more offbeat sensibilities. Stream Z Nation on Peacock, Tubi, AMC+, and Shudder. Z Nation at Peacock Learn More Learn More at Peacock The Decameron (2024) I've never been particularly convinced that an end-of-the-world narrative needs to be set in the future, and this very darkly funny, but surprisingly humane, show offers up a slice of a real-life apocalypse, 14th century style. Loosely adapting Giovanni Boccaccio's story collection with hints of Bridgerton-esque swagger, we're taken to plague-ravaged Florence, as a bunch of nobles and attendants make their way across a dangerous landscape to hole up in a countryside villa to wait out the end while draining the liquor supplies—as you would. Rules and social mores are turned upside down, particularly by servant Licisca (Tanya Reynolds), who kind of accidentally kills her lady on the way to the villa and then decides to take her place. Despite being about how hell is other people, the show makes for an entirely addictive binge experience. Stream The Decameron on Netflix. The Decameron (2024) at Netflix Learn More Learn More at Netflix Into the Badlands (2015 – 2019) About 500 years from now, war has eradicated anything resembling civilization and left the planet ravaged, even as some vestiges of technology remain. Still, firearms are largely taboo given the devastation they've caused—allowing for an action apocalypse dominated by kick-ass martial arts combat. The Badlands, Rocky Mountains and Mississippi River here, are dominated by competing feudal(-esque) kingdoms, dominated by Marton Csokas's creepy, over-the-top Baron Quinn and, initially, his chief lieutenant Sunny (Daniel Wu). Stream Into the Badlands on Prime Video and AMC+. Into the Badlands at Prime Video Learn More Learn More at Prime Video Scavengers Reign (2023) This one's a smart, impressively voice-acted, and beautifully animated sci-fi epic following the stranded survivors of the crashed interstellar cargo ship Demeter 227. The web of natural life on the world on which they find themselves is unusually complex, and the rules they're used to don't seem to apply. The outer space sci-fi setting here doesn't, on the surface, have much to do with the blasted desert of Fallout, but both shows are set in imagined worlds that are intricate, colorful, and devilishly clever. Stream Scavengers Reign on HBO Max. Scavengers Reign (2023) at HBO Max Learn More Learn More at HBO Max Snowpiercer (2020 – 2024) Though initially feeling like an unnecessarily extended imitation of Bong Joon Ho's allegorical post-apocalyptic film, Snowpiercer, the show, ultimately takes on a life of its own as a clever sci-fi melodrama, smartly recognizing that there are no heroes and few true villains at the end of the world—mostly just people doing whatever they can to survive. In a frozen future (2026, to be precise), humanity survives on an extremely long train that circumnavigates the globe. If it stops, the power goes out and everyone (literally everyone) dies. Those who came aboard with wealth live near the front in relative luxury, while the poor live on scraps (or worse) in the train's tail. Daveed Diggs stars as former detective Andre Layton, a 'Tailie' deputized by Jennifer Connelly's Melanie Cavill, engineer and the train's Head of Hospitality, to solve a series of murders. The inevitable uprising that follows sees the two of them on different sides of a violent conflict, before each realizes they're just pawns of apocalypse's elite. Stream Snowpiercer on AMC+ or buy episodes from Prime Video. Snowpiercer (2020 – 2024) at AMC+ Learn More Learn More at AMC+ Train to the End of the World (2024) This anime series makes clear that it definitely isn't 5G that we need to be worried about...it's 7G, an experimental cell network that warps reality and leaves Japan as a series of isolated settlements—it's also caused strange mutations, including turning people into animals, and creating mind-controlling mushrooms à la The Last of Us. Discovering evidence that one of her classmates is alive outside of Tokyo, Shizuru Chikura gets some friend together and they commandeer a train to carry them through the strange new wilderness. Stream Train to the End of the World on Crunchyroll or buy episodes from Prime Video. Train to the End of the World at Crunchyroll Learn More Learn More at Crunchyroll The Last of Us (2023 – ) Predating Fallout by just about a year, The Last of Us started what remains an extremely exclusive club of video game adaptations that click, in this case even picking up a bunch of Emmys—Fallout maybe running a bit behind in terms of major awards, but has picked up nominations for Outstanding Drama and Lead Actor Emmys, which ain't too shabby. Pedro Pascal and Bella Ramsey star here, at least initially, as Joel and Ellie, travelers through an apocalyptic wasteland populated by zombified humans infected by a fungus. There's genuine suspense and expertly crafted horror in the show's zombie threat, but it's all built around the dynamic between Joel and Ellie, a beaten-down smuggler and the immune teenager he's being paid to deliver to the other side of the country. Their relationship sells the premise, and makes the stakes feel very real when the zombie mushroom people come out to bite. When the show upends that cart in season two, it's devastating. Stream The Last of Us on HBO Max. The Last of Us at HBO Max Learn More Learn More at HBO Max Murderbot (2025 – ) I suppose it says something about our uniquely fun era that you can turn on the TV and take your pick of future dystopias—here we visit a hyper-capitalist future in which everything's hunky-dory, as long as you mostly only care about money. A dark comedy based on the Hugo-Award winning book series by Martha Wells, the show stars Alexander Skarsgård is the title's hilariously deadpan robot, a private "security construct" who's managed to hack its way through its own programming and gain free will—which it mostly wants to use to watch its favorite streaming shows. It can't just run off for fear of drawing attention, but the self-named Murderbot (it's being ironic, kinda) is content to do the bare minimum when it's assigned to a team of inexperienced and naive hippie researchers who don't see the need for a killer security robot—at least, not until they're enmeshed in a complicated capitalist plot in which they're all just cogs. Stream Murderbot on Apple TV+. Murderbot (2025 – ) at Apple TV+ Learn More Learn More at Apple TV+ Station Eleven (2021 – 2022) The miniseries, based on the Emily St. John Mandel bestseller, was released at either the best time or the worst possible time, the story of a flu pandemic twenty years on hitting HBO square in the middle of COVID—and don't all of our current apocalypse dramas owe just a bit to that waking nightmare? The show follows two tracks, one introducing Kirsten Raymonde, a young stage actor whose performance in a production of King Lear is cut short by the onset of a virus with a 99% fatality rate. We also visit Kirsten twenty years on, still an actor, in a world very much changed. It’s a slow-burn, picking up steam only after a couple of episodes, but ultimately, the series makes a moving case for the power of art, even (or especially) in moments when survival is on the line. Stream Station Eleven on HBO Max. Station Eleven at HBO Max Learn More Learn More at HBO Max The Leftovers (2014 – 2017) No weird mutations here; instead we get an apocalypse that looks disturbingly normal. As the series begins, around 2% of the world's population disappears without explanation—it's enough to upend just about everything. Politics have adapted to the new normal, religions have collapsed and reformed, and families have had to make peace with the inexplicable loss of loved ones. The first season revolves around the Garvey family led by Kevin (Justin Theroux), a sheriff whose wife (Amy Brenneman) left him to join a cult, while subsequent seasons broaden the scope to bring in other characters in other locations. Showrunner Damon Lindelof also co-created Lost, and Leftovers inherits that show's relatively grim tone while doing it one better in sticking a landing. Stream The Leftovers on HBO Max. The Leftovers at HBO Max Learn More Learn More at HBO Max The Rain (2018 – 2020) We get a lot of Fallout-esque desert dystopias, but leave it to those melancholy Danes to center an apocalypse around precipitation. In this three-season import, a virus spread by rainfall that wipes out most of the population of Scandinavia. Siblings Simone and Rasmus emerge from their bunker six years later, setting off across Scandinavia with the hope of finding a safe haven, and maybe their father. It turns out that one of them holds the key to wiping out the virus and saving the world. It’s not the most original premise (The Last of Us game came out five years earlier), but the setting gives it a unique feel, and the series comes to a decisive ending. Stream The Rain on Netflix. The Rain at Netflix Learn More Learn More at Netflix Now Apocalypse (2019) OK, so maybe the end of days is feeling a little heavy at this point, and you're looking for something a little brighter and a lot more gay. I got you! New Queer Cinema pioneer Greg Araki followed up his neon-tinged apocalypse in Kaboom with Now Apocalypse, a successor in spirit. Avan Jogia plays Ulysses Zane, living in sun-soaked California with his best friend Carly (Kelli Berglund), a struggling actress and sex worker. He keeps having bizarre dreams about an alien invasion that feel increasingly like they might be premonitions...or possibly just anxiety delusions brought on by too much weed. The show only lasted one season, and never quite made it to its own prophesied apocalypse, but it was definitely fun while it lasted, and definitely offers something a bit to the left of the typical dreary end-of-the-world. Stream Now Apocalypse on Tubi. Now Apocalypse at Tubi Learn More Learn More at Tubi The 100 (2014 – 2020) At seven seasons, the CW’s YA The 100 is, currently, our most deeply explored TV apocalypse, telling the story of the descendants of refugees of nuclear devastation who return to Earth from their habitat in space—to encounter the remnants of humanity who’d survived on Earth. Naturally, the first people sent to scope things out are the juvenile delinquents (better them than me, honestly), and they discover that three civilizations that have risen up in the aftermath of the apocalypse, and they are all pretty darned scary (including the inevitable cannibals). The show builds an impressive mythology over the course of its run, leading to a conclusion that’s borderline metaphysical. Buy episodes of The 100 from Prime Video. The 100 (2014 – 2020) at Prime Video Learn More Learn More at Prime Video View the full article

-

A new year brings a new tax filing season. With many cash-strapped Americans worried about their finances, many can’t wait to file their returns. The sooner you file, the sooner your chances of getting your refund, after all. But just when can you begin submitting your tax return to the Internal Revenue Service (IRS)? That depends. Here’s what you need to know about the 2026 tax filing season. When does the 2026 tax filing season begin? There are actually two start dates to the 2026 tax filing season this year. The 2026 tax filing season refers to the period taxpayers have to file their tax returns for the 2025 calendar year. According to an IRS press release on Thursday, the official day of the 2026 tax filing season begins on Monday, January 26, 2026. From this day, anyone who is required to file a federal tax return can do so. But January 26 isn’t the earliest date some people can begin submitting their tax returns to the IRS. As the IRS noted in its Thursday release, the agency will actually begin to accept tax returns from a select group of taxpayers starting today, Friday, January 9, 2026. Who can submit their tax returns beginning on January 9? Not every taxpayer can submit their returns beginning on January 9. According to the IRS, this submission start date is only open to “qualified taxpayers.” So, who is a qualified taxpayer? The IRS says a person meets that designation if they are in a select group of people who use the IRS Free File program to submit their taxes. Per the IRS’s Thursday notice: “The IRS Free File program will begin accepting individual tax returns starting Friday, Jan. 9 for qualified taxpayers. Taxpayers comfortable preparing their own taxes can use IRS Free File Fillable Forms starting Jan. 26, regardless of income.” What this means is not everyone who uses the IRS Free File program can submit their tax returns starting today—only select individuals. Those IRS Free File users who can begin submitting their tax returns today are limited to those individuals who need to report $89,000 in adjusted gross income (AGI) or less, according to the IRS’s Free File information page. Taxpayers who use Free File’s online forms and who make more than $89,000 in adjusted gross income will need to wait until January 26 to submit their tax returns, just like everyone else. Will eligible taxpayers who submit via Free File before January 26 get their tax refunds faster? That’s unknown, as every individual’s tax situation is different. In the IRS’s notice, it states that the agency will begin “accepting” tax returns from eligible individuals on January 9. It does not say it will begin “processing” the returns then. What this means is that even if you are eligible to submit your tax return before January 26, it can’t be guaranteed that the IRS will actually begin processing your return before January 26. Still, it’s reasonable to assume that if you want to get your tax refund as soon as possible, you should file your tax return on the earliest date you can. The IRS says individuals have until Wednesday, April 15, 2026, to file their taxes for the 2025 tax year and pay any taxes owed. View the full article

-

Increase your website‘s domain authority by building quality backlinks, focusing on the right keywords, etc. View the full article

-

Two things can be true at once. K-pop is an inextricable force in global pop culture, and it has long been undercelebrated at institutions like the Grammys — where K-pop artists have performed but have never taken home a trophy. That could change at next month’s 2026 Grammy Awards ceremony. Songs released by K-pop artists — or K-pop-adjacent artists, more on that later — have received nominations in the big four categories for the first time. Rosé, perhaps best known as one-fourth of the juggernaut girl group Blackpink, is the first K-pop artist to ever receive a nomination in the record of the year field for “APT.,” her megahit with Grammys’ favorite Bruno Mars. The song of the year category also features K-pop nominees for the first time. “APT.” will go head-to-head with the fictional girl group HUNTR/X’s “Golden,” performed by Ejae, Audrey Nuna and Rei Ami from the “KPop Demon Hunters” soundtrack. And the girl group Katseye, the brain child of HYBE — the entertainment company behind K-pop sensation BTS and countless other international acts — fashioned in the image of the K-pop idol system, has been nominated for best new artist. Is this a historic moment for K-pop? It depends on who you ask. Areum Jeong, assistant professor of Korean Studies at Arizona State University and author of “K-pop Fandom: Performing Deokhu from the 1990s to Today” says the majority of these nominations strike her more as “a de-territorialized, hybrid idea of K-pop,” instead of a recognition of K-pop. While Rosé “was recruited and trained under the K-pop system, and while ‘APT.’ does contain some motifs from the Korean drinking game,” Jeong says, “the song does not feel like a localized K-pop production. … Same with Katseye, who was trained and produced under HYBE but marketed more toward Western fans and listeners.” Jeong says that both “APT.” and Katseye’s “Gabriela” — both of which will go head-to-head with “Golden” in the pop duo/group performance category — “seem less K-pop than other K-pop songs that could have been nominated over the years.” She argues the same is true for the music of “Kpop Demon Hunters.” “It is very similar to ‘APT.’ in that it takes inspiration and motif from Korean culture,” where “K-pop serves as an idea, a jumping-off point, or a motif, creating alternatives or new possibilities.” Mathieu Berbiguier, a visiting assistant professor in Korean Studies at Carnegie Mellon University, points out that these nominations differ from past K-pop Grammy nominations because “Golden,” “APT.” and Katseye all feature “a mainstream popular music factor.” That’s the connection of a massive popular Netflix film (“Kpop Demon Hunters”), a collaboration with Bruno Mars (“APT.”), and Katseye’s international membership and Netflix series (“Pop Star Academy: Katseye”), respectively. “It tells you that K-pop is not considered as something niche anymore,” he says. “Now, when we think about pop music in general, we also think of K-pop as part of it.” Bernie Cho, industry expert and president of the South Korean agency, the DFSB Kollective, agrees that there is an international, mainstream appeal to the nominees. “All the nominees represent a sort of post-idol K-pop, in the sense that Rosé, the three ladies of HUNTR/X and Katseye represent the globalized version of K-pop, where the ‘K’ is very much there, but some people might argue it’s silent. The songs are not necessarily for Korea, by Korea, from Korea, just kind of beyond Korea,” he says. “It’s a celebration and testament to how diverse and dynamic K-pop has become.” Why are these acts being recognized now? “For years, the Recording Academy has snubbed K-pop acts that have set record-breaking standards, such as BTS,Seventeen and Stray Kids,” argues Jeong. “I think one of the main reasons is that the Western world is still so resistant to non-English lyrics.” “It does not surprise me that ‘APT.’ and Katseye’s music, which mainly contain English lyrics and seem less K-pop, were nominated,” she continues. Berbiguier adds that “is a reflection of K-pop nowadays, like, trends: the fact that there’s less and less Korean and more and more English.” There may be an additional factor at play. Tamar Herman, a music journalist and author of the “Notes on K-pop” newsletter, says many critics and industry voices found 2025 to be a lackluster year for new pop music in the U.S. — a fact that was all but confirmed in Luminate’s 2025 Mid-Year Report, which found that streams of new music had slowed compared to the year prior, potentially due to a dearth of megahits dominating the charts. “Yes, it’s a big moment for K-pop, but it is so overdue, these recognitions are more of a sign of how poorly the music industry in the U.S. did this year that we’re looking externally,” she says. She argues that acknowledgment of Korean entertainment from U.S. entertainment industries is more symbolic of U.S. cultural dominance slipping than “K-pop being really good, because K-pop has been really good for a really long time,” she says. “This is all recognition of just global storytelling improvement, global taste-making improvement.” “I don’t want to diminish it,” she adds. “These are all universally friendly, accessible, good pop songs.” And if they weren’t, they wouldn’t connect. “It’s very obvious that they’re not just performers. They’re artists. They’re singers. They’re songwriters,” says Cho. Will a K-pop artist win a Grammy for the first time this year? The jury is still out. “I think it’s not even a matter of if or when. It’s going to be who and how many,” says Cho. Others are less committal. “It’s hard to predict,” says Berbiguier. “For me, it’s more possible that ‘Golden’ gets one.” “Yes and no,” offers Herman. For her, it depends on an evolving and fluid definition of K-pop. After all, HUNTR/X is a fictional girl group from an animated film that did not debut through the K-pop music industry system. Would a victory for their song “Golden” mean a victory of K-pop? That’s a matter of opinion. The 68th Grammy Awards will be held Feb. 1 at Crypto.com Arena in Los Angeles. The show will air on CBS and stream on Paramount+. For more coverage, visit https://apnews.com/hub/grammy-awards. —Maria Sherman, AP Music Writer View the full article

-

Paul Nurse tells FT that national science academy should avoid ‘making judgments’ about ‘character’ of fellowsView the full article

-

We may earn a commission from links on this page. Deal pricing and availability subject to change after time of publication. I really adore my Series 10 Apple Watch. But if I hadn't upgraded last year, I would have gone for the Series 11, just for the extra battery life upgrade. I usually like to wait for discounts before upgrading, though, and if you're like me, Amazon has some good news: While the Series 11 only came out four months ago, it's already down to its lowest price ever. You can get the 42mm Series 11 model for $299 (down from $399) and the 46mm Series 11 model for $329 (down from $429). That's a discount of $100 across the board. Apple Watch Series 11 GPS 42mm Jet Black Aluminum Case with Black Sport Band - M/L $299.00 at Walmart $399.00 Save $100.00 Get Deal Get Deal $299.00 at Walmart $399.00 Save $100.00 The Series 10 was the one with the big redesign, but the Series 11 upgrade is about the smaller, quality-of-life upgrades, the chief of which is the battery life. For the first time in 10 years, the Apple Watch's battery life jumped from 18 hours to 24 hours. I already use some tweaks to make my Series 10 last for two days, so the Series 11 model will go even further still. The screen is brighter at 2,000 nits peak brightness, and Apple now uses a Ion-X glass for better wide-angle viewing. It's also twice as scratch-resistant as before, IP6X dust resistant, and swim-proof (WR50). And if you plan to go for the cellular mode, you also get 5G for the first time in an Apple Watch. There are also new software features like background hypertension notifications, and a new Sleep Score (though they're available on the older models as well). Overall, the Series 11 makes for a solid upgrade if you're using an Apple Watch Series 7 or 8. PCMag gave the Apple Watch Series 11 a 4.5 star "Outstanding" rating, and an Editor's Choice award. PCMag notes that "while the watch's design and sensors haven’t changed much this generation, they remain at the head of the class. With top-notch lifestyle and health features, excellent performance, and almost two days of power on a charge, the Series 11 earns our Editors’ Choice award, making it the best Apple Watch for most iPhone users." Our Best Editor-Vetted Tech Deals Right Now Apple AirPods Pro 3 Noise Cancelling Heart Rate Wireless Earbuds — $199.99 (List Price $249.00) Apple Watch Series 11 [GPS 46mm] Smartwatch with Jet Black Aluminum Case with Black Sport Band - M/L. Sleep Score, Fitness Tracker, Health Monitoring, Always-On Display, Water Resistant — $329.00 (List Price $429.00) Amazon Fire TV Stick 4K Plus — (List Price $24.99 With Code "FTV4K25") Dell 15 DC15255 (AMD Ryzen 7 7730U, 1TB SSD, 16GB RAM) — $519.99 (List Price $688.99) Samsung Galaxy Tab A9+ 64GB Wi-Fi 11" Tablet (Silver) — $159.99 (List Price $219.99) Samsung Galaxy Watch 8 — $279.99 (List Price $349.99) Deals are selected by our commerce team View the full article

-